Gurus

User/Subscriber Economics: An Alternative View of Uber's Value - Aswath Damodaran

Wednesday, June 28, 2017

In the week since I posted my Uber valuation, I have received many suggestions on what I should have done differently in the valuation, with many of you arguing that I was being a over optimistic in my forecasts of total market, market share and margin improvements and some of you positing that I was too pessimistic. I don't claim to have any certitude about these numbers but the spreadsheet that I used to value Uber is an open one, and you are welcome to convert your suggestions into valuation inputs and make the valuation your own. In just the last few days, though, I have been watching an argument unfold among people that I respect. about whether the reason for my low valuation for Uber is that I am using a DCF model, with the critics making the case that valuing a company based upon its expected cash flows is an old economy framework that will not yield a reasonable estimate of value for new economy companies, driven less by infrastructure investments and returns on those investments, and more by user and subscriber economics. I have long argued that DCF models are much more flexible than most people give them credit for, and that they can be modified to reflect other frameworks. So, rather than deflect the criticism, I will try to build a user based model to value Uber and contrast with my conventional valuation.

Aggregated versus Disaggregated Valuation

If you are doing an intrinsic valuation, the principle that the value of a business is the present value of the expected cash flows from that business, with the discount rate adjusted for risk, cannot be contested. That is true for any business, manufacturing or service, small or large, old economy or new economy. Since that is what a discounted cash flow valuation is designed to do, I have to believe that what critics find objectionable in my Uber DCF model is not with the model itself but in how I estimated the cash flows for Uber, and adjusted for risk. I followed the aggregated model for discounted cash flow valuation where I estimated the cash flows to Uber as a company, starting with its revenues and working through the consolidated expenses and total reinvestment each year and discounted these cash flows at a cost of capital that I estimated for the entire company. Along the way, I had to make assumptions about a total market that Uber would go after, the market share that I expect the company to get in that market and the operating margins in steady state.

Disaggregated Valuation

Value is additive and you can value any company on a disaggregated basis, breaking it down into different divisions/businesses, geographical areas or by units:

- Business Units: In a sum of the parts valuation (SOTP), you can break a multi-business company into its individual business units and value each unit separately. I have a paper where I describe the process of doing a SOTP valuation, using United Technologies, a conglomerate, as my example. If that SOTP valuation is much higher than the value that the market attaches to the company, you may very well find an activist investor targeting the company for a break up.

- Geographical Groupings: When valuing a multinational, you can break the company's operations down geographically and value each geographical grouping (Asia, Latin America, North America, Europe) separately, not only using different assumptions about growth and risk in region but even different currencies for each region.

- Unit-based Valuation: More generally, when valuing any company, you can try to value it on a unit-basis, building up to its value by valuing each unit separately and then aggregating across units. Thus, a pharmaceutical company can be valued by taking each of the drugs that are in its portfolio, including those in the pipeline, and valuing that drug based upon its cash flows and risk and then adding up the values across the entire portfolio. A retail business can be valued by valuing individual stores and adding up the store values and a subscription-based company can be valuing by valuing a subscription and multiplying by the number of subscriptions, current and forecasted.

I may be misreading the critics of my Uber valuation but it seems to me that some of them, at least are making the argument it is better to value Uber, by valuing an individual Uber user first, and then scaling the value up to reflect not just the number of users that Uber has today (existing users) but also new users it expects to add in the future.

Aggregated versus Disaggregated Valuations: Weighing the Trade offs

Valuation on a disaggregated basis allows you to be much more flexible in your assumptions, allowing them to vary across each grouping but there are four reasons why you seldom see them practiced (or at least practiced well) in company valuation.

- Law of large numbers: As companies get larger and more diverse, there is an argument to be made that you are better off estimating on an aggregated basis rather than a disaggregated one. The reason is statistical. To the extent that your estimation errors on a unit basis are uncorrelated or lightly correlated, your estimates on an aggregated level will be more precise than the unit-based estimates. For example, you will have a much better chance of estimating the aggregate revenues for Pfizer correctly than you do of estimating the revenues of each of its dozens of drugs.

- Information Vacuums: Information on a disaggregated basis is difficult to get for individual businesses, geographies, products or users, if you are an investor looking at a company from the outside. If you are doing your valuation from inside the company (as an owner or venture capitalist), you may be able to get this information, but as you will see with my Uber user valuation, even insiders will face limits.

