Good Articles to Share

Stock Review – HAIO (7668) (HAI-O ENTERPRISE BERHAD) - IVKLSE

Saturday, 21 September 2019

Bursa Malaysia - 7668

Bloomberg - HAIO:MK

Yahoo - 7668 .kl

Webpage - https://www.hai-o.com.my/

Yahoo - 7668 .kl

Webpage - https://www.hai-o.com.my/

Company Profile

HAIO established in 1975 and has since become an establish household name offering wide range of complementary medicine (TCM), medicine tonic as well as wellness, beauty and healthcare products and clinical services. HAIO have business presence nationwide with 57 retail chain stores and franchises, 37 Multi-Level-Marketing (MLM) branches, stocklists and sales points, and 2 GMP manufacturing plants across Malaysia.

HAIO had joint venture with world renowned Beijing Tongrengtang since 2002 to offer TCM consultation services and high quality herbal medicines to public.

1) Operating Segment

HAIO consists of 3 main reporting segments as follow:

|

Segment

|

% 2019 Revenue

|

Asset Turnover

|

Return on Asset (%)

|

% 2019 CAPEX

|

|

Multi-Level-Marketing

|

68.48

|

1.59

|

33.51

|

48.57

|

|

Wholesales

|

17.96

|

0.35

|

38.13

|

27.07

|

|

Retail

|

12.35

|

1.20

|

2.73

|

2.71

|

|

Non Reportable segment

|

1.21

|

0.11

|

4.10

|

21.65

|

From 2019 annual report, Multi-Level-Marketing (MLM) segment is producing the most revenue for HAIO in 2019, 68.48 % of 2019 are from Multi-Level-Marketing segment. MLM segment had high asset turnover and return on asset hence it is not surprise most of the capital expense, CAPEX, for the year 2019 go to this segment. (48.57 % of 2019 CAPEX).

HAIO had invested RM 8,296,000, 2.53% of 2019 revenue into CAPEX. RM 1,796,000 was invest into other non-reportable segment which only generate RM 3,980,799 revenue over the year of 2019 (45% of revenue generate from others segment is invest back into the segment)

|

PROS:

|

|

è 48.57 % of 2019 CAPEX go to MLM which has high Asset turnover ratio and return of asset.

|

|

CONS:

|

|

è 21.65 % of 2019 CAPEX go to non-reportable operating segment which is not the main operating segment of HAIO

è 45% of revenue generate from non-reportable segment is invested back into the segment.

|

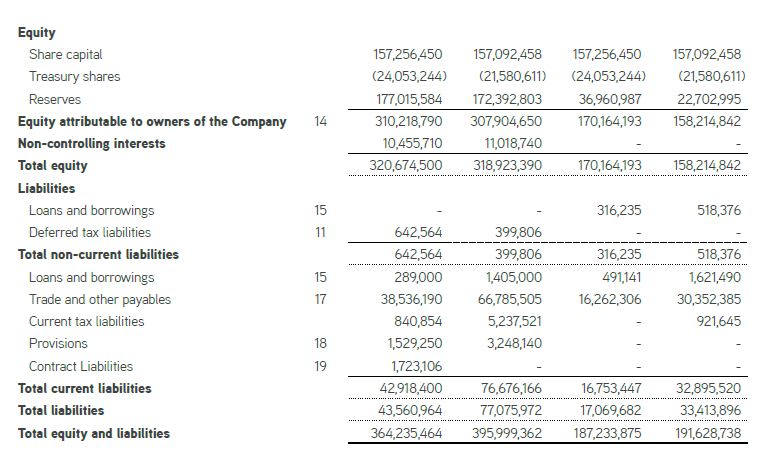

Financial Statement

HAIO investment properties had decrease from RM 55,949,690 (2018) to RM 45,658,791 (2019), 18.39 % decrease. It is mainly because the decrease in the value of the freehold and leasehold land held by HAIO. However the net rental income had increase from RM 1,640,616 to RM 2,723,831, 66.02% increase.

