Real Talk

[SELL] Carimin - Exposing KYY's Nonsense

BatuHitam

Publish date: Fri, 22 Feb 2019, 09:56 AM

BatuHitam

0 1

This blog is my take on doing what I deem to be the right thing - exposing overvalued stocks and stocks which are being manipulated to look better than they actually are.

My main goal is to prevent investors from bleeding more than they need to. I do not have short positions and do not benefit from the tumbling house of cards.

My main goal is to prevent investors from bleeding more than they need to. I do not have short positions and do not benefit from the tumbling house of cards.

KYY’s credit as an investor is rapidly diminishing. The most recent target of his is none other than Carimin Petroleum. With its share price up 300% in 2.5 months, alarm bells should be ringing in the head of any competent investor. This report will aim to discredit KYY’s recommendation as stupidity at best and straight-up misleading at worst.

From his post ‘Carimin - As I See It’, one finds the following quote:

Just based on its strong earning, the company must be very efficient and most likely the company can secure more contracts from Petronas. As a result, the company will have a very good profit growth prospect which is the most powerful catalyst to move share price.

This is utter bullshit. This article will attempt to show that:

- Earnings are not strong

- Company is the exact opposite of efficient

- No more upside from Petronas, who is their largest client

- Thus, little to no profit growth prospects

- Our valuation at the end will show that this company is highly overvalued, and we recommend those who own this stock to SELL

KYY’s Valuation: Even an IB intern can smell the bullshit

In the post ‘Waiting for Correction Strategy’, KYY pegged FY EPS of RM0.2 and P/E of 10x to arrive at a price per share of RM2. The investment thesis and rationale behind this is apparently:

‘I believe the big buyers who were not afraid to buy so aggressively, must have inside information that the Q2 EPS is 5 or more sen.’

No investor of a sound mind will recommend and investment because of an upwards movement of share price – what is even more insane is the attributing of the movement not to speculation but to apparent insider information.

Many people are involved in the calculation of the profit or EPS, such as the company directors, accountants, book keepers, clerks etc. As a result, many people already knew the 2Q EPS and likely they would have leaked out the information to their friends and relatives.

The above is an unedited quote by KYY. Even Warren Buffet and Charlie Munger, at the ripe old age of 88 and 95 respectively, are not senile enough to make investment decisions based on what is a baseless and frankly ridiculously rationale.

The nail in the coffin for me is the pro-rating of EPS for the next 3 Quarters based on 1Q19 and then pegging a PE of 10x. This is absolutely outrageous stuff for a company that has barely even been profitable and is exposed to a highly volatile and risky O&G sector, while paying no dividend. In contrast, Apple currently trades at 14x P/E even with its high margins, strong branding, resilient businesses and dividends.

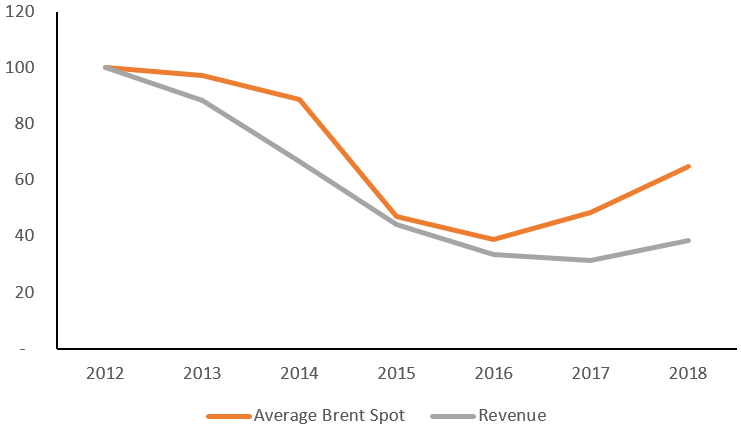

Lastly, the chart below with Carimin’s revenue and Brent spot price indexed to 2012 shows that Carimin’s revenue dipped much more than the brent crude and hasn’t exhibited as strong of a recovery. Carimin is solely exposed to the Malaysian O&G industry and any notion that there will be a massive recovery in both the industry and Carimin’s business is unfounded. More evidence of this will be presented later.

What does Carimin actually do?