- Missing Value Pieces: When valuing a company on a disaggregated business, it is easy to overlook some items that are consequential for value. In sum of the parts valuation, for instance, analysts are so caught up in estimating the values of individual businesses that they sometimes forget to value "corporate costs", which can be a multi-billion drag on value.

- Corporate Structure: There are some items that are easier to deal with at the aggregate level, because that is where they affect the business. Thus, you can model when taxes come due and the effect of losses easier when you are valuing an aggregated business than when you are valuing it on a disaggregated level. Similarly, if you are concerned about legal penalties or corporate governance, these are better addressed at the aggregated level.

It is true that aggregation comes with costs, starting with the blurring of differences across disaggregated units (business, geographies, products, users) as well as the missing of competitive advantages that apply only to some units of the business and not to others. It is also true that using an aggregated valuation can result in a process that is disconnected from how the owners and managers at user-based companies think about their companies and thus cannot help them in managing these companies or valuing them better.

User Based Valuation

Now that we have laid out the pluses and minuses of aggregated versus disaggregated valuation, let us think about how you would construct a disaggregated valuation of a company that derives its value from users or subscribers. In general, the value of such a company can be written as the sum of three components:

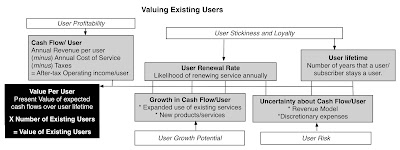

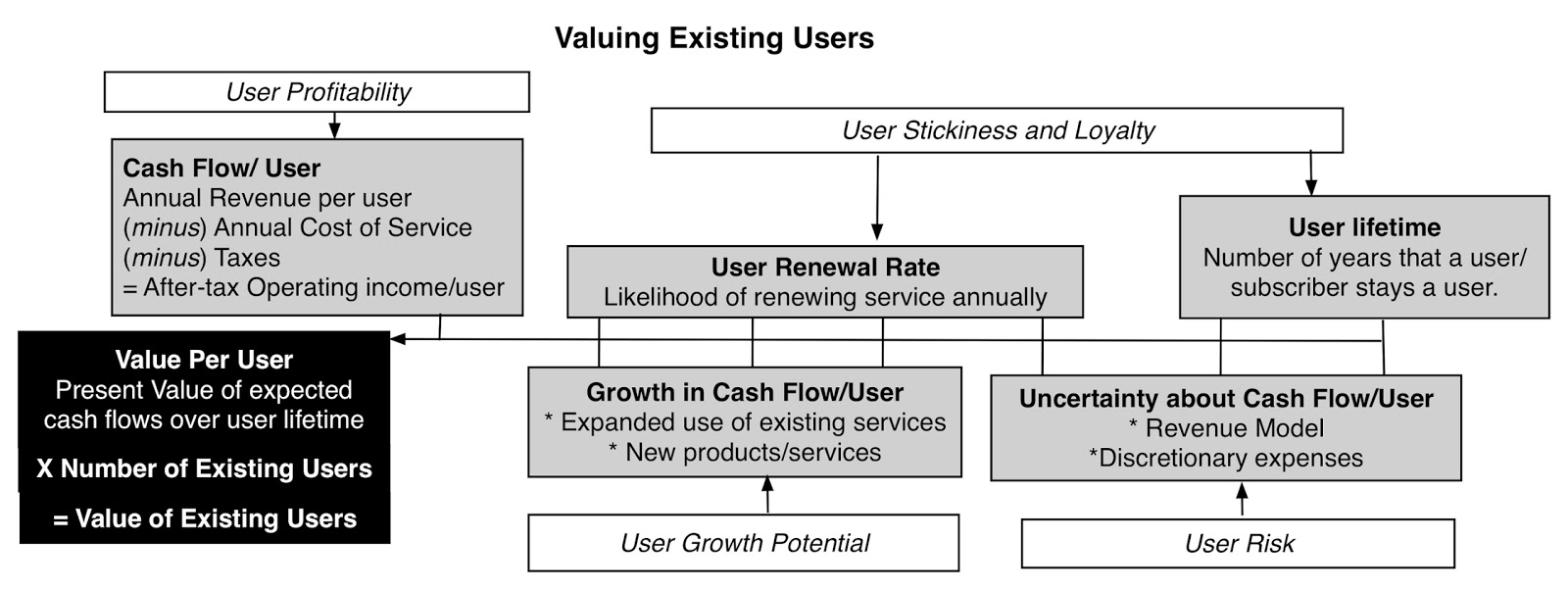

1. Valuing Existing Users

The key step in a user-based valuation is estimating the value of a user and that value is a function of many variables: the cash flows that you are currently generating from a typical user, the length of time you expect that user to use your product or service, your expectations of how much growth you can expect in cash flows from a user over time and the uncertainty that you feel about all of these judgments:

Consider the implications that emerge from this simple framework:

Corporate Expenses and ValueNow that we have laid out the pluses and minuses of aggregated versus disaggregated valuation, let us think about how you would construct a disaggregated valuation of a company that derives its value from users or subscribers. In general, the value of such a company can be written as the sum of three components:

Value of user-based company = Value of existing users + Value added by new users - Value drag from corporate expenses

1. Valuing Existing Users

The key step in a user-based valuation is estimating the value of a user and that value is a function of many variables: the cash flows that you are currently generating from a typical user, the length of time you expect that user to use your product or service, your expectations of how much growth you can expect in cash flows from a user over time and the uncertainty that you feel about all of these judgments:

Consider the implications that emerge from this simple framework:

- The value of a user increases with user stickiness and loyalty (captured in the expected lifetime of a user and the annual renewal rate).

- The value of a user is directly proportional to the profitability of that user (captured as the difference between the revenues from that user and the cost of servicing that user).

- The value of a user is directly proportional to the growth that you can generate in profits over time, by either getting the user to use more of your product or service or coming up with other products or services that you can sell that user.

- The value of a user decreases as you become more uncertain about future cash flows from that user, with that uncertainty being a function of the revenue model that you use and the discretionary nature of the product or service. A subscription-based model, where users agree to pay a fixed amount every period, will generally be less risky and more valuable than a transaction-based model or an advertising-based model, that delivers the same cash flows. A product or service that delivers a necessity (transportation) is less risky than one that meets a more discretionary need (travel).

If you can value a user, you can then estimate the value of an existing user base, by multiplying the value/user by the number of existing users. If you have multiple types of users, with perhaps different revenue models for each, as is the case with LinkedIn's premium and regular members, you can value each user group separately.

