The perils of holding all else constant in perpetual growth equations and playing with individual inputs, not only leads to the use of impossibly high growth rates but also inflates the importance of growth in the terminal value estimation. Growth is not free and it has to be paid for with reinvestment and in the terminal value equation, this effectively means that you cannot leave cash flows fixed and change the growth rate. As the growth rate increases, even within reasonable bounds, the company will have to reinvest more to deliver that growth, leading to lower cash flows, thus making the effect on value unpredictable.

Paying for Growth

To make this relationship explicit, let us start by defining the two fundamental drivers of growth, a measure of how much the company reinvests (reinvestment rate) and how well it reinvests (Return on invested capital)

Thus, as g changes, both the numerator and denominator change. For a firm that expects to generate $100 million in after-tax operating income next year, with a cost of capital of 10%, the terminal value can be estimated as a function of the ROIC it earns on its marginal investments in perpetuity. With a growth rate of 3% and a return on capital is 12%, for instance, the terminal value is:

Thus, as g changes, both the numerator and denominator change. For a firm that expects to generate $100 million in after-tax operating income next year, with a cost of capital of 10%, the terminal value can be estimated as a function of the ROIC it earns on its marginal investments in perpetuity. With a growth rate of 3% and a return on capital is 12%, for instance, the terminal value is:

Changing the growth rate will have two effects: it will change the cash flow (by altering reinvestment) and change the denominator, and it is the net effect that determines whether and how much value will change.

Changing the growth rate will have two effects: it will change the cash flow (by altering reinvestment) and change the denominator, and it is the net effect that determines whether and how much value will change.

The Excess Return Effect

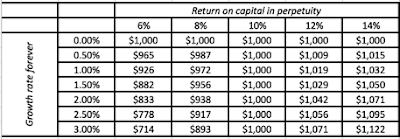

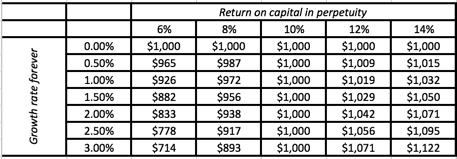

Tying growth to reinvestment leads us to a simple conclusion. It is not the growth rate per se, but the excess returns (the difference between return on invested capital and the cost of capital) that drives value. In the table below, I take much of the hypothetical example from above (a company with expected operating income of $100 million next year and a cost of capital of 10%) and examine the effects of changing growth rate on value, for a range of returns on capital.

Paying for Growth

To make this relationship explicit, let us start by defining the two fundamental drivers of growth, a measure of how much the company reinvests (reinvestment rate) and how well it reinvests (Return on invested capital)

In stable growth, the expected growth rate has to be a product of these two numbers

Growth rate = Reinvestment Rate (RR) * Return on Invested Capital (ROIC)

Over finite time periods, the growth rate for a company can be higher or lower than this "sustainable" growth rate, as profit margins and operating efficiency change, but once you get to the terminal value, where you are looking at forever, there is no evading its reach. Isolating the reinvestment rate in the equation and plugging back into the terminal value equation, here is what we get:

Thus, as g changes, both the numerator and denominator change. For a firm that expects to generate $100 million in after-tax operating income next year, with a cost of capital of 10%, the terminal value can be estimated as a function of the ROIC it earns on its marginal investments in perpetuity. With a growth rate of 3% and a return on capital is 12%, for instance, the terminal value is:

Thus, as g changes, both the numerator and denominator change. For a firm that expects to generate $100 million in after-tax operating income next year, with a cost of capital of 10%, the terminal value can be estimated as a function of the ROIC it earns on its marginal investments in perpetuity. With a growth rate of 3% and a return on capital is 12%, for instance, the terminal value is:The Excess Return Effect

Tying growth to reinvestment leads us to a simple conclusion. It is not the growth rate per se, but the excess returns (the difference between return on invested capital and the cost of capital) that drives value. In the table below, I take much of the hypothetical example from above (a company with expected operating income of $100 million next year and a cost of capital of 10%) and examine the effects of changing growth rate on value, for a range of returns on capital.

