Amazing Race

[ APB Resources ] Gaining Strength

NickCarraway

Publish date: Thu, 27 Mar 2014, 01:01 AM

NickCarraway

0 21

DISCLAIMER :The information in this research has been obtained from sources believed to be reliable.Its accuracy, completeness or correctness is not guaranteed and opinions are subject to change without notice.This research is for information purposes only and not to be construed as a solicitation for contracts.The writer accepts no liability for any direct or indirect loss arising from the use of this research. The writer may have an interest in the securities of the company(ies)mentioned here

Summary:

- APB Resources is a well established process equipment fabricator with impressive continuous operating profit track record.

- Since last surge in demand for process equipments during 2006 to 2008, APB Resources has doubled up its production capacity to ride on the next boom cycle.

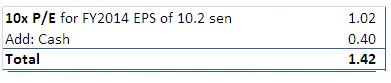

- Based on its constant profit track record and huge cash pile of RM0.40 per share, APB Resources should be fairly priced at RM1.42 which provides 20% upside from its last price of RM1.18.

- With estimated annual 6.5sen dividend per share, current share price offers a decent 5.5% dividend yield.

Introduction Listed on the Main Board of Bursa Malaysia via the Reverse Take-Over exercise of NCK Corporation Bhd in 2004, APB Resources is an investment holding company with 2 principal activities:-

(i) Manufacturing of process equipments for oil & gas, petrochemicals, oleochemicals and power industries.

(ii) Non-destructive testing (NDT) services.

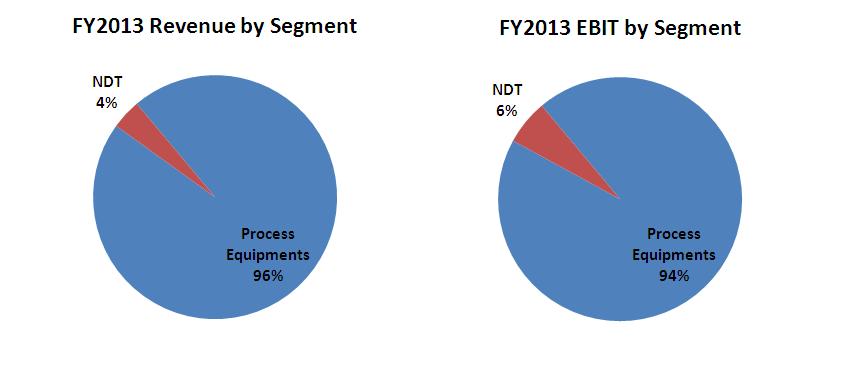

Its process equipment manufacturing business is the key earning driver, accounting for 96% and 94% of APB Resources revenue and EBIT in FY2013. Complementary business of NDT services plays a secondary role to its earnings.

Well Established Name in Process Equipment Manufacturing. With over 30 years of experience in process equipments, APB Resources has cultivated lengthy relationships with large companies around the world, with client base ranging from petrochemical, chemistry, oil palm processing, paper mill to power generation industries.

Its business is also supported by strong in-house design and engineering capabilities which tailor makes its products to suit client specifications and requirements. Products manufactured by APB Resources range from normal carbon steel to exotic material such as incoloy, inconel, monell, hastaloy and high chrome nickel alloys used for exchanger and process equipment, to requested sizes and weight up to 1,000 MT per unit.

Although APB Resources has the capability to fabricate a wide range of process equipments, its strength is in the design and engineering of pressure vessels. Pressure vessels comprise equipment that makes up the backbone of any processing plant, performing such vital functions as separation, distillation and conversion.

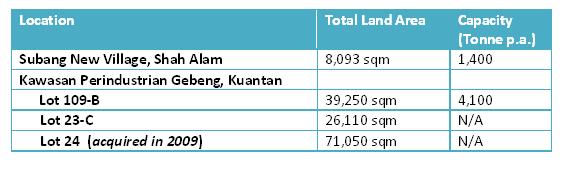

Progressive Expansion. APB Resources has 2 fabrication plants where one is in Subang New Village, Shah Alam and another in Gebeng, Kuantan.

In 2006, it entered into a JV agreement with PSC Petroleum Sdn Bhd (PSC) to operate an additional 10 acre yards with equipment in Pulau Jerejak to cater for its process equipment operations. However, the JV didn’t materialise as PSC went thru restructuring exercise undertaken by its new shareholder Boustead Holdings. PSC was subsequently incorporated into Boustead Heavy Industries Corp Bhd (BHIC) that was relisted in 2007.

