Wizard of Finance

Sime Darby demerger - a revisit

wizard_of_finance

Publish date: Sun, 10 Dec 2017, 12:14 PM

wizard_of_finance

0 10

A systematic approach to financial literacy. Making the world of wall street accessible to the man on the street

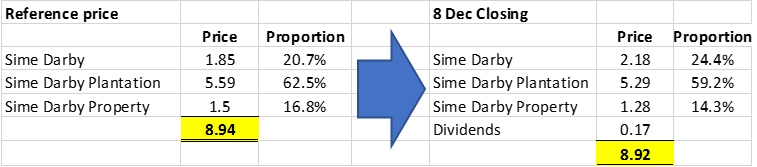

Let us quickly revisit the case analysis of the Sime Darby demerger. In our first posting

(link here: https://klse.i3investor.com/blogs/wiz_of_finance/140175.jsp), we mentioned that the plunge in share prices in the first day of trading was the result of:

1) The misallocation of value based on the reference price, especially given the dividend

2) Panic selling among shareholders of Sime Darby Property and Sime Darby Plantation

We maintained that the fundamentals of Sime Darby remained unchanged before the re-listings and hence the total share prices should not drop. After a period of irrationality, the price of all three Sime Darby related counters finally retraced to approximately the same price before the re-listings as below. This is as per what we expected.

So..what’s next?

Again, we stand by our opinion that SDPlant would be the counter with the most short term potential as per our posting here https://klse.i3investor.com/blogs/wiz_of_finance/140696.jsp.

With more visibility over the earnings of the individual companies, we opine that SIMEPLT is the most stable blue chip counter among the 3 counters and still have some upside to go when a relative valuation comparison is done among its peers. We also opine that SIMEPROP also has upside potential but given the weak property sentiment at this time, in the short term, there should be some volatility.

Disclaimer: This is not a buy call. Please do your own research before investing.

Cheers,

Wiz_of_Finance

If you are interested in contacting me for more analysis, please contact me at wiz.of.finance@gmail.com

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Wizard of Finance

Orion IXL - Run or punt (update after small and mid cap pullback)

Created by wizard_of_finance | Jan 21, 2018

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

Mercury Securities Research

2

Stock Market Enthusiast

3

THE INVESTMENT APPROACH OF CALVIN TAN

4

5

Phillip Capital Research Reports

6

save malaysia!

7

Good Articles to Share

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....