Note that as you increase the growth rate in perpetuity from 0% to 3%, the effect on the terminal value is unpredictable, decreasing when the return on invested capital < cost of capital, unchanged when the ROIC = Cost of capital and increasing when the ROIC> Cost of capital. In fact, you an just as easily construct an equity version of the terminal value and show that the growth rate in equity earnings can affect equity value only if the ROE that you assume in perpetuity is different from your cost of equity.

There are a few valuation purists who argue that the only assumption that is consistent with a mature, stable growth company is that it earns zero excess returns, since no company can have competitive advantages that last forever. If you make that assumption, you might as well dispense with estimating a stable growth rate and estimate a terminal value with a zero growth rate. While I see a basis for the argument, it runs into a reality check, i.e., that excess returns seem to last far longer than high growth rates do. Thus, your high growth period has to be extended to cover the entire excess return period, which may be twenty, thirty or forty years long, defeating the point of computing terminal value. It is for this reason that I adopt the practice of assuming that excess returns will move towards zero in stable growth and giving myself discretion on how much, with zero excess return being my choice for firms with few or no sustainable competitive advantages, a positive excess return for firms with strong and sustainable competitive advantages and even negative excess return for badly managed firms with entrenched management.

Two Dangerous Practices

If you follow the practice of tying growth to reinvestment, you will be well-armed against some of the more dangerous practices in terminal value estimation.

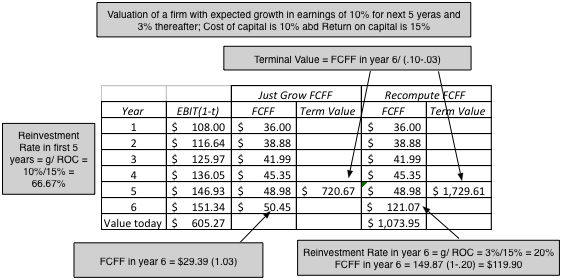

1. Grow the nth year's cash flow: If you consider the perpetual growth equation in its simplest form, it looks as follows:

The sheer simplicity of the equation can lull you into a false sense of complacency. After all, if you have projected the free cash flows for the your high growth period of 5 years, i.e, the cash flows after taxes and reinvestment, and you want to estimate your terminal value at the end of year 5, it seems to follow that you can grow your free cash flow in year 5 one more year at the stable growth rate to get your numerator for the terminal value calculation. The danger with doing is that you have effectively locked in whatever your reinvestment rate was in year 5 now into perpetuity and to the extent that this reinvestment rate is no longer compatible with your stable growth rate, you will misvalue your firm. For example, assume that you have a firm with $100 million in after-tax operating earnings that you expect to grow 10% a year for the next five years, with a reinvestment rate of 66.67%% and a return on investment of 15% backing up the growth; after year 5, assume that the expected growth rate will drop to 3%, with a cost of capital of 10%. In the table below, I illustrate the effect on value today of using the "just grow the year 5 free cash flow" and contrast it with the value that you would obtain if you recomputed your terminal year's cash flow, with a reinvestment rate of 80%, compatible with your stable growth rate and return on capital

The sheer simplicity of the equation can lull you into a false sense of complacency. After all, if you have projected the free cash flows for the your high growth period of 5 years, i.e, the cash flows after taxes and reinvestment, and you want to estimate your terminal value at the end of year 5, it seems to follow that you can grow your free cash flow in year 5 one more year at the stable growth rate to get your numerator for the terminal value calculation. The danger with doing is that you have effectively locked in whatever your reinvestment rate was in year 5 now into perpetuity and to the extent that this reinvestment rate is no longer compatible with your stable growth rate, you will misvalue your firm. For example, assume that you have a firm with $100 million in after-tax operating earnings that you expect to grow 10% a year for the next five years, with a reinvestment rate of 66.67%% and a return on investment of 15% backing up the growth; after year 5, assume that the expected growth rate will drop to 3%, with a cost of capital of 10%. In the table below, I illustrate the effect on value today of using the "just grow the year 5 free cash flow" and contrast it with the value that you would obtain if you recomputed your terminal year's cash flow, with a reinvestment rate of 80%, compatible with your stable growth rate and return on capital

