After struggling in year 2012, many poultry farming companies finally caught investors' eyes by producing much better earnings since the start of year 2014.

As a result, most of their share prices have gone up about 50% and some more than 100% in just one year time, outperforming the unfortunate KLCI by several streets.

Is it too late to join the poultry party now? Are those poultry farming companies still undervalued after the jump in share price?

I have found 9 listed companies involved in poultry farming and related business. I'll just do a simple comparison among them.

Not every company runs exactly the same business. Some rear chicken only for its meat (broiler), some only for its eggs (layer), some slaughter the chicken, some process the meat to nuggets etc (food).

Some companies also venture into related businesses such as marine food, chicken feeds, making fertilizer from chicken manure, manufacturing egg trays and trading animal health products.

Below are main business for the 9 listed companies

| Company | Business |

| QL | Broiler, Layer, Feeds, Marine, Palm Oil |

| Huat Lai | Broiler, Layer, Feeds, Fertilizer, Trays |

| CAB | Broiler, Food, Marine, Retail |

| Lay Hong | Broiler, Layer, Food, Supermarket |

| Farmbes | Broiler, Layer, Food, Property |

| PW | Broiler, Layer, Feeds, Cattle, Food |

| Teo Seng | Layer, Feeds, Trays, Animal food & health products |

| LTKM | Layer, Sand mining, Property |

| TPC | Layer |

Looking into their historical financial results, almost all except QL and may be Teoseng, have rather "choppy" performance in which net profit swing up & down despite consistently higher revenue every year.

Due to company expansion and inflation, we would expect revenue to go up consistently. So the fluctuating net profit must be due to fluctuating cost.

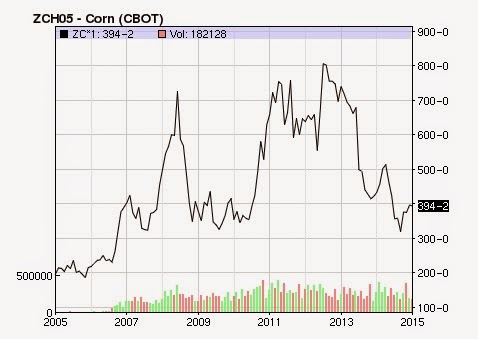

For pure broiler and/or layer farming, chicken feeds make up 70-75% of its cost of sales. So market price of corn and soybean which are used as chicken feeds will have a big impact on the company's performance.

Other than increase in poultry & eggs selling price, significant reduction in corn and soybean price since 2013 has largely improved the earnings of poultry farming operators.

Charts below show 10-year historical corn & soybean price.

Charts below show 10-year historical corn & soybean price.

As we can see from the charts above, corn & soybean price have dropped about 50% from their peak in 2012, mainly due to overproduction in the US.

From 2010, corn price rose steeply for almost 100% in less than a year, while soybean price also rose about 50% in the same period. Both stayed at high level throughout 2011-2012.

This may explain why most poultry farming companies suffered loss (except QL, Teo Seng & PW) or lower profit (Teoseng & PW) in calendar year 2012.

Now the corn & soybean price have suddenly dropped to about 8-year low. Do you think it will continue to drop to its 10-year low, or rebound, or move sideways in 2015?

From history, it can rise as fast as it falls.

Nevertheless, I think no one can be sure but surely it will have a great impact on poultry farmers' earning.

Among those 9 poultry-related companies, which one is the best to invest in?

I will use annualized figures to calculate the EPS to better reflect each company's latest performance, as I predict most of them will release even better results in the final quarter of CY2014 due to even lower feed price in the 2nd half of 2014.

So, this analysis which uses annualized earnings (except CAB), will not be very accurate.

So, this analysis which uses annualized earnings (except CAB), will not be very accurate.

| Stock | FY End | Revenue | PATAMI | PATAMI % | ROE | CR | D/E |

| QL | Mac | 2620 | 176.4 | 6.7 | 13.6 | 1.76 | 0.44 |

| Huat Lai | Dec | 1222 | 44.6 | 3.6 | 20.5 | 0.58 | 2.44 |

| CAB | Sep | 672 | 11.2 | 1.7 | 6.5 | 0.73 | 0.61 |

| Lay Hong | Mac | 646 | 15.7 | 2.4 | 12.3 | 0.83 | 1.38 |

| Farmbes | Dec | 432 | 2.7 | 0.6 | 2.8 | 1.15 | 2.74 |

| Teo Seng | Dec | 363 | 40.9 | 11.3 | 27.2 | 1.12 | 0.26 |

| PW | Dec | 287 | 14.1 | 4.9 | 6.5 | 0.88 | 0.40 |

| LTKM | Mac | 187 | 29.7 | 15.9 | 16.9 | 2.40 | NC |

| TPC | Dec | 79 | 3.8 | 4.8 | 20.1 | 0.41 | 2.25 |

NC = net cash

CR = current ratio

CR = current ratio

QL is the largest among all in term of market cap, revenue and net profit, with its diversification in businesses and also geographical location.

QL has been holding a significant stake in Lay Hong since 2010. It currently owns 38.3% of Lay Hong and recently failed in a rather hostile takeover bid to acquire Lay Hong.

Teo Seng is a subsidiary of Leong Hup which was recently taken private and delisted in 2012. Leong Hup is the country's largest integrated poultry operator.

Teo Seng is a subsidiary of Leong Hup which was recently taken private and delisted in 2012. Leong Hup is the country's largest integrated poultry operator.

TPC which is currently a PN17 company, is a 52.91% subsidiary of Huat Lai since 2012.

Meanwhile, Farmbes recently appears as a subject of a RM380mil reverse takeover by Chinese-owned SHH (M) Holding Sdn Bhd.