Despite the setback in securing easier access to the sea in the JV with PSC, APB Resources opted for expansion near its own facilities. APB Resources managed to double its yard space from 18 acres in 2006 to around 36 acres currently.

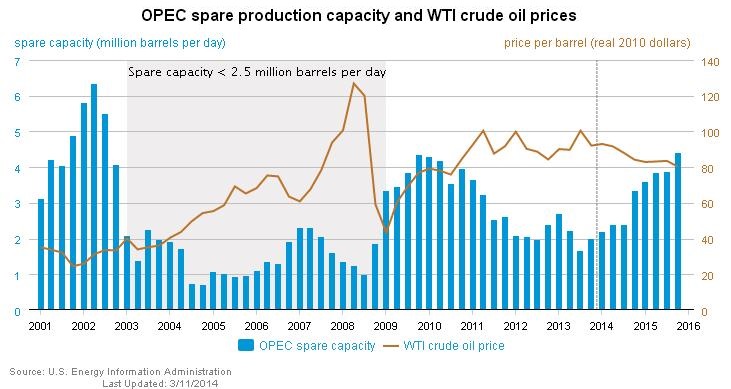

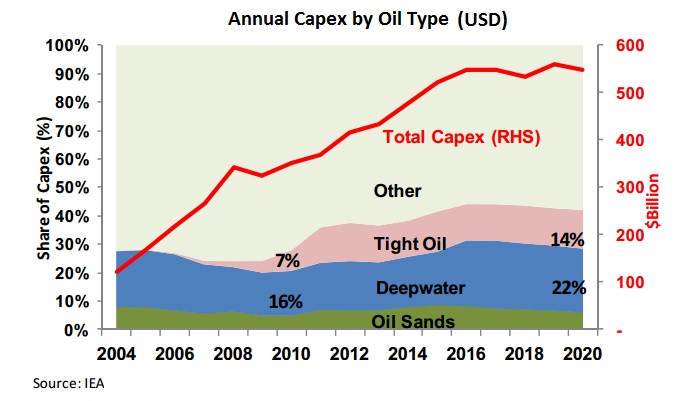

Prepared for the next Boom Generally, OPEC spare capacity provides an indicator of the world oil market's ability to respond to potential crises that reduce oil supplies. Such low OPEC spare capacity level (chart below) shall require continuous capex spending (chart below) in order to ensure adequate supply meeting global oil demand. In such instance, fabricators will benefit first from capex spending by oil majors via order flows compared to other service providers.

In addition, APB Resources management shares the view that demand from power and oleochemicals sector shall be positive for process equipments market. Given the capital spending spree and increasing demand for process equipment globally, the spill-over effect is positive for companies in the process equipment fabrication sector.Since the last boom in demand for process equipments during 2006 to 2008, APB Resources is now ready to ride on the next boom after doubling its production capacity in 2009.

Healthy Orderbook. APB Resources outstanding orderbook is estimated to range between RM100 million to RM150 million at any one point which would last 6 to 9 months, of which 90% are from overseas. Fuelled by increasing demand for process equipments, APB Resources should enjoy strong orderbook over the next 3 to 5 years and be able to build up and sustain revenue of at least RM150 million per annum.

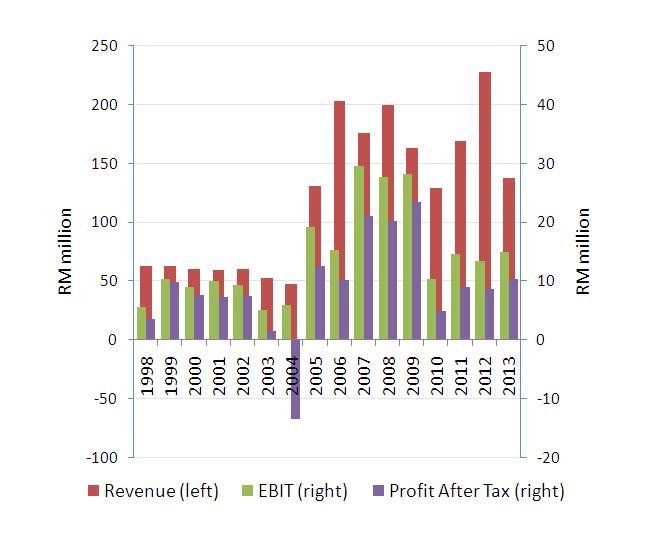

Impressive Profit Track Record. Since 1998, APB Resources displayed continuous profit track record with the exception of FY2004 due to the need to absorb the losses of NCK Corporation Bhd in order for APB Resources to assume NCK Corporation Bhd’s listing status.

