HLBank Research Highlights

Rohas Tecnic - Ripe for Further Rebound in Anticipation of Improving 4Q19 Results and a Strong FY19-21 EPS CAGR of 22%

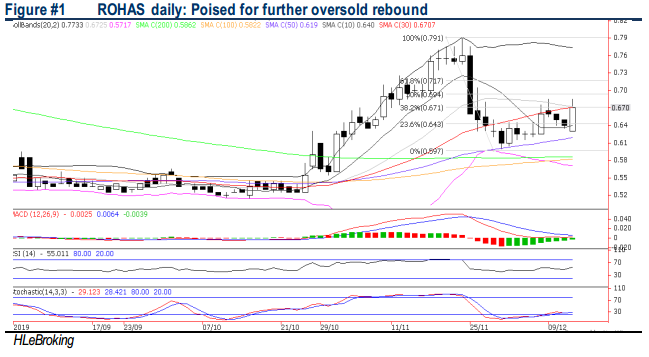

We are sanguine on ROHAS’s mid- to long-term outlook, underpinned by completion of its loss-making HGPT legacy contracts as well as tower fabrication orderbook at RM200m (1.1x cover of FY18 revenue) and EPCC projects at RM340m (1.5x cover of FY18 revenue). In addition, potential fabrication and EPCC orderbook replenishments would be buoyed by Sarawak state’s initiative to rollout 5,000 towers and the transmission line (JV with Muhibbah) from Butterworth to Penang Island which will run parallel to the Penang Bridge (estimated project value: RM1bn). Technically, after building a base above 50D SMA, ROHAS is poised for an oversold rebound towards RM0.695-0.83 levels, in anticipation of a better 4Q results and a strong FY19-21 EPS CAGR of 22% coupled with undemanding valuations at 10.2x FY20E P/E and 0.96x P/B (4% and 40% below PESTECH’s P/E and P/B).

Ripe for further oversold rebound. After hitting YTD high of RM0.79 (22 Nov), ROHAS experienced a 24% correction to a low of RM0.60 (29 Nov) before creeping higher at RM0.67 yesterday. Despite the pullback, the stock is able to build a base above 50d SMA (near RM0.62), which bodes well for further oversold rebound towards RM0.695 (50% FR) and RM0.745 (76.4% FR). A decisive breakout above RM0.745 will augur well for further advance to LT objective at RM0.83 (123.6% FR), supported by bottoming up indicators. Meanwhile, retracement supports are situated at RM0.63 (12 Dec low) and RM0.62. Cut loss at RM0.605.

Source: Hong Leong Investment Bank Research - 13 Dec 2019

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on HLBank Research Highlights

Technical tracker - HLIB Retail Research –19 July 2024 (Short-Selling)

Created by HLInvest | Jul 19, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-29 15:05:00

EMA 5

5 Mins

SELL

2024-07-29 14:55:00

ADX

5 Mins

SELL

2024-07-29 14:55:00

TURTLE SYSTEM 20

5 Mins

SELL

2024-07-29 14:50:00

EMA 5

5 Mins

BUY

2024-07-29 14:50:00

ADX

5 Mins

BUY

Apps

Top Articles

1

Good Articles to Share

Wall Street expert warns stock market is a 'really big accident waiting to happen'

3

Good Articles to Share

How insuring a pet may save money in the long run: Spot Pet CEO

4

Good Articles to Share

5

南洋 - 凭单专栏/温世麟

6

Good Articles to Share

Democrats might put ‘someone else’ in Kamala Harris’ place, GOP sen warns #shorts

7

Good Articles to Share

@tastyliveshow CEO: Betting on black swan events is ‘a complete waste of money’ #shorts

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....