US-owned Cargill Malaysia is reported to be keen on a controlling stake in CAB as well.

It seems like merger & acquisition activities are robust within the poultry industry.

Meanwhile, Farmbes recently appears as a subject of a RM380mil reverse takeover by Chinese-owned SHH (M) Holding Sdn Bhd.

US-owned Cargill Malaysia is reported to be keen on a controlling stake in CAB as well.

It seems like merger & acquisition activities are robust within the poultry industry.

Other than CAB, PW & Farmbes, all other companies' ROE are good at above 10%, especially Teo Seng, Huat Lai & TPC which are above 20%, thanks to recent lower feeds price.

It's noteworthy that Teo Seng and LTKM's net profit margin stand out from the rest at more than 10%.

In term of balance sheet, it looks like poultry farming is a capital intensive business as many companies are heavily debt-ridden.

Huat Lai, Farmbes & TPC all have net debt to equity ratio of above 2x while Lay Hong is at 1.38. Only LTKM manage to keep a net cash position with impressive current ratio.

From the table above, generally the more "investable" ones to me are QL, Teo Seng & LTKM. CAB & PW are not that attractive due to thin margin and low ROE, besides higher borrowings.

| Stock | Price | #EPS | PE | NAS | PB | DIV | DY% |

| QL | 3.26 | 14.1 | 23.1 | 1.04 | 3.1 | 3.5 | 1.1 |

| Huat Lai | 2.85 | 51.6 | 5.5 | 2.52 | 1.1 | 4 | 1.4 |

| CAB | 1.01 | 8.5 | 11.9 | 1.16 | 0.9 | 0 | 0 |

| Lay Hong | 3.42 | 31.0 | 11.0 | 2.55 | 1.3 | 5 | 1.5 |

| Farmbes | 0.60 | 4.4 | 13.6 | 1.55 | 0.4 | 0 | 0 |

| Teo Seng | 1.85 | 20.4 | 9.1 | 0.75 | 2.5 | *10 | 5.4 |

| PW | 1.52 | 23.1 | 6.6 | 3.71 | 0.4 | 5 | 3.3 |

| LTKM | 4.09 | 68.4 | 6.0 | 4.05 | 1.0 | 18 | 4.4 |

| TPC | 0.385 | 4.8 | 8.0 | 0.24 | 1.6 | 0 | 0 |

# base on annualized earnings

QL is no doubt a great company but its PE ratio and PB ratio are too high now.

Though Huat Lai has lowest PE, relatively low PB ratio and high ROE of 20.5, it also has scary amount of debts and very low current ratio.

Apart from Huat Lai, LTKM & PW have the lowest PE at 6.0x & 6.6x respectively, while both Farmbes & PW have the lowest PB at 0.4x.

Teo Seng's dividend is the most attractive, followed by LTKM and PW. It is a little surprise to me that Huat Lai still pay dividend.

So it is not difficult to come to a conclusion that Teo Seng & LTKM are the two companies that suit my investment style.

Coincidentally, both are only in layer farming without broiler farming. Both export their eggs to Singapore as well.

Though Teo Seng is valued higher compared to LTKM now, LTKM seems too conservative in expanding its poultry business compared to Teo Seng.

LTKM who already built 26 units of terrace houses in Banting since 2011 even plans to go bigger into property development with its 20-acre land in Jenjarom!

Anyway, I think both are still not bad to invest in, depending on your taste & timing.

For me, I don't know much about their future expansion plan but it seems like organic growth will be slow.

Besides Teo Seng & LTKM, PW is also worth a second look.

It just made its first venture into table eggs production since 2013 with its new layer farm at Pendang, Kedah.

From its FY13 annual report, PW mentioned that it was developing the 2nd phase of its layer farm which was expected to be completed by early 2015. This will double its daily capacity from 420,000 to 850,000 eggs.

Thus, even with lowish ROE at 6.5%, PW can be a dark horse with very low projected PE & PB ratio, along with satisfactory dividend yield.

Anyway, its tight balance sheet & cash flow remain a risk.

Besides Teo Seng & LTKM, PW is also worth a second look.

It just made its first venture into table eggs production since 2013 with its new layer farm at Pendang, Kedah.

From its FY13 annual report, PW mentioned that it was developing the 2nd phase of its layer farm which was expected to be completed by early 2015. This will double its daily capacity from 420,000 to 850,000 eggs.

Thus, even with lowish ROE at 6.5%, PW can be a dark horse with very low projected PE & PB ratio, along with satisfactory dividend yield.

Anyway, its tight balance sheet & cash flow remain a risk.

We can assume confidently that chicken & eggs price will only rise in the future. However, cost of energy, raw material and man power will rise as well.

I think corn and soybean price are particularly important to poultry industry, as it can fluctuate so much as shown earlier.

If corn & soybean price are to rebound furiously just like it happened in 2010, those companies' financial results will not be that pretty I guess.

Furthermore, if the raw materials for chicken feeds are imported in USD, recent weakening of RM against USD might add more pressure if corn & soybean price also go up later.

Anyway, I think investors can still anticipate good financial results from poultry operators for year 2015 at least.

Furthermore, if the raw materials for chicken feeds are imported in USD, recent weakening of RM against USD might add more pressure if corn & soybean price also go up later.

Anyway, I think investors can still anticipate good financial results from poultry operators for year 2015 at least.

As usual, investors need to study those companies in more detail. Invest at own risk.

http://bursadummy.blogspot.com/2015/01/poultry-farming-listed-companies-in.html

apini

if you are a buddhist or believe in karma , if you still have an alternative , this is definitely not your choice. not say I don't want but i dare not. you may not agree, you may think I am silly. but I just DARE NOT. the only reason

2015-01-10 19:03