Amazing Race

[ UPA ] a unique paper products producer

NickCarraway

Publish date: Tue, 01 Apr 2014, 12:13 AM

NickCarraway

0 21

DISCLAIMER :The information in this research has been obtained from sources believed to be reliable.Its accuracy, completeness or correctness is not guaranteed and opinions are subject to change without notice.This research is for information purposes only and not to be construed as a solicitation for contracts.The writer accepts no liability for any direct or indirect loss arising from the use of this research. The writer may have an interest in the securities of the company(ies)mentioned here

[ UPA ] a Unique PAper products producer

Last Price: RM1.41

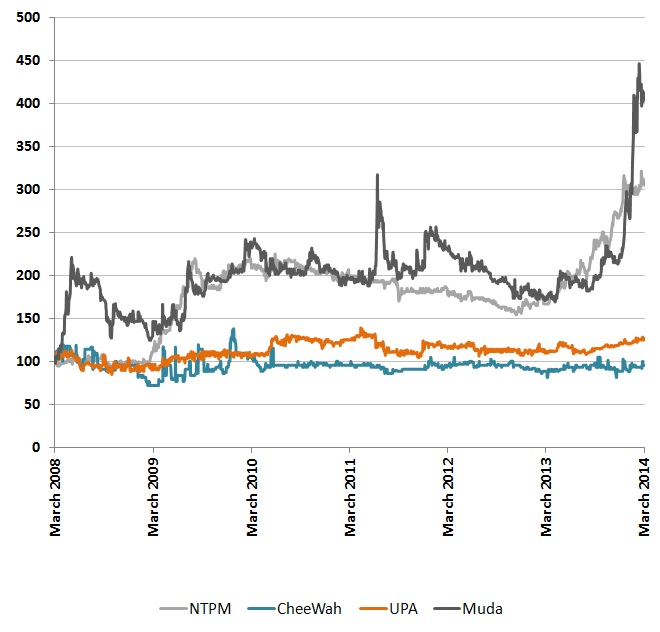

Sector Laggard Since a year ago, there are 2 paper products producers that have outperformed the market. They are Muda Holdings Bhd (‘Muda’) and NTPM Holdings Bhd (‘NTPM’).

In terms of laggard in this segment, UPA Corporation Bhd (‘UPA’) is less known to investors. It has its niche position in terms of stationery market. Besides being the leading printer of diaries in Malaysia, UPA manufactures plastic stationery products, recondition printing and binding machines, produces PET and PVC shrink films.

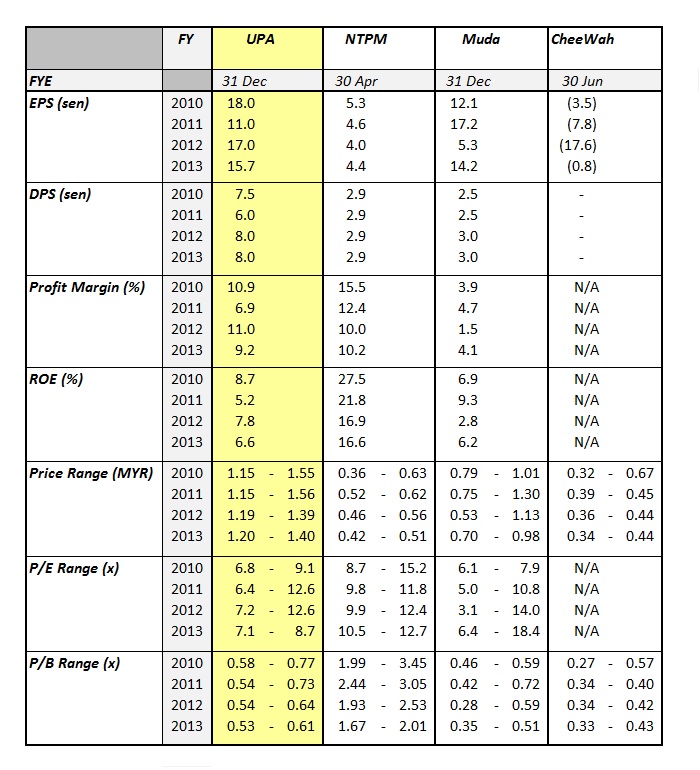

Healthy Earning The earning profile of UPA is comparable to Muda (in terms of ROE) and NTPM (in terms of profit margin). However, despite posting healthy earning, UPA’s share price performance has been flat and investors are treating it like another loss-making paper products producer, Chee Wah Corporation Bhd (‘Chee Wah’).

Attractive Value Based on simple calculation and its historical record, UPA should achieve EPS of 15sen with ease in FY2014.

By pegging at conservative P/E of 10x (which is at 15% discount to Muda’s T12M P/E of 12x and upto 40% discount to NTPM T12M P/E of 16.9x) and adding net cash of 27sen, UPA should be fairly valued at RM1.77 (10 x 15sen plus 27sen) which gives 25% upside from last price of RM1.41.

Current share price also provides attractive dividend yield of 5.7% and trades at nearly 40% discount to its last book value of RM2.32 per share.

Relative Performance of Selective Peers (base 100 at Mar 2008)

Comparative Valuation

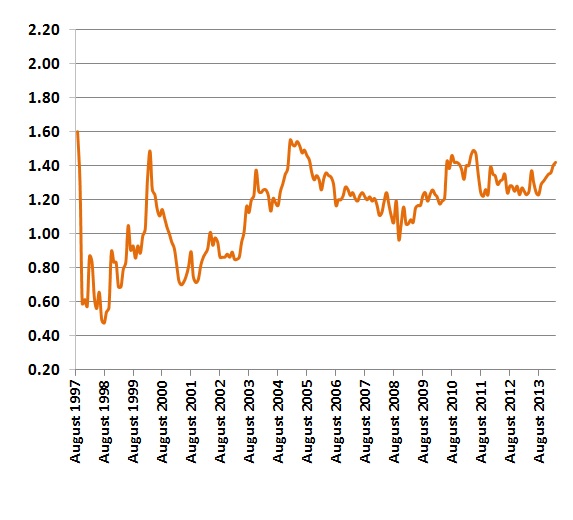

Historical Share Price of UPA

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Amazing Race

Discussions

Be the first to like this. Showing 1 of 1 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

2

save malaysia!

3

BFM Podcast

4

BFM Podcast

5

BFM Podcast

6

BFM Podcast

7

BFM Podcast

8

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Blue Sky

good write up.. have been holding upa for the dividend too... dy with 6% good return... they are still undervalue.. tp 1.60.. with strong earnings and sales for past 5 years..

2014-04-01 19:09