HLBank Research Highlights

Retail Strategy - Finding Certainty in Uncertain Times

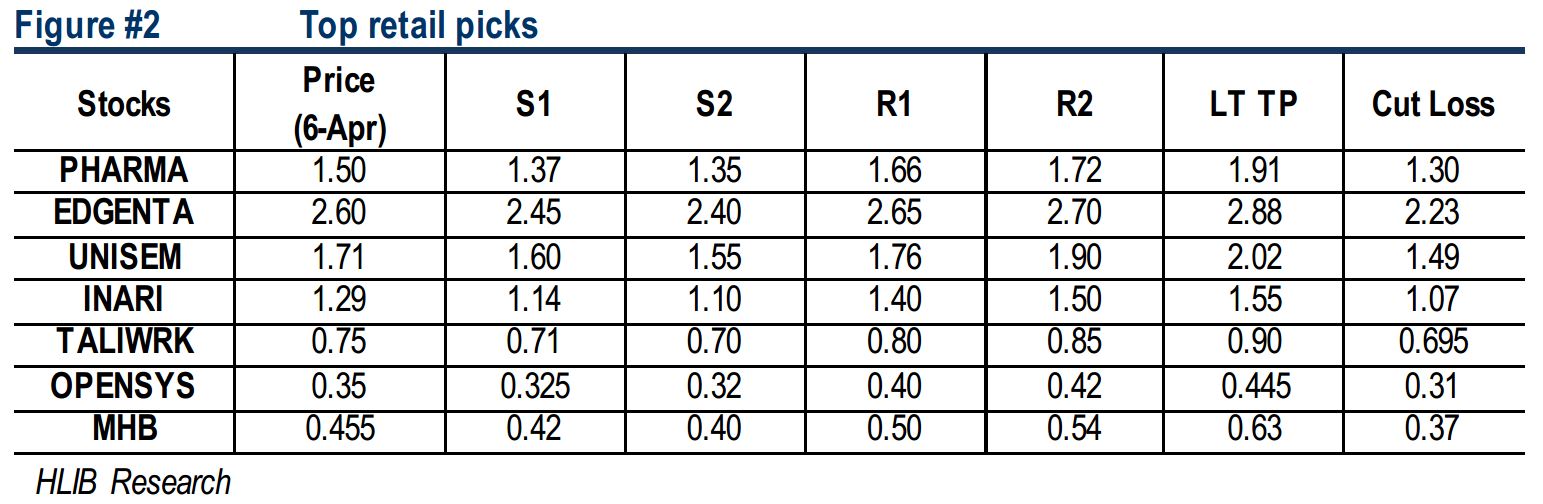

Bursa Malaysia is expected to witness choppy times ahead, with the Covid-19 outbreak globally and IMF stated that the world has entered “recession” as the pandemic has damaged some of the supply chains and soften demand for most of the products/ services. Nevertheless, traders are advised to lookout for certainty under uncertain times, focusing in (i) healthcare (PHARMA, EDGENTA) – where demand would improve in combating Covid-19, (ii) technology (INARI, UNISEM) – unavoidable transition from 4G to 5G and (iii) net cash and dividend yielders (TALIWORKS, OPENSYS, MHB) – ability to sail through these trying times.

1Q20 Market Review and 2Q20 Outlook

Unprecedented global shock: Covid-19 outbreak… Malaysia is going through the movement control order (MCO) of 1 month and most of the cities throughout the world have gone into some degree of lockdown. This has affected economic activities globally, especially the aviation and tourism sectors.

…disrupting global economic activities. Supply chain disruptions and demand for technological products have softened, eventually affecting 1H20 earnings and IMF has warned that world may face recession in 2020, with a recovery in 2021.

Malaysia’s political front. Beside the Covid-19 episode, foreign investors will watch closely on our political situation once the parliament sitting restarts on 18th May. Meanwhile, the Prime Minister has introduced the PRIHATIN stimulus package worth RM250bn in order to cushion the downside risk of Covid-19 impact.

