Insas Undervalued?

Insas Undervalued?

Insas undervalued?

Insas Berhad (Insas) is engaged in the investment holding and the provision of management services. The Company operates in the five segments:

1)financial services and credit and leasing include stock broking and dealing in securities, credit and leasing and granting of loans and other related financing activities.

2)property investment and development include property development and property holding.

3)investment holding and trading include investment holding and trading of securities

4)retail trading and car rental include cars and limousines for hire/rental.

5)information technology related services include wireless microwave telecommunication products, and wireless broadcast card and electronic manufacturing services.

Look at business segments above, I am a bit dizzy. Can't find a suitable word to describe it, maybe can considered 'rojak' conglomerate of Malaysia.

Let's go to their lastest Q317 of the company.

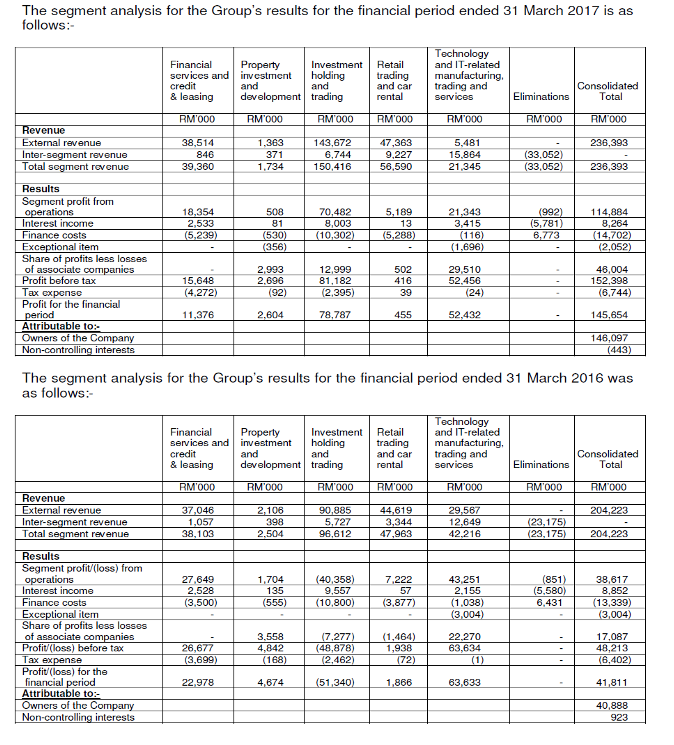

Financial services and credit & leasing division

The unit reported lower pre-tax profit of RM15.6 million for the nine months period ended 31

March 2017 (nine months period ended 31 March 2016: RM26.7 million) due to lower gain on

fair value changes of financial assets at fair value through profit and loss of RM0.4 million in the

current period (nine months period ended 31 March 2016: gain on fair value changes RM9.8

million).

With my limited knowledge on accounting, I guess this division involved in financial services that holding some financial assets that value quite volatile(securities?). Company will determine the value of the financial assets in the end of some period. M&A Securities S/B-Stock broking firm in this segmen? If compare to last financial year this segment not that impressive.

Property Investment and development

No explanation for this segment on Q317 report. Maybe the contribution from this segment is too small to bring any significant impact. (Hop Hup Construction Berhad in this segment?)

Investment holding and trading division

The investment unit reported higher revenue of RM143.7 million for the nine months period

ended 31 March 2017 as compared to revenue of RM90.9 million reported in the preceding

year’s corresponding period as a results of higher trading activities in the current financial

period.

The investment unit reported pre-tax profit of RM81.2 million for the nine months period ended

31 March 2017 (nine months period ended 31 March 2016: pre-tax loss of –RM48.9 million)

primarily due to gain on fair value changes of financial assets at fair value through profit and

loss of RM30.4 million and gain on foreign exchange of RM14.5 million (nine months period

ended 31 March 2016: loss on fair value changes of –RM42.0 million and loss on foreign

exchange of –RM16.8 million).

To me this is also another hard to understand segment. From the result, for the past 9 months this segment made the most profit compare to other segments. I suspect this segment involved in trading the securities including the subsidiaries and associate companies. This segment profit comes form the gain of fair value of financial assets and foreign exchange.

Retail trading and car rental

No explanation for this segment also. Maybe the contribution from this segment is too small to bring any significant impact on the profit for this financial period.

Technology and IT-related manufacturing, trading and services division

The Technology unit reported lower revenue of RM5.5 million for the nine months period ended

31 March 2017 as compared to revenue of RM29.6 million reported in the preceding year’s

corresponding period as a results of lower trading activities in the current financial period.

