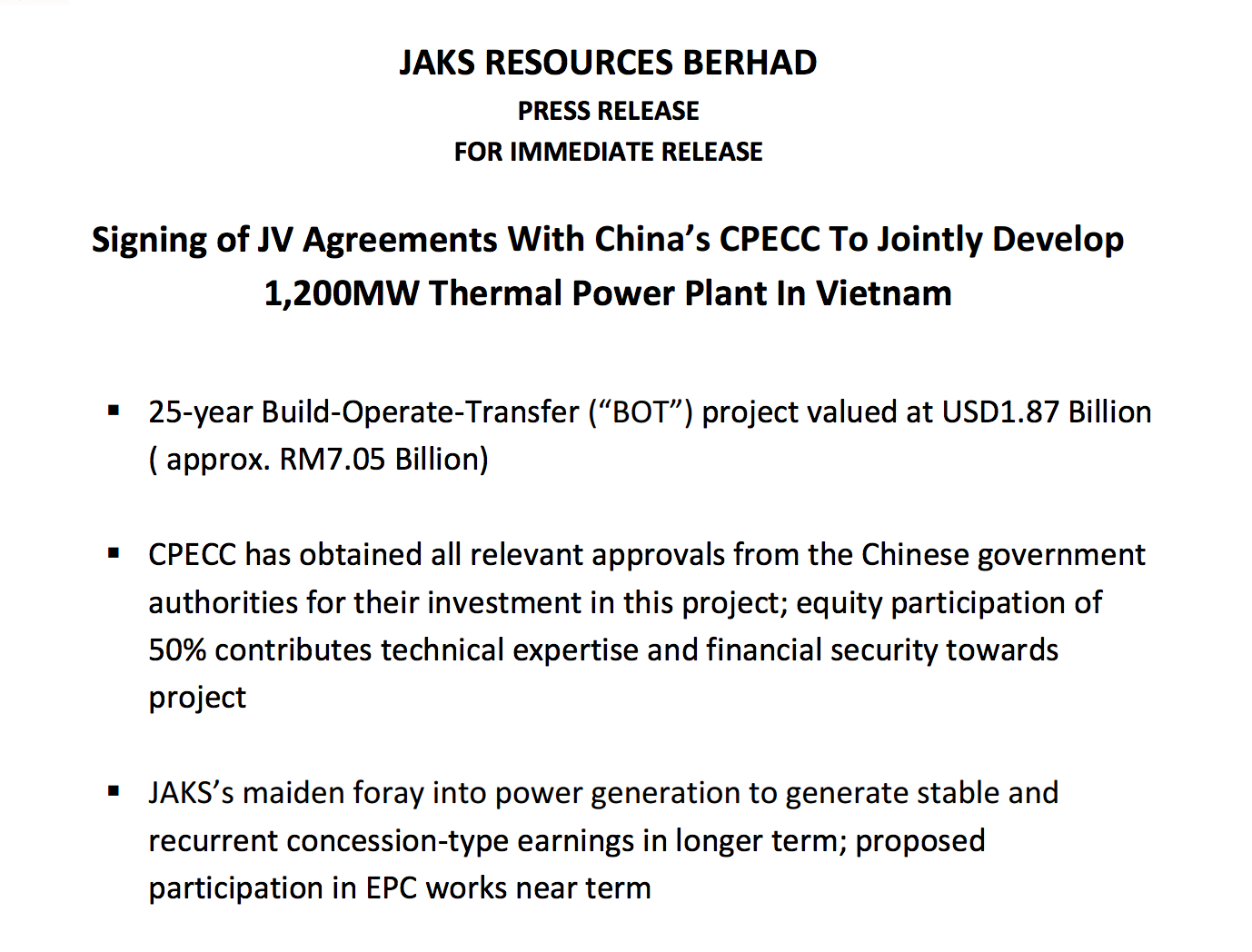

What has it gotten with the IPP in Vietnam? Basically as below, a BOT (transfer - after 25 years) project and its partner CPECC has bought into the project by funding a huge portion of it.