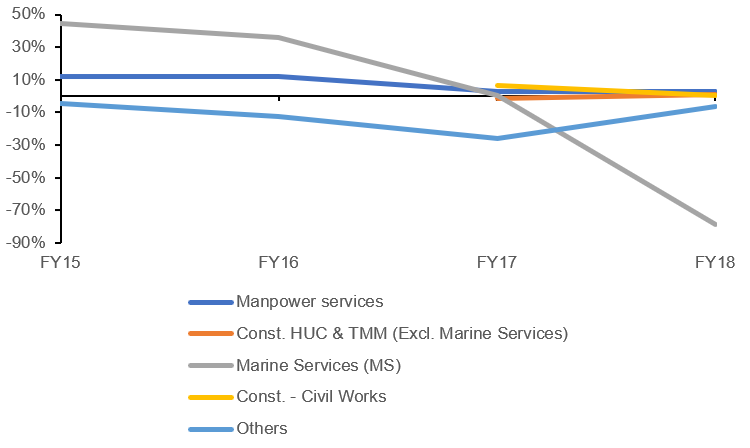

KYY called Carimin a renowned company, what renowned company has a market cap of US$45M? The actual business model for Carimin leaves a lot to be desired. Even after recent acquisitions in an attempt to diversify its business, we see that only the manpower services and const. HUC & TMM segments are profitable. In fact, Carimin is badly struggling to find any consistency in terms of profitability. While we commend that it has at least pare down its debt, we remain sceptical as to whether it has the management has the actual expertise to turn around many of the company’s floundering businesses. The track record of said management has been nothing to be proud of so far.

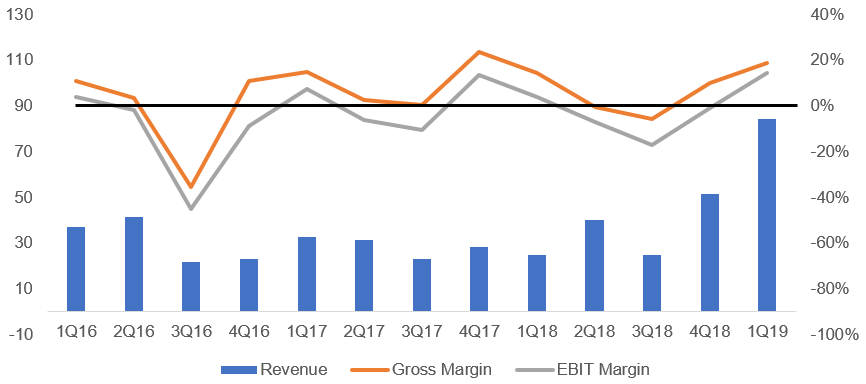

Highly volatile margins for what seems to be a simple business

Moreover, the type of businesses Carimin is engaged in low in value, as indicated by its margin. Furthermore, their overall margins have proven to be incredibly volatile and EBIT margins have usually been -ve between the second to fourth quarters, based on historical data.

No Further Upside

It is no secret that 100% of Carimin revenues are dependent on Malaysia’s O&G sector. In particular, Petronas provides the majority of their business. Contrary to what KYY and the management would like you to believe much of that revenue potential has already been recognised.