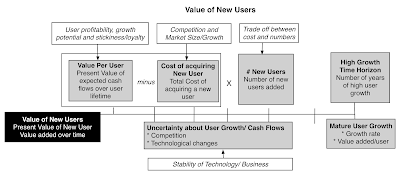

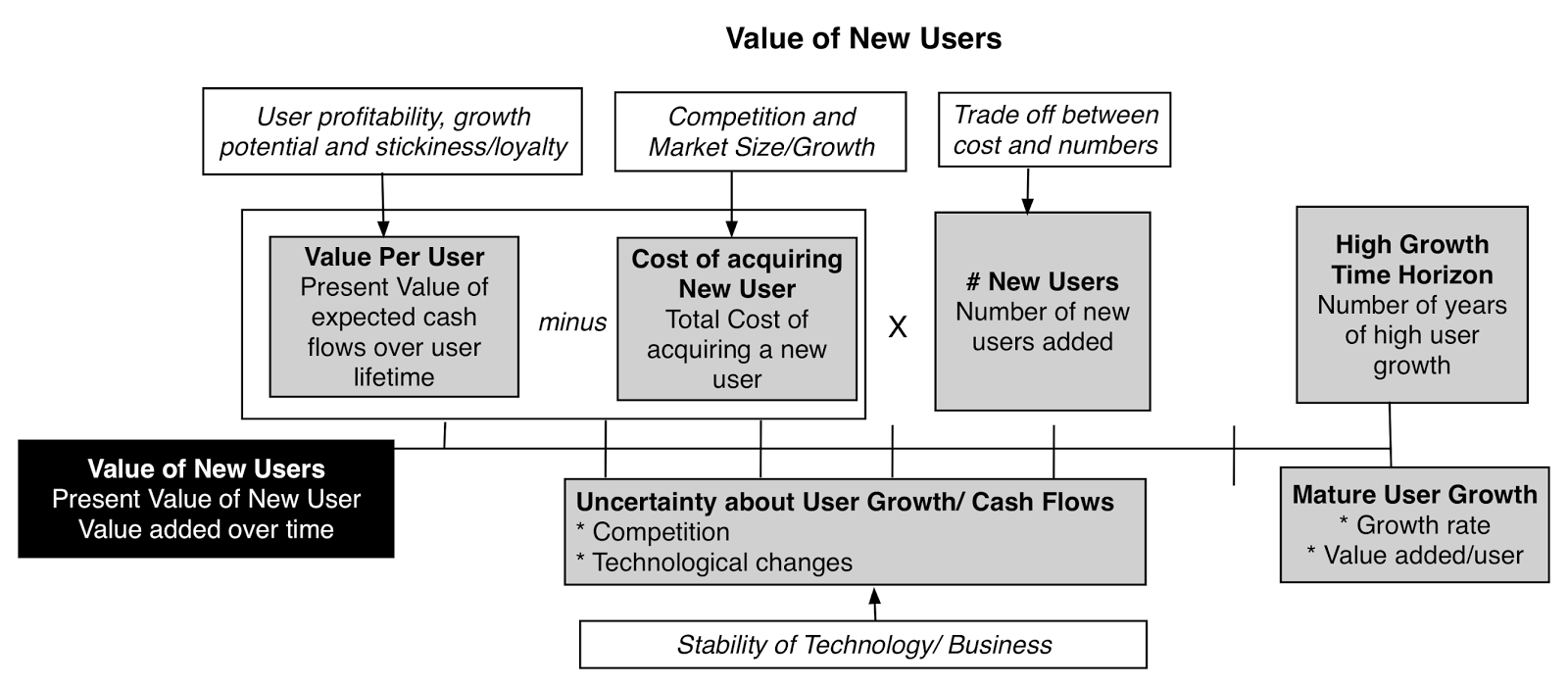

Value Added by New Users

The second segment of value is the value added by new users that you expect to see added in the future. To estimate this value, you can start with the value per user from the last section but you have to net out the cost of acquiring a new user, which can take the form of advertising, introductory discounts and/or infrastructure investments to enter new markets. That net value added by a new user (value per user minus cost of acquiring a user) then has to be multiplied by the number of new users that you expect to add each period and brought back to the present, adjusting for both the risk in the cash flows and the time value of money.

Again, I will agree that this is simplistic but consider the common sense implications:

- The value added by a new user increases with the value of a user, estimated in the last section. A strategy of going for fewer and more intense users may create more value than one with more and less engaged users, a warning that pursuing user growth at any cost can be dangerous for value.

- The value added by a new user decreases as the cost of adding users increases. That cost will be a function of the competitiveness of the business (increasing as competition increases) but also of networking effects. If you have strong networking effects, the cost of adding new users will decrease as you accumulate new users, thus creating a value accelerator for your business.

- The value added by a new user decreases as you become more uncertain about user growth. That uncertainty will be a function of competition and whether the technology that you have built your product or service on is sustainable.