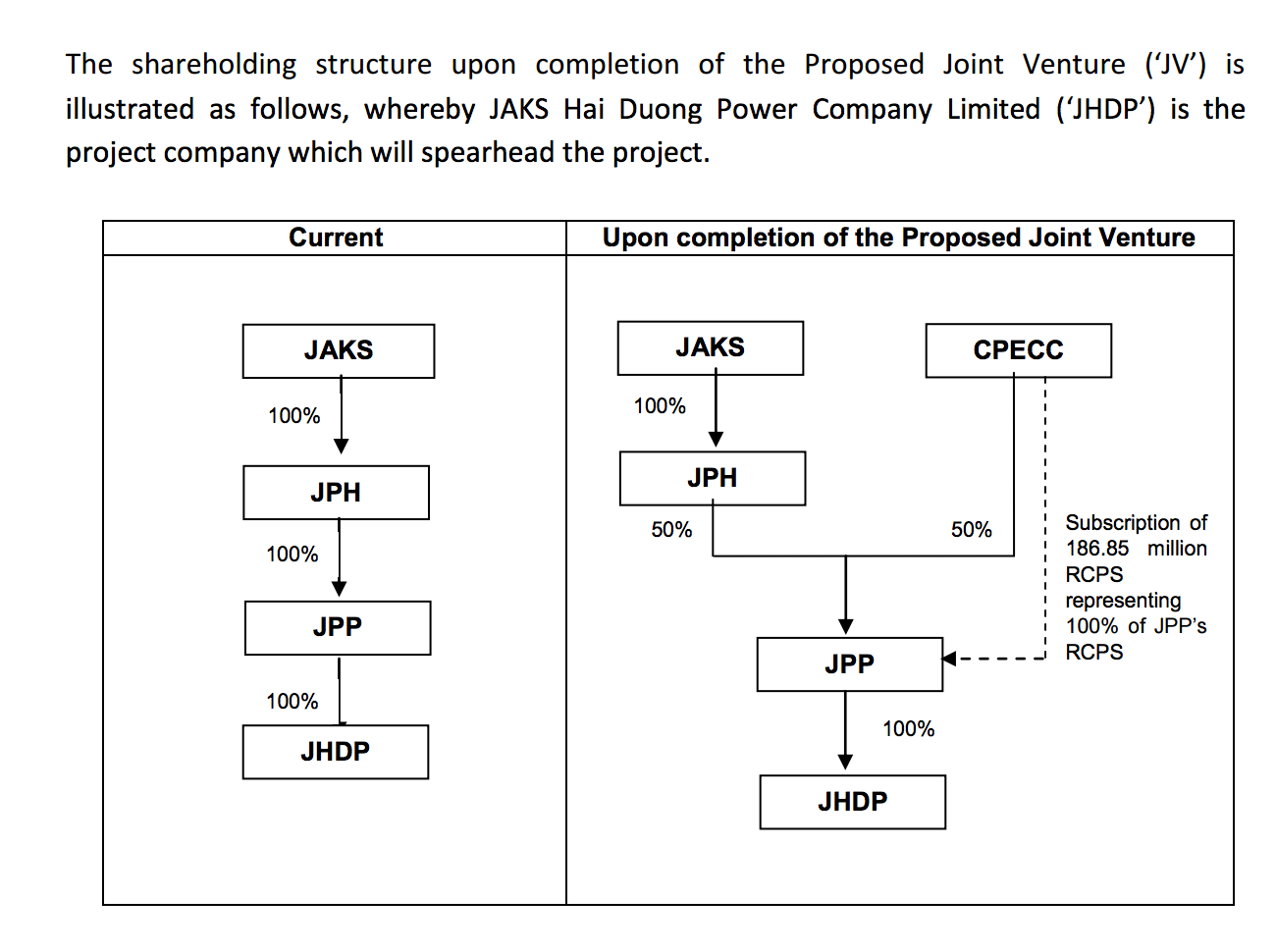

The structure is as per below:

Do I have reason to believe it can be delivered? Yes.