Conclusion

It is conventional wisdom that it is the growth rate in the perpetual growth equation that is the most significant driver of the resulting value. That may be true if you hold all else constant and change only the growth rate, but it is not, if you recognize that growth is never free and that changing the growth rate has consequences for your cash flows. Specifically, it is not the growth rate per se that determines value but how efficiently you generate that growth, and that efficiency is captured in the excess returns earned by your firm.

YouTube Video

Attachments

There are a few valuation purists who argue that the only assumption that is consistent with a mature, stable growth company is that it earns zero excess returns, since no company can have competitive advantages that last forever. If you make that assumption, you might as well dispense with estimating a stable growth rate and estimate a terminal value with a zero growth rate. While I see a basis for the argument, it runs into a reality check, i.e., that excess returns seem to last far longer than high growth rates do. Thus, your high growth period has to be extended to cover the entire excess return period, which may be twenty, thirty or forty years long, defeating the point of computing terminal value. It is for this reason that I adopt the practice of assuming that excess returns will move towards zero in stable growth and giving myself discretion on how much, with zero excess return being my choice for firms with few or no sustainable competitive advantages, a positive excess return for firms with strong and sustainable competitive advantages and even negative excess return for badly managed firms with entrenched management.

Two Dangerous Practices

If you follow the practice of tying growth to reinvestment, you will be well-armed against some of the more dangerous practices in terminal value estimation.

1. Grow the nth year's cash flow: If you consider the perpetual growth equation in its simplest form, it looks as follows:

Note that just growing out the FCFF yields a value today of only $605 million, about half of the (right) value that you get with a recomputed FCFF.

2. Stable Growth firms don't need to reinvest: I am not sure what the roots of this absurd practice are but they are deep. Analysts seems to be willing to assume that when you get to stable growth, you can set capital expenditures = depreciation, ignore working capital changes and effectively make the reinvestment rate zero, while allowing the firm to continue growing at a stable growth rate. That argument fails at two levels. The first is that if you reinvest nothing, your invested capital stays constant during your stable growth period, and as operating income rises, your return on invested capital will approach infinity. The second is that even if you assume a growth rate = inflation rate, you will have to replace your existing productive assets as they age and the same inflation that aids you on your revenues will cause the capital expenditures to exceed depreciation.

Conclusion

It is conventional wisdom that it is the growth rate in the perpetual growth equation that is the most significant driver of the resulting value. That may be true if you hold all else constant and change only the growth rate, but it is not, if you recognize that growth is never free and that changing the growth rate has consequences for your cash flows. Specifically, it is not the growth rate per se that determines value but how efficiently you generate that growth, and that efficiency is captured in the excess returns earned by your firm.

YouTube Video

Attachments

DCF Myth Posts

Introductory Post: DCF Valuations: Academic Exercise, Sales Pitch or Investor Tool

- If you have a D(discount rate) and a CF (cash flow), you have a DCF.

- A DCF is an exercise in modeling & number crunching.

- You cannot do a DCF when there is too much uncertainty.

- It's all about D in the DCF (Myths 4.1, 4.2, 4.3, 4.4 & 4.5)

- The Terminal Value: Elephant in the Room! (Myths 5.1, 5.2, 5.3, 5.4 & 5.5)

- A DCF requires too many assumptions and can be manipulated to yield any value you want.

- A DCF cannot value brand name or other intangibles.

- A DCF yields a conservative estimate of value.

- If your DCF value changes significantly over time, there is something wrong with your valuation.

- A DCF is an academic exercise.