Bullbearbursa.com

Bina Puri Holdings Berhad (BPURI) – Optimism in stance amidst challenging times

Bullbearbursa

Publish date: Mon, 31 Dec 2018, 09:35 AM

Bullbearbursa

0 22

All materials published here are prepared by BullBearBursa.com.

For more information and latest news, plaese refer to http://www.bullbearbursa.com/ or our official facebook page https://www.facebook.com/bullbearbursa/

For more information and latest news, plaese refer to http://www.bullbearbursa.com/ or our official facebook page https://www.facebook.com/bullbearbursa/

Bina Puri Holdings Berhad (BPURI) – Optimism in stance amidst challenging times

Here is why we think BPURI is truly a GOOD BUY for you! You do not want to miss this ride as the upside catalyst of this counter (TP: RM0.98) shall bring you an adventurous trip.

1) Who is Bina Puri Holdings Berhad (BPURI) (5932)?

BPURI mainly operates as a contractor of earthworks, and also in building and road construction in Malaysia. Its construction portfolio comprises infrastructural works, such as roads and highways, bridges and interchanges, airport works, etc.

The company's other projects include construction of low, medium, and high-rise residential, commercial, and educational buildings. It also engages in property development; manufactures polyol; produces ready mix concrete; and engages in quarry operations.

In addition, BPURI Holdings operates as a commission agent; and manufactures bricks and plaster cement.

2) What is the current industry prospect for BPURI?

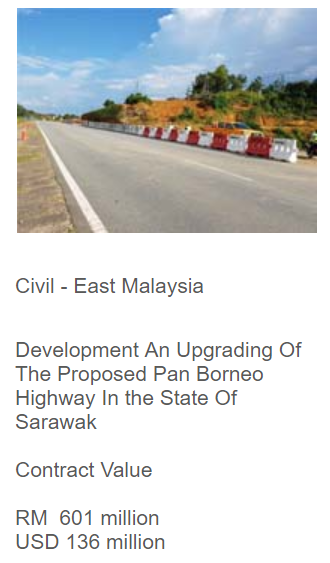

Although the order book replenishment prospects of construction player had been pacing down recently, the group still hold its stance in coming back stronger for the year ahead despite intensive & tough environment. Since the rise of new government, the job flows of construction sector had decelerate significantly due to review of mega projects. But on a positive note, pick up may be seen in 2H19 as there will be resumption of a few selective infrastructure projects (which likely include Pan Borneo Highway – Sabah & Sarawak) Why Pan Borneo Highway? This is because BPURI currently has an ongoing order book of upgrade development in Pan Borneo Sarawak which value @ RM600 million (which is the largest order book for BPURI portfolio).

Pan Borneo Sarawak (PBS)

Phase 1 of PBS has been trimmed by 4% from RM16.5b to RM15.8b. Currently, the progress of 11 work packages is approx. @ 35%. Assume the 4% has been factored into the BPURI order book, the contract value will similarly haircut by 4% which is RM24 mil impacted to the contract value of RM600 million.

The upward catalyst has yet to be seen on BPURI as the work progress was only at an initial stage. Works Minister Baru Bian was quoted in media reports as mentioned He will personally monitor the project to ensure its timely completion by 2021.

Although the revised capex for PBS was calculated on a lower cost due to cost-cutting & optimization measures, PBURI will certainly gain back its position starting 2019 when the progress starts to ramp up in a faster pace.

Stable income flow are expected from 2019 onwards as the Pan Borneo Highway progress will start ramping up soon.

3) How was BPURI doing in terms of financially?

BPURI has improved significantly on their profitability due to surge of sales in property segment.

For YoY profitability, BPURI has registered a PAT of RM13.3 million compared to RM6.8 million in corresponding period of previous financial year. It shows an improvement margin of 97% as their earning catalyst were mainly came from construction (Pan Borneo Highway – Sarawak) & property segment in the East & West Malaysia.

With Pan Borneo Highway Sarawak rolling soon, a stable stream of earnings is expected for BPURI. Despite weak prospect on construction sector, BPURI still able to improve their debt management from a gearing of 1.86 to 1.61.

Overall, BPURI has been sustaining their balance sheet strength in a healthy manner given the weak prospect and intensive competition.

|

|

9M2018 |

9M2017 |

9M2018 vs 9M2017 |

|

RM’000 |

RM’000 |

(%) |

|

|

|

|

|

|

|

Revenue |

526,851 |

781,204 |

-32.56% |

|

GP |

76,569 |

67,163 |

14.00% |

|

PBT |

20,044 |

11,018 |

81.92% |

|

PAT |

13,299 |

6,751 |

96.99% |

|

EBITDA |

56,099 |

47,078 |

19.16% |

|

Basic/Diluted EPS (sen) |

|||

|

GP margin |

14.53% |

8.60% |

5.93% |

|

PBT margin |

3.80% |

1.41% |

2.39% |

|

PAT margin |

2.52% |

0.86% |

1.66% |

|

EBITDA margin |

10.65% |

6.03% |

4.62% |

|

Key Financial Ratios |

|||

|

Current Ratio (times) |

1.15 |

1.12 |

2.68% |

|

Gearing Ratio (times) |

1.61 |

1.86 |

13.44% |

|

ROE(%) |

9.27% |

4.94% |

4.33% |

|

ROA(%) |

0.84% |

0.40% |

0.44% |

|

|

|

4) How should BPURI be valuated given the impression of weak prospect?