Do I have reason to trust the project has decent to good return? I should think so considering the interest from CPECC. It has country risks obviously, but this one sounds to be more secure.

Now, all that is good as if it is able to secure good IRR, this basically is a great investment with Jaks trading at about RM535 million valuation. (Jaks has mentioned of it eyeing at least a 10% IRR.)

With that, it is definitely not wrong for a person who understands construction to wallop - and wallop he did. Another point to note is that the controlling shareholder - Mr Ang Lam Poah only owns around 8% to 9% of the company on paper. (I would tend to think he definitely has supports from his other friendly shareholders.) What Mr Ang did wrong was that he took a long time to accumulate the shares, probably thinking of getting them at cheap - below RM1.

Seeing opportunities (probably), Mr Koon Yew Yin bought the shares in a very quick manner and in the process, accumulated more than 11% over a short period of time. (Mr Koon is now, the single largest shareholder) At the point of him becoming a substantial shareholder, it triggered the attention of Ang's group, I believe. Jaks announced an unusual quarterly 31 Dec 2016 loss and at the same time, announced that it is to do a 10% private placement.

|

| KYY's holding has increased to 11.7% by 1 March 2017 |

Can Mr Koon do much? We shall see. And I do not think he is keen to takeover anyway - as the project is for Mr Ang to lose (he is the person, whom have worked hard to pull everything together), moreover Koon is not in the right age to do that. A new management could jeopardize the project.

Mr Koon's past records have been more of a short to medium term investor - come in - make a kill and go. With that, (I would think) Mr Ang has reasons to be afraid and not to entertain much requests. The ball is in Ang's court to play and decide how to play.

(You see, if I have Warren Buffett as my shareholder, I should feel proud. But, if I have Carl Icahn as my shareholder - I would put on more defences surrounding me, because of animal instincts. In this case though, activists investing may not work well.)

Will someone like Mr Koon ask for a favourable return from the shares? Almost a surety. Why would he invests into Jaks anyway? - and this manner of buying.

The biggest question is - if Jaks current controlling shareholders do not want to play ball - the shares can be stuck at RM1.10 to RM1.30 for a long time - something that a shorter term shareholder would not want! It could end up being you buy to push up your own share price. You can buy but you cannot sell at a profit.

One thing for sure (unless with a deal being made, the private placements may not be that cheap - at least not the type of price which Ang and his group have been buying at i.e. around RM1 - and the way Mr Koon has been buying.)

This is quite interesting turns out and a lesson to note in the long term.

calvintaneng

Haha! Hahaha!

After reading felicity post on Jaks' venture into power plant for a 25 year BOT (Built- Operate - transfer) project in Vietnam I hope you silly fellas chasing Jaks will finally wake up!

A power plants needs long drawn out gestation period BEFORE you see any profit. Better go and plant durian trees.

Suddenly, Uncle Kyy has led so many punters into LONG TERM INVESTING. Wuhuhu!

I bought MFCB ( Mega First Corp Bhd or My Father Comes Back). It has taken a full 10 year to see MFCB cross from Rm1.50 to Rm2.50 & then split.

Mega First has 2 power plants - One in China & one in Tawau, Sabah.

10 years really long gestation period. In fact MFCB built those 2 power plants in year 1995 & 1996. So with concession around 22 years MFCB's time almost ripe after 20 years already!

QUESTION NOW IS?

ARE YOU GUYS WILLING TO WAIT BETWEEN 10 to 20 YEARS' Gestation Period to See Real Profits from Jaks Vietnam Power Plants?

If so

HAHAHA! YOU GUYS ARE NOW REALLY LONG TERM INVESTORS!!

HUHUHU!!

2017-03-05 16:12