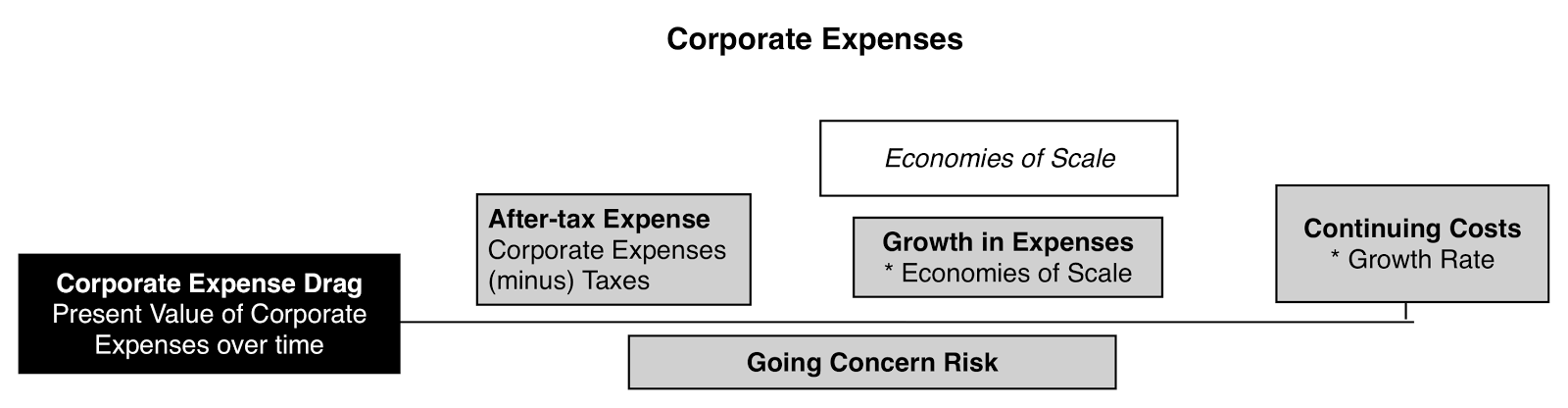

To get from user value to the value of the business, you have to bring in the rest of the company into your analysis. To the extent that you have expenses that are unrelated to servicing existing users or adding new ones, i.e., corporate expenses, for lack of a better term, you have to compute the value of these expenses over time and reduce your value as a company by this amount:

While at first sight, this item may look like wasteful that should be eliminated, it represents both a danger and an opportunity for young companies. It is a danger to the extent that bloated corporate expenses can drag a company's value down, but it can be an opportunity insofar as it is at the basis of economies of scale. If corporate expenses represent necessary expenses to keep a business going, and they grow at a rate much lower than the growth rate in users and revenues, you will see margins improve quickly as a company scales up.