The trade and others receivable of HAIO has decrease from RM 31,951,966 to RM 21,783,945, 31.82% decrease and the trade receivable past due also decrease from RM 3,257,059 to RM 2,180,565, 33.05 % decrease. The decrease of the trade and others receivable is mainly due to the decrease in sales from RM 461,969,489 to RM 328,406,809, 28.91% decrease in sales.

HAIO cash and cash equivalents had also decrease from RM 68,674,442 to RM 53,792,063, 21.67% decrease.

|

PROS:

|

|

è 66.02% increase of net rental income.

|

|

CONS:

|

|

è 28.91% decrease in revenue.

è 21.67% decrease in cash and cash equivalents

|

HAIO had low loans and borrowing which is RM 289,000 in 2019. In 2019 HAIO had contract liabilities which is revenue recognised overtime during the membership period expected to recognised as revenue over the perios of 3 years to 1 years.

|

PROS:

|

|

è HAIO had low loans and borrowing

|

Financial Ratio

|

Description

|

2019

|

2018

|

Different

|

|

Gross Profit Margin

|

0.38

|

0.35

|

+0.03

|

|

Net Profit Margin

|

0.14

|

0.16

|

-0.02

|

|

Interest Coverage Ratio

|

578.56

|

808.87

|

-230.31

|

|

Effective Tax

|

0.25

|

0.25

|

0.00

|

Warrant

No Warrant issue

Dividend and Bonus Issued for the past five year

HAIO had constant dividend for the past five year from 2014 – 2018 with the average of RM 0.14 with the dividend yield of 5.56 % base on HAIO stock price of RM 2.52 on 21/9/2019.

|

PROS:

|

|

è HAIO had dividend yield of 5.56 % for the past five year which is higher than fixed deposit of 3.00%

|

|

|

Market Research

Affin Hwang Capital (26 June 2019)

Price Target : RM 1.80

- Incentive trip campaign failed to revitalise MLM sales

JX APEX Security Bhd (26 June 2019)

Price Target : RM 2.24

- MLM division - business environment remain challenging

- Wholesale division – focus on core products

- Retail division – continuous expansion

KENAGA Investment BankBerhad (26 June 2019)

Price Target : RM 1.95

- Pressure from stagnant distributors’ growth

- Weakening of MYR against RMB

Estimated Price

IVKLS Price : RM 1.53

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Good Articles to Share

Thai baht down as bullion loses shine; Singapore dollar slips post inflation data

Created by Tan KW | Nov 25, 2024

One dead, three hurt as DHL cargo plane crashes into house near Vilnius airport

Created by Tan KW | Nov 25, 2024

South Korea's Yoon, Malaysia's Anwar agree to cooperate in defence, minerals

Created by Tan KW | Nov 25, 2024

South Korean opposition leader cleared of forcing witness to commit perjury

Created by Tan KW | Nov 25, 2024

Discussions

Be the first to like this. Showing 3 of 3 comments

Post a Comment

Featured Posts

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-11-25 16:50:00

ADX

10 Mins

SELL

2024-11-25 16:20:00

EMA 5

10 Mins

SELL

2024-11-25 16:20:00

EMA 5

5 Mins

SELL

2024-11-25 16:20:00

ADX

5 Mins

SELL

2024-11-25 16:20:00

TURTLE SYSTEM 20

5 Mins

SELL

Apps

Top Articles

1

2

3

Good Articles to Share

4

Good Articles to Share

What’s behind the slew of restaurant bankruptcies in 2024? Experts unpack the problems

5

Good Articles to Share

Four convicted in Spain over homophobic murder that sparked nationwode protests

6

Good Articles to Share

7

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Taehyung

TP=1.53 ? already $2.50 lah !

The coming Qtr result is expected to be good..

2019-09-21 21:16