Given that BPURI is a conglomerate with multiple business segments, it is not hard to see that sum of part (SOP) valuation being an appropriate way to value the company.

In terms of valuation basis, loss making business segments-construction and quarry and ready-mix concrete segments are valued using PB multiple as net profits are not available while property investment and development and power supply segments are valued using PE multiple. On the other hand, polyol segment is being valued using its net book value as the segment contribution remains negligible.

Book value or net profit of each business segments for the latest financial year are being use together with fair PB/PE multiple to derive the fair value of each business segments. To be conservative, we have come out with the fair PE/PB multiples for each business segments with reference to the lowest multiple among its respective industry peers (refer to Table XXX).

Even with such conservative approach, we are still able to derive an intrinsic value of the company at MYR0.978 per share, far fetch from the current price of MYR0.20 per share! While the poor financial performance coupled with its rather weak balance sheet are something warrants concern, we see such pessimism being unjustified due to its severe undervaluation. Although turnaround in operations remains to be seen, it is likely that any forms of positive news will drive a valuation re-rating for the company, given such pessimistic sentiments on the company.

Table XX: Sum of Part Valuation

|

Business Segment |

Valuation Basis |

Book Value/Net Profit for the Latest Financial Year (RM'000) |

Fair PB/PE Multiple (Times) |

Fair Value (RM'000) |

|

Construction |

PB multiple |

200,518 |

0.4 |

75,395 |

|

Property Investment and Development |

PE multiple |

29,804 |

4.8 |

142,165 |

|

Quarry and Readymix Concrete |

PB multiple |

4,471 |

0.71 |

3,174 |

|

Power Supply |

PE multiple |

3,090 |

11.1 |

34,299 |

|

Polyol |

Net Book Value |

568 |

NA |

568 |

|

Grand Total |

|

|

|

255,601 |

|

|

|

|

||

|

Existing Shares (000) |

|

261,348 |

||

|

|

|

|

||

|

Intrinsic Value (MYR/share) |

|

0.978 |

||

|

|

|

|

Table XXX: Valuation Multiples for the Respective Industries

|

Construction Sector |

PB Multiple |

|

Ahmad Zaki Resources |

0.41 |

|

George Kent |

1.34 |

|

Malaysian Resources Corp |

0.70 |

|

Sunway Construction |

3.77 |

|

WCT |

0.38 |

|

Industry Average |

1.32 |

|

|

|

|

Property Investment and Development Sector |

Rolling PE Multiple |

|

Crescendo |

13.57 |

|

Hua Yang |

26.64 |

|

Sunsuria |

5.98 |

|

Malton |

4.77 |

|

MKH |

10.47 |

|

MK Land |

9.11 |

|

Paramon |

5.36 |

|

Plenitu |

10.63 |

|

Tambun |

5.57 |

|

Industry Average |

10.23 |

|

|

|

|

Quarry and Readymix Concrete Sector |

PB Multiple |

|

Hume Industries |

1.00 |

|

Lafarge |

0.71 |

|

Industry Average |

0.855 |

|

|

|

|

Power Supply Sector |

Rolling PE Multiple |

|

Cypark |

11.09 |

|

Malakoff |

20.51 |

|

Ranhill |

11.26 |

|

Tenaga |

13.77 |

|

YTL Power |

13.08 |

|

Industry Average |

13.94 |

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Bullbearbursa.com

What’s next for Techbond (5289) after its listing debut year (TP: RM0.90)

Created by Bullbearbursa | Oct 28, 2019

6 things you should know about MTAG – Potential 45% upside you wouldn’t want to miss!

Created by Bullbearbursa | Sep 23, 2019

Techbond TP RM 1.28 - 33% Upside You Never Want to Miss [RHB Research]

Created by Bullbearbursa | Feb 13, 2019

5 Things You Need To Know About TechBond IPO – 43.18% Upside You Never Want to Miss

Created by Bullbearbursa | Dec 03, 2018

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-16 15:40:00

ADX

5 Mins

SELL

2024-07-16 15:40:00

EMA 5

10 Mins

SELL

2024-07-16 15:20:00

EMA 5

5 Mins

SELL

2024-07-16 14:35:00

TURTLE SYSTEM 20

5 Mins

SELL

2024-07-16 14:35:00

TURTLE SYSTEM 55

5 Mins

SELL

Apps

Top Articles

1

Bursa Stock Musings - Thoughts & Ideas

PGF Capital - insti shareholding up from 5% to 14%! (part 1)

2

南洋行家论股

4

How to become a resilient trader

5

RHB Investment Research Reports

6

The Daily Pulse of Bursa Malaysia

7

8

Koon Yew Yin's Blog

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

lksiam

TP 0.98?? Haha... TP nowadays is for shouting.

2018-12-31 09:53