Valuing Uber: A User based Model

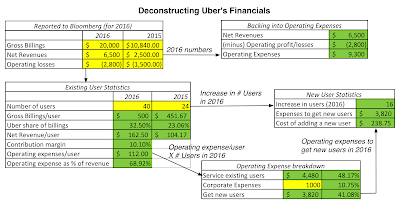

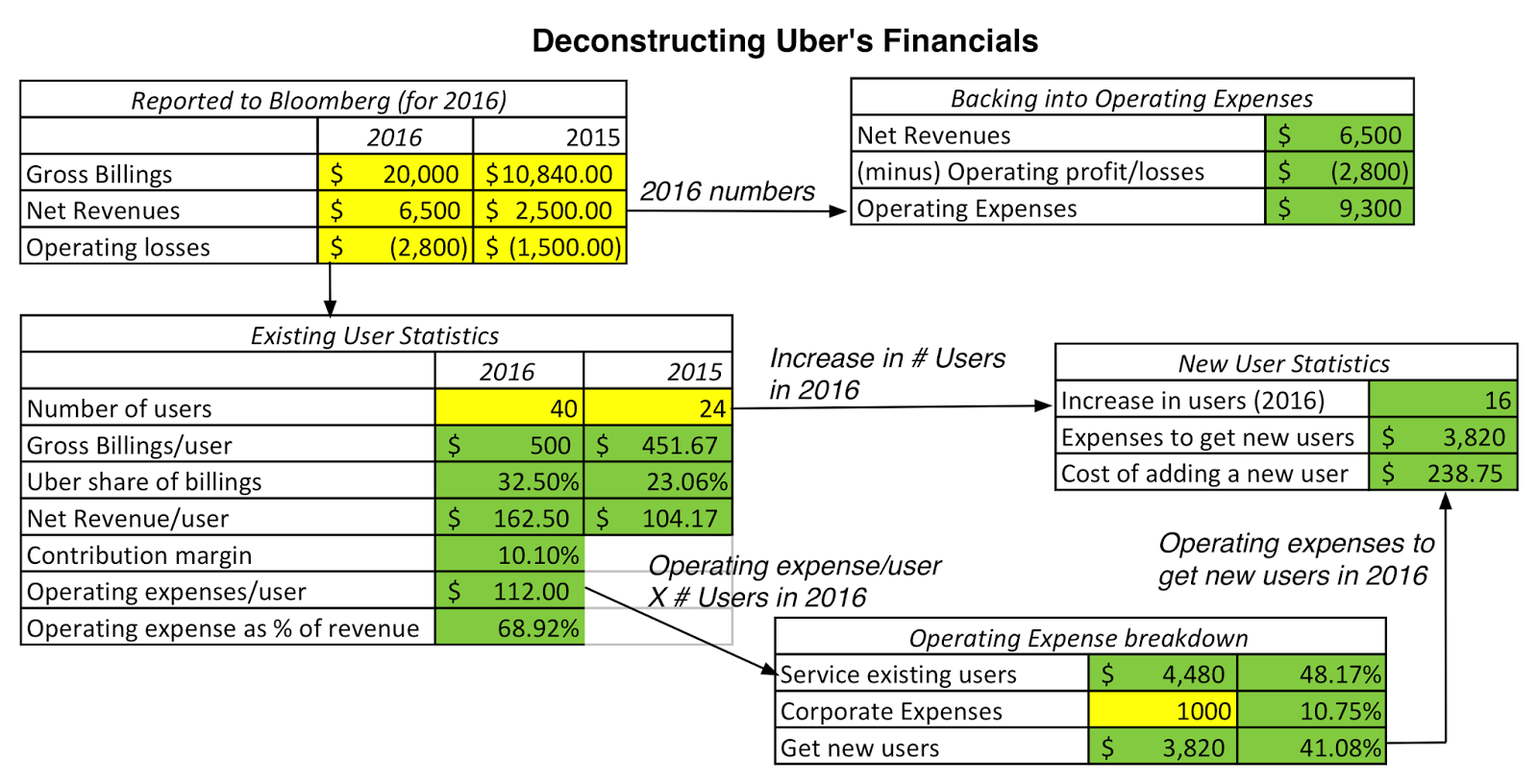

Deconstructing the Financials

Can Uber be valued using a user-based model? Yes, but it will require assumptions about users that are, at best, tentative and at worst, based upon little information. While I will attempt with the limited information that I have on Uber to do a user-based valuation, I will leave it to someone who has access to more information than I do (a VC invested in Uber or an Uber manager) to tweak the numbers to get better estimates of value.

Deconstructing the Financials

The numbers that we have on Uber's operations are minimalist, reflecting both its standing as a private company and its general secretiveness. In 2016, according to the financials that Uber provided to a Bloomberg reported, Uber reported $20 billion in gross billings, $6.5 billion in net revenues (counting all revenues from UberPool) and a loss of $2.8 billion (not counting the $1 billion loss on the China operations). According to other reports, Uber had about 40 million users at the end of 2016, up from 24 million users at the end of 2015. Finally, other (dated) reports suggest Uber's contribution margins (revenues minus variable costs) in its most profitable cities ranges from 3-11% of gross billings and its contribution margin in San Francisco, its longest standing and most mature market, is 10.1%. Bringing in these noisy and diverse estimates together, here are my estimates of user statistics:

These numbers are stitched together from diverse sources and vary in reliability, but based upon my judgments, I break down Uber's operating expenses in 2016 into three categories: to service existing users (48.17%), to get new users (41.08%) and corporate expenses (10.75%); the last estimate is a shot in the dark, since there is no information available on the value. The annual profit from an existing user, based on 2016 numbers, is about $50.50 (Net Revenues - Expense/user) and the cost of adding a new user is about $238/75, and both will be key inputs in my valuation.

Valuing Existing Users

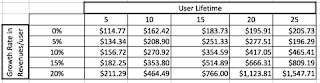

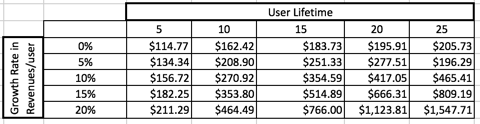

To value Uber's existing users, I use the framework developed in the last section, in conjunction with the estimates that I obtained from the limited financial information provided by Uber. I valued existing users, assuming four additional parameters: a lifetime of 15 years for users, an annual renewal likelihood of 95%, a compounded growth rate of 12% in annual revenues from users expanding their user of Uber services and a growth rate of 9.9% a year in annual user servicing expenses (on the assumption that 80% of the servicing cost is variable). Assuming a cost of capital of 10% (in the 75th percentile of US firms), the resulting value per user and the overall value of existing users is shown below:

|

| Download spreadsheet |

The value per existing user is about $410 and the overall value of Uber's 40 million existing users is $16,412 million. Not surprisingly, this value is sensitive to user stickiness (as measured by user lifetime) and user growth potential (as measured by the growth rate in annual revenues):

In a market where investors swoon at user numbers, this table makes an obvious point. Not all users are created equal, with more intense, sticky users being worth a great deal more than transient, switching users.