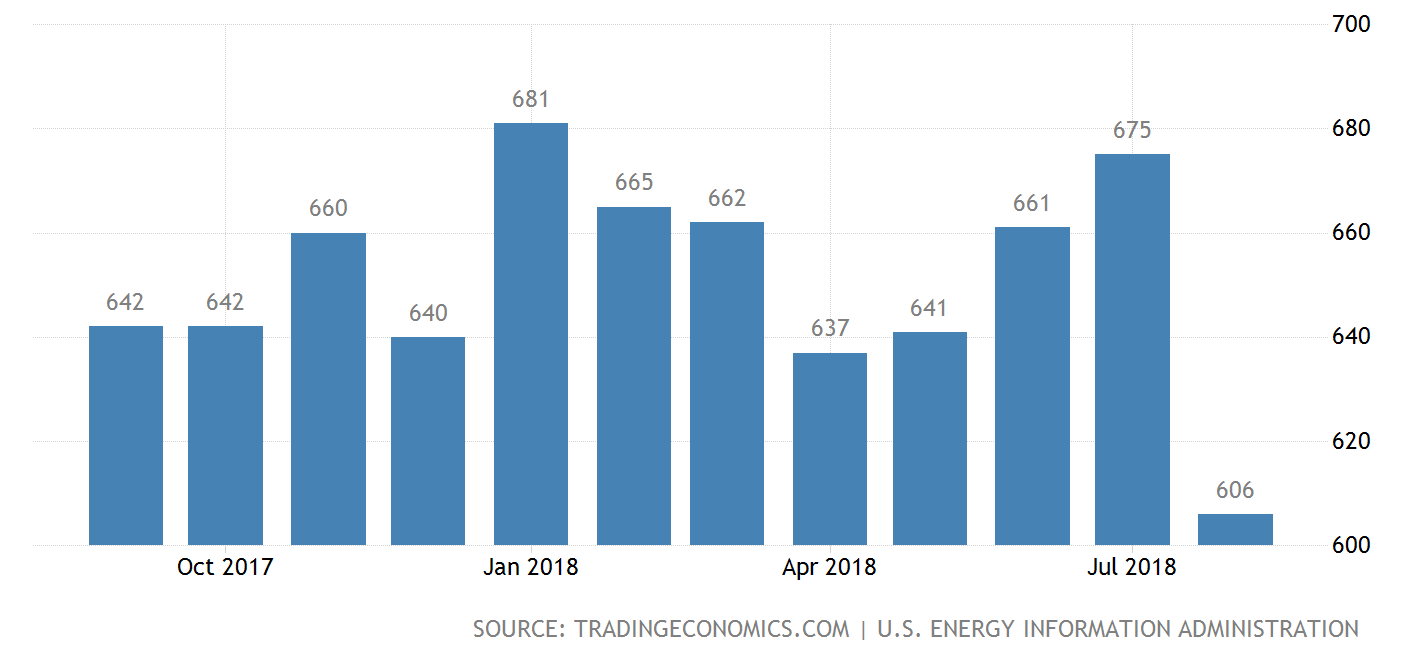

Firstly, Crude oil production in Malaysia has been relatively stable in the past few years. However, the total production levels are down from the highs of 704kbpd in 2006. Going forward, we do not expect much changes in output level, as pressures from shale producers and opec will lead to compressed output levels in an effort to profit from the inelasticity of O&G demand. With renewables expected to take flight in the next 3-5 years, our long term outlook for O&G prices is rather bearish. If oil prices remain in the current range, OPEC will continue to put a lid on output.

The current proven crude reserves in Malaysia is 3,600 million barrels. Assuming an output of 650kbpd, we have approximately 15 years of crude remaining.

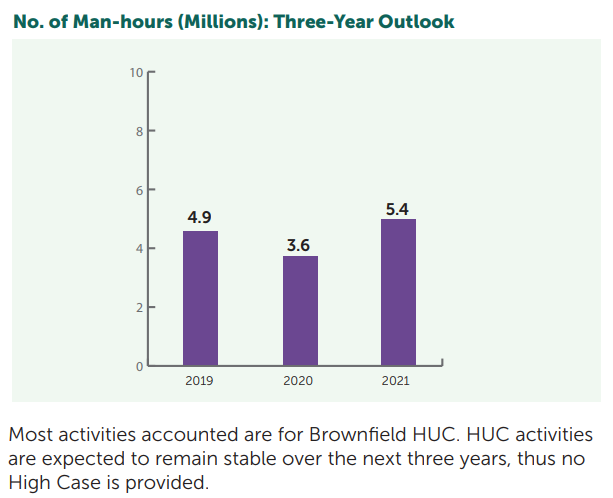

Secondly, Petronas expects man-hours to range between 3.6 – 5.4 million hours. This does not bode-well for the thesis that Carimin will benefit in the surge in O&G projects that at this point, doesn’t seem to be materialising.

Thirdly, Petronas’ forecast for HUC and MCM indicates that all contracts for the next 3 years have been fully given out. This implies zero new revenue contribution from Petronas in this segment for Carimin over the next few years. Moreover, the outlook for post 2021 is neutral, and thus we expect no medium or long-term upside for Carimin.

Our Valuation: Base Share Price of RM0.84

To summarise our key theses:

- Top-line expansion will be highly unlikely, our bull case assumes that orderbook replenishment maintains the revenue run rate implied by 1Q19 (which is very bullish)

- Margin volatility implies some form of contraction going into the next 3 quarters. Q4 and Q1 historically constitute the periods with highest margins

- Long term outlook is bearish due to the onset of renewable energy and an estimated 15 years of remaining proven reserve – thus we are projecting a 20Y DCF with no terminal value

Historical Numbers:

Tabulated Assumptions:

DCF Valuation: Ran for over 20 years to err on the conservative side

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

Discussions

10 people like this. Showing 30 of 30 comments

No need bising. You still can run at 0.800. There are buyers at this price.