Chart: Revenue & PAT FY1998-FY2014

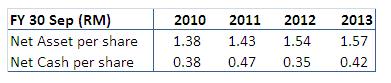

Huge Cash Pile. Arising from high demand for pressure storage vessels and heat exchangers, such astonishing profit track record allows APB Resources to build up cash holdings over the years. The cash per share was RM0.40 per share as at end 2013.

Table: NA & Net Cash per share FY2010-2013

The reason for holding on to such huge cash pile is not clear. It might be due to its high criteria in evaluating any potential expansion that could contribute to its bottom line. Also, it remains unclear if APB Resources would decide to distribute the excess cash back to shareholders. Otherwise, the huge amount of cash could also be readily available for APB Resources to privatise the company easily.

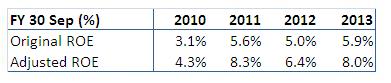

Low Profile. The stock is not noticeable by most investors as the large cash pile distorted its effective capital structure and thus led to lower Return on Equity (“ROE”). If cash was excluded from its capital, the adjusted ROE will normalise closer to its regional peers.

Table: Original vs Adjusted ROE FY2010-2013

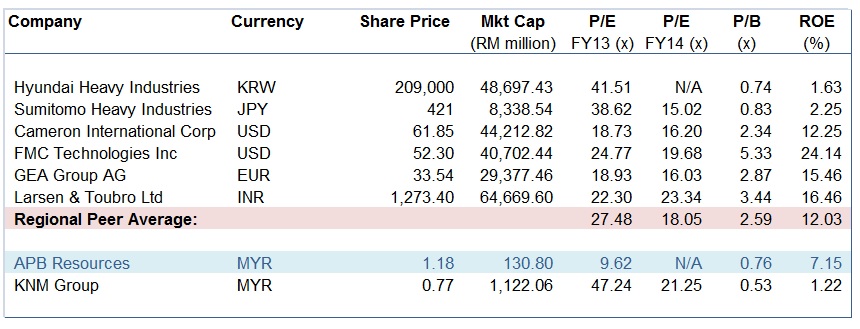

Table: Peer Comparison

1Q2014 Results. The recently announced 1Q2014 results as at end Dec 2013 of APB Resources reported that it has completed a number of high value but relatively low margin projects with revenue recorded at RM58.0 million (4Q2013: RM37.5 million). It continued to chalk up good Profit Before Tax (PBT) posting RM5.4 million (4Q2013: RM5.2 million) partly boosted by forex transaction gain of RM2.1 million (4Q2013: RM1.6 million).

Attractive Valuation. On a conservative basis, assuming forex were to stabilize in subsequent quarter without any profit contribution to APB Resources, it should be able to achieve PAT of RM11.5 million or EPS of 10.2 sen for FY2014.

Based on its constant profit track record and huge cash pile, APB Resources should be fairly priced at RM1.42 which provides 20% upside from its last price of RM1.18. While APB Resources doesn’t state its dividend policy but based on historical trend, its annual dividend per share was around 6.5sen.

Value per share

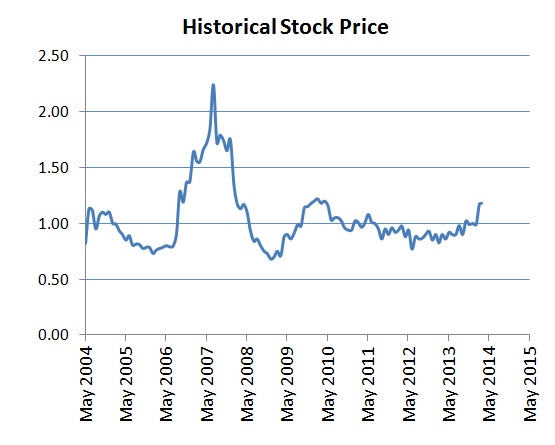

The stock is tightly held by major shareholders (55%) together with Tabung Haji (8%) and has low liquidity. It will be suitable as medium to long term investment with decent dividend yield of 5.5% underpinned by its high net cash position.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Amazing Race

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

THE INVESTMENT APPROACH OF CALVIN TAN

2

My Trading Adventure 2025

3

My Trading Adventure 2025

4

All Official Update

5

Bursa Stock Talk

6

Readers' Digest MY

Japan’s Telecommunication Boom: Innovation, Growth & the Future

7

My Trading Adventure 2025

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....