Kenanga Research & Investment

Weekly Technical Review - 23 November 2020

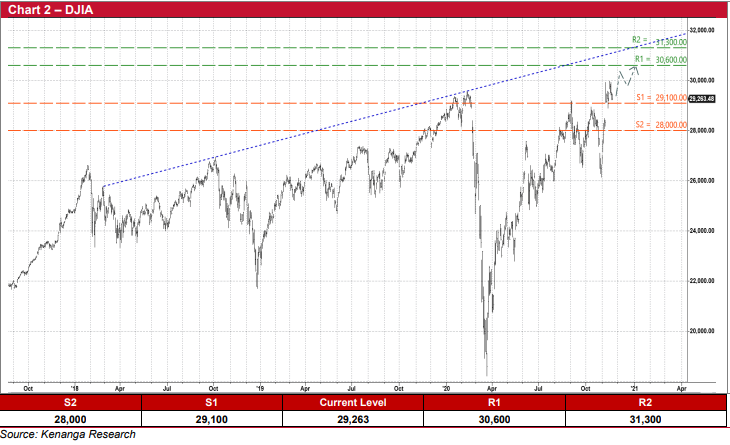

The Malaysian stock market rally may be short-lived as the bulls appear to be exhausted after raging since the start of November. The key FBMKLCI touched an intra-week high of 1,613 last Tuesday before losing steam to end at 1,594 on Friday. This was just slightly above the preceding week’s closing of 1,590. On Wall Street, the DJIA soared initially only to surrender the early gains and finished at 29,263 for a weekly loss of 216 points or 0.7%

Trading activity remained brisk on the local stock exchange with daily average transaction volume standing at 13.1b shares valued at RM5.9b, versus the average of 13.5b shares worth RM5.9b traded the week before. Continuing from where they left off, domestic institutions remained net buyers (of RM270m) as foreigners were still net sellers (amounting to RM269m) while local retail investors posted negligible net selling flows (of RM1m) last week.

Kicking off the week ahead, today is the cut-off date for the December’s FTSE Bursa Malaysia semi-annual review to determine stocks to be inserted and deleted in the FBM Index series, whereby decisions will be made based on the ranking by full market capitalisation when market closes today. As of last Friday, in the running to be added as index constituents for the widelyfollowed FBMKLCI are Supermax Corporation (ranked 22nd), Kossan Rubber (ranked 29th) and QL Resources (ranked 30th). Possibly to be replaced on the list is any of the following three existing component stocks, namely Genting Bhd (ranked 31st), Genting Malaysia (ranked 33rd) and KLCC Property (ranked 34th).

To recap, the ground rules state that a security will be inserted into the FBMKLCI if it rises to 25th position or above while a security will be deleted from the FBMKLCI if it falls to 36th position or below. Therefore, as it stands, our sensitivity analysis (which hypothetically hold the rest of the index members constant) suggests that Supermax Corporation will probably make it to the list unless the stock declines by more than 6% today. Both Kossan Rubber and QL Resources are not likely to be included as their respective share prices would need to climb by more than 23% and 24% by the end of today. On the other hand, Genting Bhd is expected to remain as an index constituent (unless the stock drops by more than 25% today) while either Genting Malaysia or KLCC Property (despite their share prices being above the 36th position threshold by comfortable margins of 19% and 17%, respectively) could be ousted to make way for the likely entry of Supermax Corporation.

And this Wednesday or Thursday, investors will switch their attention to the Parliament when the Budget 2021 proposal will go through the voting process by the elected representatives. Meanwhile, more earnings report cards are due for release as the corporate reporting season for the July to September quarter comes to an end next Monday (30 November).

On the chart, after breaking past the 50-day SMA and a descending trendline, the FBMKLCI appears toppish following the emergence of a potential double-top formation. This was also approximately the same level at which the benchmark index pulled back subsequently after struggling futilely to overcome in November and December last year. With the immediate momentum on the downside, we retain our support levels at 1,550 (S1) and 1,510 (S2) while our resistance hurdles stand at 1,600 (R1) and 1,645 (R2). Over on Wall Street, against a volatile backdrop, the DJIA may continue to show a positive bias ahead. Our major support and resistance levels for the DJIA remain at 29,100 (S1) / 28,000 (S2) and 30,600 (R1) / 31,300 (R2), respectively.

Source: Kenanga Research - 23 Nov 2020

More articles on Kenanga Research & Investment

Actionable Technical Highlights - PRESS METAL ALUMINIUM HLDG BHD (PMETAL)

Created by kiasutrader | Nov 25, 2024

Actionable Technical Highlights - PETRONAS CHEMICALS GROUP BHD (PCHEM)

Created by kiasutrader | Nov 25, 2024

Weekly Technical Highlights – Dow Jones Industrial Average (DJIA)

Created by kiasutrader | Nov 25, 2024

Malaysia Consumer Price Index - Edge up 1.9% in October amid food price surge

Created by kiasutrader | Nov 25, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

2

3

save malaysia!

Visa-free travel to China extended for Malaysians to 30 days

4

Good Articles to Share

5

Good Articles to Share

Four convicted in Spain over homophobic murder that sparked nationwode protests

6

Good Articles to Share

7

Good Articles to Share

What’s behind the slew of restaurant bankruptcies in 2024? Experts unpack the problems

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....