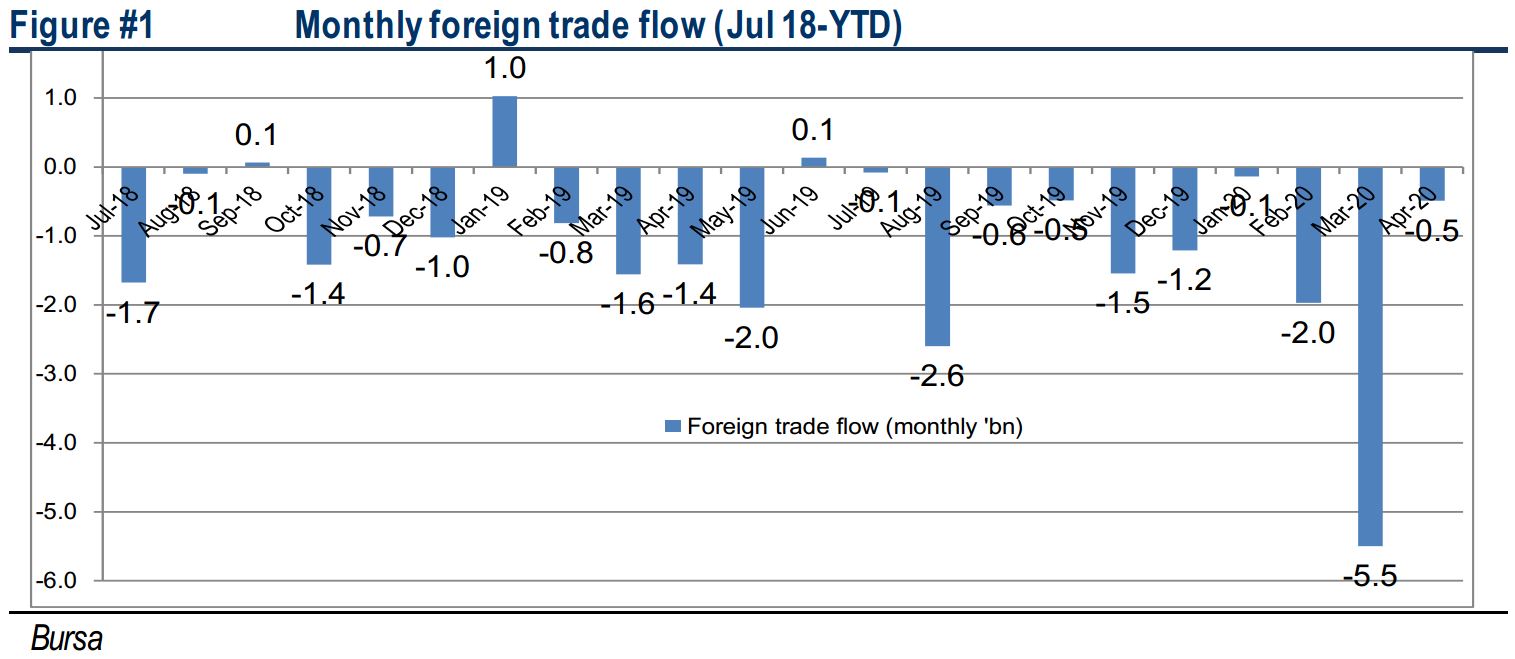

Foreign trade flow remains negative. In 1Q2020, the foreigners have net sold of RM7.6bn in Malaysian equities.

Challenging 2Q20. With Covid-19 affecting business environment, especially under the MCO period, companies will lose out at least 1 month of earnings, hence reflecting a softer 1H20 results. Also, ringgit may stay in the depreciation mode given the softer demand for commodities such as crude oil and CPO. These challenges would persist throughout 2Q20.

Retail Strategy for 2Q20

Certainty in uncertain times of 2Q20. Following the Covid-19 outbreak, we are likely to expect softer 1H20 earnings (which will be mostly reporting in May and Aug), while short term demand shocks may dampen business activities moving forward until Covid-19 is being contained/ vaccine is developed. Hence, it is advisable to look for certainty in uncertain times and looking for stocks within the (i) healthcare industry (higher demand for gloves and medical supplies), (ii) technology sector (progressive rolling out of 5G and NFCP) and (iii) net cash and high divvy yielders.

Healthcare: There is a better chance that the gloves sector will do well in FY20 amid higher demand for gloves following the Covid-19 outbreak. Besides, we believe the recent PRIHATIN stimulus package that involved allocation of RM 1.5bn (RM500m to MoH and RM1bn for Covid-19 equipment and services to combat Covid-19 cases, inclusive of medical services from private hospitals) into the healthcare system in Malaysia would bode well for PHARMA and EDGENTA.

Technology: Although it is likely that this sector might go into a soft period in 1H20 following some slowdown in demand for gadgets after the Covid-19 outbreak, pickup in demand might be seen later in 2H20, accompanied by transition of 4G to 5G and on-going NFCP. Under this sector, we like INARI and GTRONIC.

Net cash and high divvy yielders: In order to sail through smoothly in this cautious business environment, we would favour companies with net cash position and high dividend yielders, such as (i) TALIWORKS, which involved in the water-related segment, (ii) OPENSYS, which served the financial sector and (iii) MHB, may benefit from the recent rebound in oil price.

Retail Stock Picks for 2Q20

PHARMA – Stimulus package allocation to cushion the downside risk

5-year extension of concession. Last year, PHARMA was awarded with a 5-year extension (till end-2024) of concession to source for drugs and medical supplies and distribute for MOH; this is positive as they are in an ideal position for the job given its experience and distribution network that has setup over past 25 years.

RM500m allocation to MoH. For the immediate priority to curb the Covid-19 outbreak, the allocation to the MoH may benefit PHARMA for the distribution of drugs and medical supply to government hospitals and clinics nationwide.

Technical rebound move could persist after a mild consolidation. It has formed a trough formation with a solid technical rebound surging above RM1.30. In view of the short-term overbought position, we think PHARMA should take a mild breather before revisiting range around RM1.66-1.72, followed by a LT target of RM1.91. Support is located around RM1.35-1.37, with a cut loss point set around RM1.30.