The Technology unit reported a lower pre-tax profit of RM52.5 million for the nine months period

ended 31 March 2017 as compared to RM63.6 million in the preceding year corresponding

period due to lower gain on disposal of shares in an associate company of RM31.1 million (nine

months period ended 31 March 2016: gain on disposal of quoted securities of RM9.3 million and

gain on disposal of shares in an associate company of RM38.0 million) and loss on foreign

exchange of -RM2.9 million (nine months period ended 31 March 2016: gain on foreign

exchange of RM1.0).

The Group’s equity accounting for Inari Amertron Group’s after-tax profit for the nine months

period ended 31 March 2017 was RM31.4 million (nine months period ended 31 March 2016:

RM22.7 million).

Another hard to understand segment. Lower revenue due to lower trading activities? Can it be lower trading activities from associate companies like Numoni, J&C...

This segment also involved disposal of shares in an associate company (company name not stated).

The only thing I can confirm is Inari Amertron Group’s after-tax profit for the nine months period ended 31 March 2017 was RM31.4 million

In my opinion, Insas is an asset management company that operate in such a way like our mini EPF manage a pool of funds, do quite a lot of securities trading. On the same time the company also owned some money making subsidiaries and associate companies like M&A Securities, Inari Amertron, Ho Hup, Melium Group (fashion), DOME cafe (F&B)...etc

SO WHAT IS THE CATCH HERE?

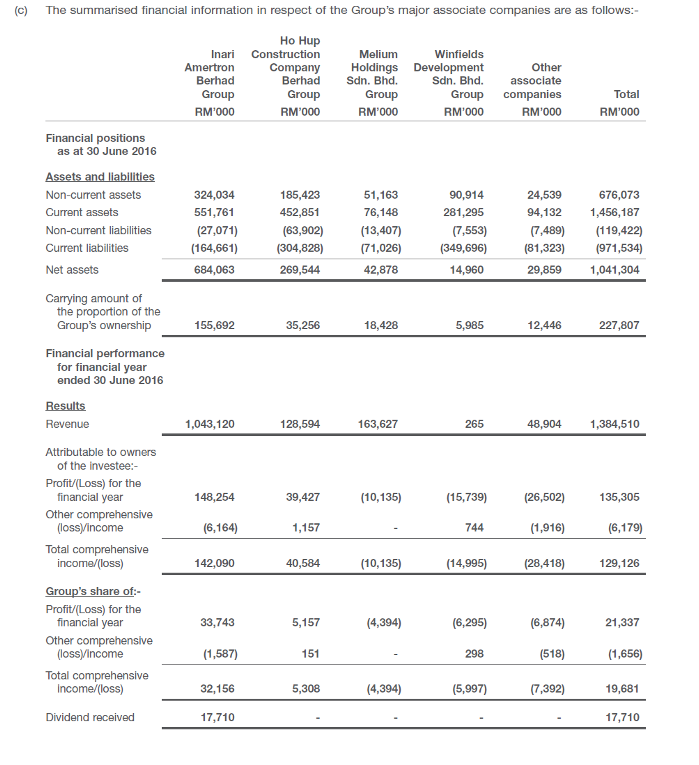

From 2016 AR below, we can see no adjustment on associate companies valuation.

In 2016 AR, 22.7% of Inari with carrying amount RM156m only, but today market value is RM964m

Let's say the management want to sell off some of the associate companies tomorrow, I assume:

-

If the company still holding 17% (instead 22%) of Inari Amertron, the market value is RM722m

-

if the company still holding 13% of Ho Hup, the market value is RM39m

Now what will happen to the company cash per share

Personally, my estimation of the company net cash at least RM500m.

cash per share = RM500m + RM761m = RM1261m/663m = RM1.91 per share

How about the NTA, if the company reevaluate some associate companies values?

With some minor adjustment I will add in RM621m (from Inari and Ho Hup)

NTA = RM2.30 + RM0.93 = RM3.23 per share

To me, Insas is kind of asset play company (deep in value) with grow potential, but hard to understand asset management business due to lack of information provided.

***caution, above writing is my own imagination and all the assumption and estimation without any concrete evidence, strictly for sharing purpose, not a buy or sell call of the company.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Discussions

4 people like this. Showing 33 of 33 comments

@con, maybe you can help me, i wrote it out to hope that someone out there might enlighten me with some answer because i can't find much info in the financial report. as i said, the catch is due to rich in cash and assets (the reason i bought the stock)

2017-07-05 20:00

if the company business related heavily on dealing with securities, as for the past 6 months due to bursa stocks rally, imo the company should do well in the coming quarter

2017-07-05 20:11

the author trying to say is, i dont know how their management works? BUT IT IS UNDER VALUED!

