Kenanga Research & Investment

Daily technical highlights – (OPENSYS, JCY)

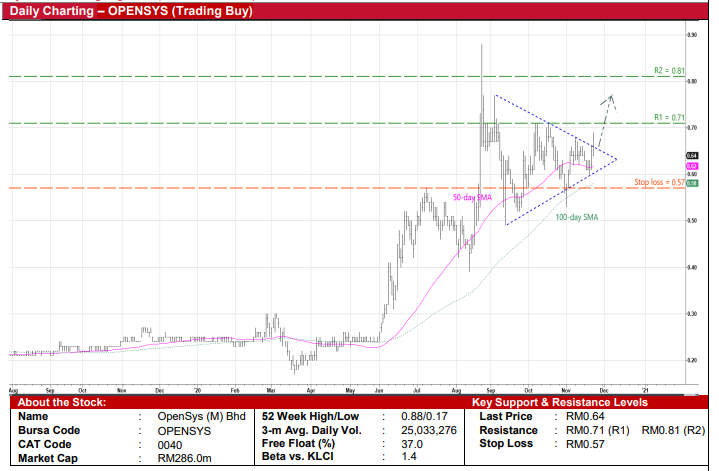

OpenSys (M) (Trading Buy)

- OPENSYS has four business revenue models, namely: (i) outright sales of cash recycling machines and cheque deposit machines to financial institutions, (ii) software development services, (iii) outsourcing services via the deployment of bill payment kiosks to utility, insurance and telecommunication companies, and (iv) maintenance services of the machines.

- In addition, the Group runs a dedicated online solar energy platform (buySolar), which is an online marketplace for renewable energy focussing on solar solutions and financing. It has recently signed a collaborative agreement with ACE Market-listed EPCC provider Solarvest Holdings to provide solar solutions referral to the latter.

- The Group’s bottomline has risen every year between FY16 and FY19, up from RM6.0m to RM11.1m over the past three years. For the 9-month ended September 2020, its net profit continued to grow by 21% YoY to RM7.3m while net cash & short-term investments stood at RM30.5m (or 6.8 sen per share) as of end-September this year.

- On the chart, OPENSYS shares – treading above the key 50-day and 100-day SMA lines – are currently riding on a positive momentum amid strong trading interest.

- With a symmetrical triangle possibly in the making, the stock could stage a technical breakout and trend higher to extend the continuation pattern.

- We have set our resistance targets at RM0.71 (R1; 11% upside potential) and RM0.81 (R2; 27% upside potential) for OPENSYS’ share price to test going forward.

- Our stop loss price is pegged at RM0.57 (or 11% below yesterday’s closing price of RM0.64).

JCY International Bhd (Trading Buy)

- JCY is a key supplier and contract manufacturer of precision components and sub-assembly for the hard disk drive (HDD) industry with production plants located in Malaysia, Thailand and China.

- In the red for the last two financial years, the Group is on track to return to the black after posting net profit of RM11.5m in the 9-month ended June 2020 (from a net loss of RM52.0m previously). The turnaround performance was mainly attributable to higher margins as a result of cost rationalisation efforts and better exchange rates.

- Financially stable, the Group was in a net cash position of RM304.7m (or 14.5 sen per share) as of June this year.

- Technically speaking, the ongoing share price weakness – which has slid from RM0.78 in early November to close at RM0.64 yesterday – presents a buying-on-weakness opportunity to accumulate the stock.

- With the positive trend still intact as JCY shares continue to hover above the 38.2% Fibonacci retracement line, the stock could climb towards our resistance thresholds of RM0.73 (R1) and RM0.81 (R2) when buying interest resumes. This implies upside potentials of 14% and 27%, respectively.

- We have set our stop loss price at RM0.57 (or 11% downside risk).

Source: Kenanga Research - 24 Nov 2020

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Kenanga Research & Investment

Actionable Technical Highlights - PRESS METAL ALUMINIUM HLDG BHD (PMETAL)

Created by kiasutrader | Nov 25, 2024

Actionable Technical Highlights - PETRONAS CHEMICALS GROUP BHD (PCHEM)

Created by kiasutrader | Nov 25, 2024

Weekly Technical Highlights – Dow Jones Industrial Average (DJIA)

Created by kiasutrader | Nov 25, 2024

Malaysia Consumer Price Index - Edge up 1.9% in October amid food price surge

Created by kiasutrader | Nov 25, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

2

3

save malaysia!

Visa-free travel to China extended for Malaysians to 30 days

4

Good Articles to Share

5

Good Articles to Share

Four convicted in Spain over homophobic murder that sparked nationwode protests

6

Good Articles to Share

7

Good Articles to Share

What’s behind the slew of restaurant bankruptcies in 2024? Experts unpack the problems

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....