Scientex Bhd

Winners Of Lower Commodity Costs

ss20_20

Publish date: Tue, 04 Nov 2014, 01:46 PM

ss20_20

0 155

坚守长期价值投资, 催化复利累进效应, 实现财务自主与享受写意人生

Value Investing & Joys of Compounding

___________________________________________________________________

ss2020 - Blog Title List | 目录:

http://klse.i3investor.com/blogs/ss2020_List/

____________________________________________________________________

以下纯粹个人投资收集与记录,且本人非专业分析员,买卖亏盈自负。

The articles here solely the collection or opinion of the author and do not represent professional advice in investment

Value Investing & Joys of Compounding

___________________________________________________________________

ss2020 - Blog Title List | 目录:

http://klse.i3investor.com/blogs/ss2020_List/

____________________________________________________________________

以下纯粹个人投资收集与记录,且本人非专业分析员,买卖亏盈自负。

The articles here solely the collection or opinion of the author and do not represent professional advice in investment

We foresee an extended period of soft prices of energy-related and other selectedcommodities, which will benefit key sectors such as utilities, aviation, plastic packaging manufacturers and construction. Key beneficiaries which rank among our top picks are Tenaga, Gamuda, as well as Air Asia, while other notable cheap beneficiaries include Scientex.

WHAT’S NEW

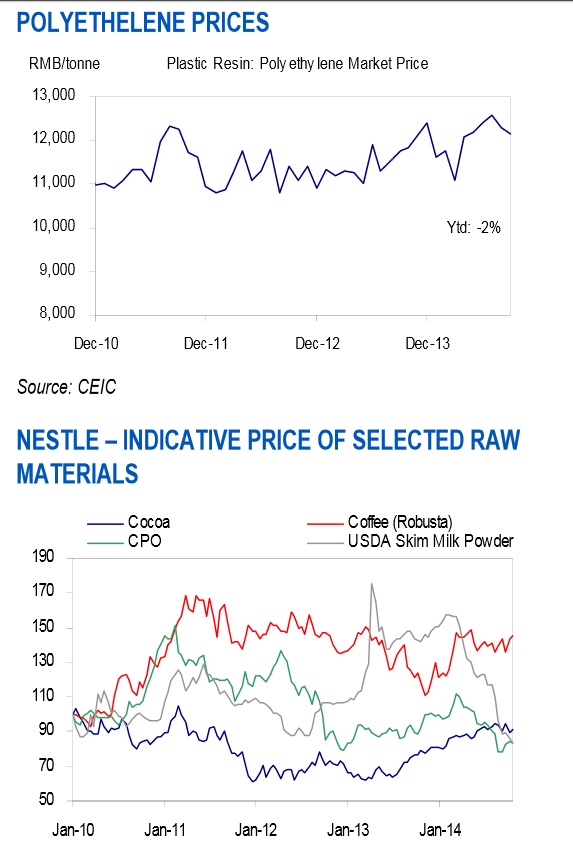

An extended period of price weaknesses for energy-related costs. Industrial commodity prices are down 5% ytd and 8% from this year’s peaks, while selected soft commodities have retreated by 12% from this year’s peak. In particular, the energy-related commodities – coal (-16% ytd) and crude oil (-22% ytd) - are likely to remain soft for the foreseeable future. Accompanying the lower energy prices is the fall in the global utilisation rates in the petrochemical industry, which points to lower plastic resin costs. In addition, international prices of steel are expected to remain in the doldrums.

Key beneficiary sectors – utilities, plastic packaging manufacturers, aviation and construction. Qualifying sectors need to fulfil two criteria:

a) benefit from lower commodity prices, and

b) good demand and revenue visibility (which eliminates cyclical sectors) and decent pricing power.

Apart from benefitting from falling input costs, some of these sectors also feature high revenue growth visibility, with the utilities and construction sectors enjoying firm domestic demand, and the regionally-oriented plastic packaging manufacturers servicing the relatively stable FMCG sector.

Scientex (NOT RATED) is a key beneficiary of declining plastic resin prices and is aggressively ramping up its production capacity in the consumer packaging segment with a RM300m expansion programme that will quadruple its capacity by 2017. Pegging the stock at 10x FY16 consensus PE, it would be valued at over RM8.80.

Plastic packaging manufacturers (notably, Scientex and Daibochi) will benefit from lower plastic resin prices (which are closely correlated to crude oil prices). Plastic resin, which accounts for 60-80% of their cost, has come off 3-5% in the last three months. In particular, we expect the consumer packaging operations to significantly benefit from lower plastic resin cost (given the operation’s modest margins) even after the producers pass on most of the cost savings under ‘cost-plus’ revenue model.

We like Scientex (NOTRATED), which will quadruple its consumer packaging capacity in 3-years. Its manufacturing division is poised to deliver 15-20% revenue CAGR over FY14-17. Meanwhile, although Daibochi recorded weak 3Q14 financial results, management is upbeat on the 2015 outlook with 15-20% top-line growth, underpinned by stronger sales to existing and new customers, as well as margin improvement from lower resin and electricity costs (after its recent installation of electricity-saving equipment). However, not all companies will benefit, eg SKP Resources fully passes on the raw materials savings to its key clients and will see aneutral impact from the fall in resin price.

The fast moving consumer goods (FMCG) sector is only a minor net beneficiary of easier commodity costs as some soft commodities have trended higher this year (see Nestle’s raw materials price chart overleaf). Nonetheless, the softer commodity costs allow for some margin improvement, and help stimulate demand as some cost savings will be passed on to consumers. While the glove industry may also be also a minor beneficiary thanks to declining nitrile prices, the build up in excess industry capacity may force producers to fully pass on cost.

To a lesser extent, the consumer sector is a beneficiary from a decline in selected input costs,although we note that not all soft commodity prices have retraced in recent months, with coffee (+16% ytd) and cocoa (+6% ytd) up sharply this year. That said, palm oil prices are down 12% ytd while indicative milk solids prices are at their lowest levels in over four years, and these has helped to lift Nestle Malaysia’s margins by 2.2ppt to 17% in 3Q14. We recently upgraded the stock to a HOLD (Target: RM62.36) due to its market leadership in the FMCG sector (enabling it to capitalise on resilient domestic demand) as well as decent dividend yields which will gain traction in 2015, but note its expensive valuations, trading at >25x 2015F PE.

UOB Kay Hian 04 Nov 2014

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

2024-11-24

SCIENTX2024-11-19

SCIENTX2024-11-18

SCIENTX2024-11-14

SCIENTX2024-11-14

SCIENTX2024-11-14

SCIENTX2024-11-14

SCIENTX2024-11-13

SCIENTX2024-11-13

SCIENTX2024-11-13

SCIENTX2024-11-13

SCIENTX2024-11-13

SCIENTX2024-11-13

SCIENTX2024-11-13

SCIENTX2024-11-13

SCIENTX2024-11-13

SCIENTXMore articles on Scientex Bhd

Scientex - Corporate Presentation 1Q16 | Corporate Update & Financial Results

Created by ss20_20 | Dec 23, 2015

Scientex - To buy Germany's Mondi unit for RM58m in expansion plan

Created by ss20_20 | Aug 06, 2015

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

2

3

4

save malaysia!

Visa-free travel to China extended for Malaysians to 30 days

5

6

Koon Yew Yin's Blog

CPO price is rising rapidly as shown by chart below - Koon Yew Yin

7

Axcapital's investment blog

KAB - Executing its way to a record quarter. Could more Petronas contracts be coming?

8

save malaysia!

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....