2017-07-05 20:18

If you go through the comments of Insas main forum for the past six months you will have a clear understanding about Insas business and operations.

2017-07-05 20:24

Author must be newbie in stock market. Insas undervalued for so many years now only you come out and write?

2017-07-05 20:35

not really, i'm in the market more than 20 yrs, not active in any forum, insas not in my radar for the past few years only recently, i found it superb potential

2017-07-05 20:44

bro... if u have more than 20 years, then i have more than 100 years, if u experienced or no we knew it straight

2017-07-05 20:49

if u have more than 20 years old, u will not write an article without understanding and say it is under valued, inari dividen provide them a lot of eps

2017-07-05 20:49

if u Handsomeeeeeeeeeeeeeeeeeeeeeeeeeeeeeeeeeeeeee, y afraid of genting ahmoi???

kekekekekkeek

2017-07-05 20:51

Hmmm yar jokers vrinkiking, cranking..gove wltan a break. He just want komen only. Personally, from presentation In as is just lucky making money from trading. IMO, management are not good managers, making money from gambling. Property ddevelopment , car rental and leasing not making money. Somethings not right. If management working.hard to fix the loopholes, let it be shown in the results. I pass this one. Good luck to all holders of Insas.

2017-07-06 05:03

If can still talk cock,that mean the traders r not badly burned, only kena surface areas. Another word still OK. In such scenario, I believe the market will continues its bull trend.

2017-07-06 09:56

If you don't understand accounting you are in the wrong biz. Please try something else and good luck.

2017-07-06 10:26

Insas is extremely overvalued for a company that don't know what it wants to do. If the main selling point of Insas is that it own shares in Inari then may as well go buy Inari. Buy Insas you get Inari but also come with whatever other nonsense investments. Of course if Insas dispose shares in Inari it will make huge gain but when are they going to sell, 197 years from now??

2017-07-06 11:00

if want insas reflect its value, then must sell all inari stake..then cantekkkkk

2017-07-06 16:44

Actually RNAV is an out-dated stock valuation method.

Most of Msia property counter are trade below their RNAV this was an evidence dat RNAV is not a good selling ponit.

People are looking a good propect /growing counter ,so I will tell people :

(1) INSAS was a proxy "INARI" play due to it's controlling intrrest (20%/ 400 mil shares or Rm 880 mil share valuation) on Inari and Insas will direct benefits from Inari growing story.

(2)Dividend - Insas is a cash rich company(>300 mil cash/share/bond),company ability to upwards their dividend.

2017-07-06 18:01

Actually RNAV is an out-dated stock valuation method.

Most of Msia property counter are trade below their RNAV this was an evidence dat RNAV is not a good selling ponit.

People are looking a good propect /growing counter ,so I will tell people :

(1) INSAS was a proxy "INARI" play due to it's controlling intrrest (20%/ 400 mil shares or Rm 880 mil share valuation) on Inari and Insas will direct benefits from Inari growing story.

(2)Dividend - Insas is a cash rich company(>300 mil cash/share/bond),company ability to upwards their dividend.

First point Valid, second point is totally fraud. Insas hardly pay shareholders dividend. Forget it

2017-07-06 18:08

Haiyo, whenever Klci start to Moo Moo , Insas as the Investment Holding in Malaysia will have relatively trending with the klci ... simple is that need not science at all.

2017-07-16 11:15

hey wltan22, from my understanding, u cannot calculate certain stuff like these. For example, NTA from associate company does not contribute to the assets of INSAS, only the subsidiary does. Besides that, if you assume Insas sold off Inari, you have to deduct the total amount recorded at non-current assets under Associate Companies. So you have to figure out what price did Insas brought Inari at first, then add all net profits contributed to Insas from Inari, deduct it by the dividend given yearly and then you get the pure value of Inari to Insas.

2017-09-23 12:43

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-11-26 16:50:00

TURTLE SYSTEM 20

5 Mins

SELL

2024-11-26 16:40:00

EMA 5

10 Mins

BUY

2024-11-26 16:40:00

EMA 5

5 Mins

BUY

2024-11-26 16:40:00

TURTLE SYSTEM 20

5 Mins

BUY

2024-11-26 16:30:00

EMA 5

30 Mins

BUY

Apps

Top Articles

2

save malaysia!

3

4

5

6

Koon Yew Yin's Blog

7

THE INVESTMENT APPROACH OF CALVIN TAN

8

Good Articles to Share

Le Pen makes new threat to withdraw support for French government

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Alex Foo

don't buy, later u insaf

2017-07-05 12:26