Value Added by New Users

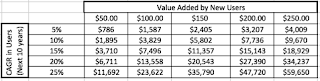

To estimate the value added by new users, I start with the value per user (estimated in the last section to be $410), which I grow at the inflation rate to get expected value per user over time, and use the cost of acquiring a new user from 2016 (about $240/user). Assuming a growth rate of 25% a year for the next five years, 10% between years six and ten and overall economic growth after year ten, I estimate the value added by new users over time. (With those growth rates, I more than quadruple the number of users over the next ten years to 164 million.) In coming up with value, I assume that new user growth is more uncertain than the value created by existing users, and use a 12% cost of capital (at the 90th percentile of US firms) to get today's value.

|

| Download spreadsheet |

The value added by new users, based upon my estimates, is $20,191 million. That value is sensitive to the net value created by each new user (value of a new user minus the cost of adding a new user) and the growth rate in the number of users:

This table illustrates the point made earlier about how some companies will be better off trading off higher value added per user for lower user growth, since there are clearly lower growth/ higher value added scenarios that dominate higher growth/lower value added scenarios in terms of value creation.

Corporate Expenses and overall Value

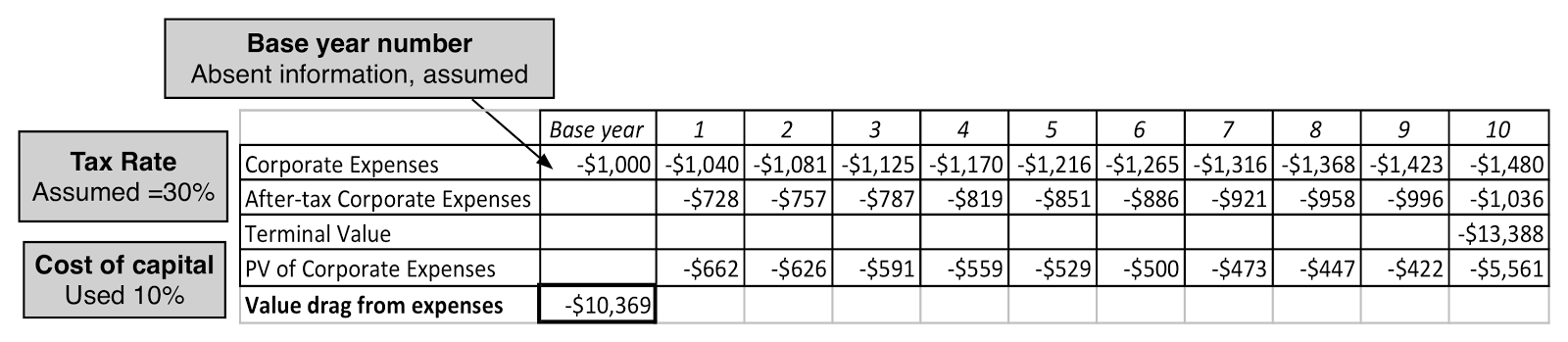

The final loose end is the corporate expense component, a number that I estimated (arbitrarily) to be $1 billion in 2016. Allowing for the tax savings that these expenses will generate and assuming a 4% compounded growth rate, well below the 15.16% compounded growth rate in total users, I estimate a value for these corporate expenses (using the 10% cost of capital that I used for existing users):

|

| Download spreadsheet |

The value drag created by corporate expenses is about $10,369 million. Bringing together all three components, we get a value for Uber's operations of $26.2 billion

Value of Uber's Operating Assets:

= Value of Existing Users+ Value added by New Users - Value drag from corporate expenses

= $16.4 billion + $20.2 billion + $10.4 billion = $26.2 billion

Adding the cash balance ($5 billion) and the holding in Didi Chuxing (estimate value of $6 billion) results in an overall value of equity of $37.2 billion for the company (and its equity, since it has no debt):

Value of Uber's Operating Assets:

= Value of Existing Users+ Value added by New Users - Value drag from corporate expenses

= $16.4 billion + $20.2 billion + $10.4 billion = $26.2 billion

Adding the cash balance ($5 billion) and the holding in Didi Chuxing (estimate value of $6 billion) results in an overall value of equity of $37.2 billion for the company (and its equity, since it has no debt):

Value of Uber Equity = Value of Operating Assets + Cash - Debt = $26.2 + $5.0 + $6.0 = $37.2 billion

This is close to the value that I obtained for Uber on an aggregated basis, but that is a reflection of my understanding of the company's economics.

