Kenanga Research & Investment

Daily Technical Highlights - (ANCOMLB, PHARMA)

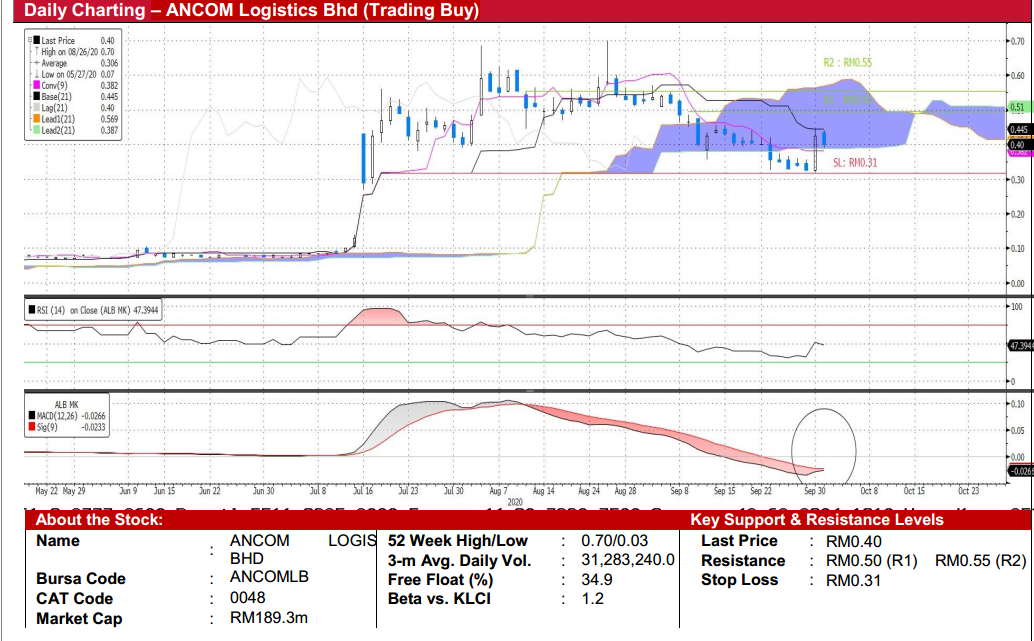

ANCOM Logistics Bhd (Trading Buy)

• ANCOMLB announced on 16th July that its holding company ANCOM had entered into an agreement with (i) S7 Holdings, (ii) Merrington Assets Limited, and (iii) MY E.G. Capital Sdn Bhd , which will allow S5 Systems Sdn Bhd (mainly owned by S7 Holdings) to perform a backdoor listing via ANCOMLB.

• Interestingly, S5 which has its expertise in the security and biometric registration, is said to be involved in all the major bids for the upcoming National Integrated Immigration System (NIIS), which is worth up to RM1.5b. Thus, the RTO is viewed positively for ANCOMLB.

• Chart-wise the stock has retraced from an all-time high of RM0.70 (26th of August 2020), to its current level, which is finding support near the “Kumo Bull Clouds”. We believe a trend reversal is in sight given the potential bullish MACD Crossover and uptick in RSI.

• Should the buying momentum resume, our overhead resistances are located at RM0.50 (R1: +25% upside potential) and RM0.55 (R2: +38% upside potential).

• Meanwhile our stop loss is pegged at RM0.31 (23% downside risk).

PHARMANIAGA Bhd (Trading Buy)

• PHARMA is involved in the (i) manufacturing of pharmaceutical medicine, (ii) logistics and distribution , and (iii) sales and marketing of medical products.

• The group is poised to benefit from the vaccine with its (i) well-integrated logistics and distribution network nationwide, and (ii) already existing Small Volume Injectable (SVI) plant located in Puchong which is suitable for the “fill and finish” of inactivated/kill vaccine.

• The stock has recently found support at its 50-Day SMA while forming a bullish “pennant” pattern after retracing from an alltime high of RM6.69 (on 25th August). Thus, should the buying interest persist, our overhead resistances are set at RM5.30 (R1:+13% upside potential) and RM5.60 (R2: +19% upside potential).

• Meanwhile our stop loss is pegged at RM4.20 (or 11% downside risk).

• Based on consensus estimates, the company is projected to turn from a loss to a net profit of RM70.2m in FY20E and RM71.6m (+2%, YoY) in FY21E. This translates to a forward PER of 17x in both years respectively.

Source: Kenanga Research - 2 Oct 2020

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Kenanga Research & Investment

Actionable Technical Highlights - PRESS METAL ALUMINIUM HLDG BHD (PMETAL)

Created by kiasutrader | Nov 25, 2024

Actionable Technical Highlights - PETRONAS CHEMICALS GROUP BHD (PCHEM)

Created by kiasutrader | Nov 25, 2024

Weekly Technical Highlights – Dow Jones Industrial Average (DJIA)

Created by kiasutrader | Nov 25, 2024

Malaysia Consumer Price Index - Edge up 1.9% in October amid food price surge

Created by kiasutrader | Nov 25, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

2

3

save malaysia!

Visa-free travel to China extended for Malaysians to 30 days

4

Good Articles to Share

5

Good Articles to Share

What’s behind the slew of restaurant bankruptcies in 2024? Experts unpack the problems

6

Good Articles to Share

Four convicted in Spain over homophobic murder that sparked nationwode protests

7

Good Articles to Share

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....