2019-02-22 10:03

@kaltech Ah my intelligence platform hasn't update the numbers for 2Q19. I've looked at the numbers and made the debt adjustments. The latest quarterly result basically fulfils my thesis once you pay attention to the margin erosion.

2019-02-22 10:13

@abang_misai I don't own any of this stock bro. I wrote this out of moral conscience. I have provided a short thesis for this stock and have happily laid out all my assumptions for you to disagree with (and not just pull a P/E of 10x out of my ass)

2019-02-22 10:16

I would buy a stock when its price crosses MA 20 days. Simple as that.

We need only a simple reason to goreng. Simple as that. No need bother what's going on with the company.

Stays long enough in i3. You should know that when Koon + Bee, it never fails.

Stays long enough in i3, You should know that KYY plays stock appears in OTB's stock pick challenge, it fliesssss. Remember vs latitud and now carimin.

.40 to .70 you don't want?

Just wait for next one. Long live KYY

2019-02-22 16:47

I do find your complexity more nonsense than KYY simplicity..........

I find KYY simplicity is the Q that makes him worth hundreds of millions.....

2019-02-22 17:08

not nice insulting sifu kyy...

if u feel manipulated, then don't buy...

simple

jgn tutup periuk nasi orang

2019-02-22 19:02

Why make things so difficult for yourself.

If you don't trust funny buy.

After buy and blame 80 year old man the only shameful one is yourself.

2019-02-22 19:05

did he point a gun and force u buy...

always bash good ppl when lose money...

if u cannot afford to lose, stock market is not for u

simple

2019-02-22 19:09

Actually i feel sayang when uncle said he exited HIBI ,

Dayang is excellent o&g support firm, just cant go far with its debt restructuring unsolved.

2019-02-22 19:12

Give you a like, hard to find any negative articles in i3. We need more short opinions.

2019-02-22 19:59

Dear all,

If according to Koon's golden rule that Hibiscus failed his rule thus he sold all and buy Carimin then he himself had failed his own rule because Carimin do not have two quater of increase profit. Luckily this quarter Carimin still show some profit otherwise no eye see. So if you still believe in Koon's golden rule then sell Carimin and buy Dayang.

Thank you

2019-02-22 20:57

Lol... Sslee, how about this, you justify how come hibiscus this q result lower than last.... Hehe

2019-02-22 21:00

Better go for construction counters. Easier to gauge their financial strength

2019-02-22 21:02

my plane bro, No doubt Gamuda is the big brother, but i prefer those 2nd liners. Must be able to give dividends and no posting losses for the last 8 quarters.

2019-02-22 22:29

Wa this guys got balls ! Nice ! . Luckily i have been buying construction since they hit rock bottom ! Oil is just too volatile to play with !

2019-02-22 23:28

If KYY is always right, follow him unthinkably.

Of course, he is not always right.

Also, his valuation is flawed.

Annualising the latest qtr and multiply by a PE of 10 is just so misleading.

But it is so important to give a target price, he has to do it.

How to be a safe investor?

His golden rule is similarly flawed. I am surprised few pointed this out to him.

2019-02-23 08:30

kyy is just like any coffee shop speculators,relying on good luck or bad luck.if you meant he did ,good and sound research,u must be joking.

2019-02-23 22:53

this article relates Brent to revenue which is stupid and manpower which contributes 10-15% earnings to Carimin only, haha, and never discuss liquidity and other factors as well, comparing apple to Carimin some more, amateur investor

2019-02-24 09:14

always remember the golden rule to play uncle counter... buy before uncle buy and sell before uncle sell

2019-02-26 16:06

exactly like what uncle typical pattern, one day very hard then lembik already after that what happen, diarhea

2019-02-26 16:08

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

Dragon Leong blog

2

Stock Market Enthusiast

Feng Shui Market Outlook for FBM KLCI in the Year of the Wood Snake (2025)

3

The Alpha Trader

5

Stock Market Enthusiast

3 Resilient Stocks That Defied Malaysia’s Market Slump in January 2025 - #GCB, #ABMB, #CDB

6

MQ Market Updates

8

My Trading Adventure 2025

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

kalteh

This would be more credible if it was published before 2nd QTR result was out yesterday.

2019-02-22 10:01