Pricing versus Valuing Users

As you can see, valuing users requires assumptions about users that can be difficult to make. So, how do venture capitalists and other early stage investors come up with per user or per subscriber numbers? The answer is that they do not. Drawing on an earlier post that I had on how venture capitalists play the pricing game, venture capitalists price users, rather than value them. What does that involve? Very simply put, the price per user at Uber, given its most recent pricing of $69 billion and the estimated 40 million users is $1,725/user ($69,000/40). To make a judgment on whether that number is a high or a low number, you would compare that price to what you the market is pricing a user at Lyft or Didi Chuxing and if naive, argue that the lower the price per user, the cheaper the company. Using the most recent estimates of pricing and users for the five big ride sharing companies, here is what we get:

| Company | Most Recent Pricing (in $ millions) | # Users (in millions) | Price/User |

|---|---|---|---|

| Uber | $69,000 | 40.00 | $1,725.00 |

| Lyft | $7,500 | 5.00 | $1,500.00 |

| Didi Chuxing | $50,000 | 250.00 | $200.00 |

| Ola | $3,000 | 10.00 | $300.00 |

| GrabTaxi | $4,200 | 3.80 | $1,105.26 |

If you follow the user valuation in the last section, you can see why this pricing comparison can be dangerous. The aggregate pricing that you get for individual companies reflects not only existing users but also new users, and dividing by the existing users will give you much higher numbers for companies that expect to grow their user base more. Even if every company is correctly priced, you should expect to see users at companies with less cash flows per user, lower user growth, less intense and loyal users and more uncertainty about future cash flows to be priced much lower than at companies with intense and sticky users, with more growth potential.

The Bottom Line

If your argument against using discounted cash flow valuation (at least in the aggregated form that it is usually done) is that you have to make a lot of assumptions, I hope that this process of valuing users brings home the reality that you cannot escape having to make those assumptions. In fact, the assumptions that you need to make to value a company on a disaggregated basis (based on users or subscribers) are often more involved and complex than the ones that you have to make in an aggregated valuation. That said, I do agree that looking at value on a disaggregated basis can not only give you insights about value drivers but also about questions that you would want to ask (and get answered) if you are thinking about investing in or building a young company whose value is coming from its user or subscriber base.

YouTube Video

Attachments

Previous Posts on Uber

- A Disruptive Cab Ride to Riches (June 2014)

- Possible, Plausible and Probable: Big Markets and Networking Effects (July 2014)

- Up, Up and Away: A Crowd Valuation of Uber (December 2014)

- On the Uber Rollercoaster: Narrative Tweaks, Twists and Turns (October 2015)

- The Ride Sharing Business: Is a Bar Mitzvah moment coming? (August 2016)

- Uber's Bad Week: Doomsday Scenario or Business Reset (June 2017)

Posted by Aswath Damodaran at 12:38 PM

http://aswathdamodaran.blogspot.my/2017/06/usersubscriber-economics-alternative.html

More articles on Gurus

Pick A Side And Fight For It, Keep Your Head Down, Or Flee - Ray Dalio

Created by Tan KW | Jun 26, 2024

Warren Buffett presides over the 2024 Berkshire Hathaway annual shareholders meeting — 5/4/24

Created by Tan KW | May 05, 2024

30 Big Ideas from Seth Klarman’s Margin of Safety (Special Report) - Vishal

Created by Tan KW | Apr 17, 2024

A Young Investor’s Guide to Navigating the Stock Market Wilderness - Vishal Khandelwal

Created by Tan KW | Jan 30, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Apps

Top Articles

1

Kenanga Research & Investment

2

TA Sector Research

BWYS Group Berhad - A Leading Sheet Metal and Scaffoldings Manufacturer

3

4

Kenanga Research & Investment

5

BFM Podcast

6

BFM Podcast

7

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....