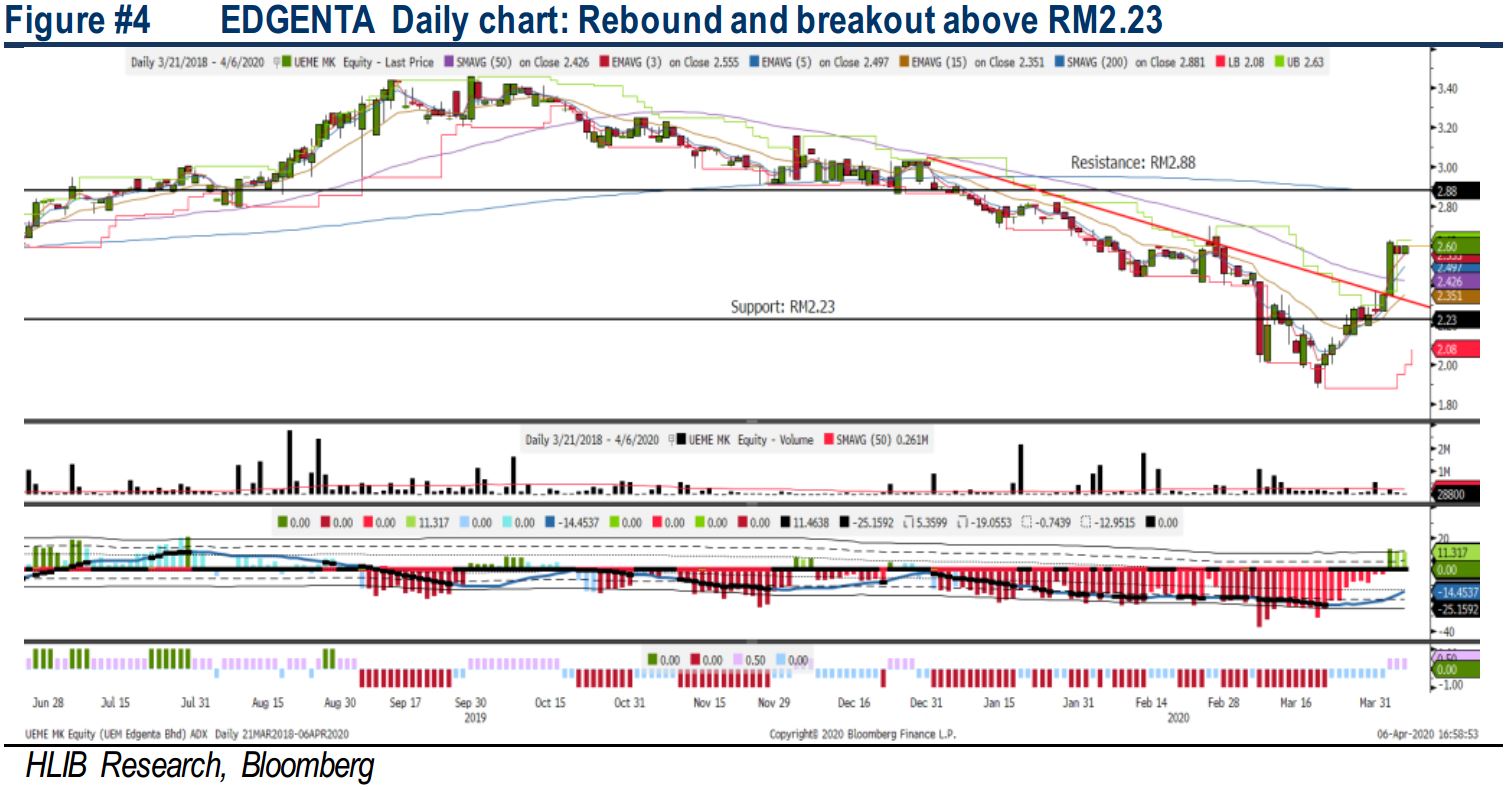

EDGENTA – Beneficiary of RM1bn Allocation to MoH

RM1bn allocation for Covid-19 equipment and services. To tackle the Covid-19 situation, RM1bn is allocated for Covid-19 equipment and we believe this may benefit Edgenta as they may be potentially involved in the procuring process. Also, this may present opportunities for its Biomedical Engineering Maintenance Service (BEMS) division, as there are more devices that will require maintenance moving forward.

Downward trendline breakout. It has experienced a downward trendline breakout around RM2.36 level. According to our indicator, the momentum is positive. Hence, share price may charge higher towards RM2.65-2.70, with a LT target set around RM2.88. Support is pegged around RM2.40-2.45, with a cut loss at RM2.23.

UNISEM – A New Lease of Life

A much-improved entity. Despite the nagging concerns over trade war and Covid-19 pandemic risks, we think UNISEM’s prospect has improved on the back of (i) closure of loss-making Batam plant (likely by 2021); (ii) strengthening USD; (iii) synergistic relationship with Tianshui Huatian Electronics Group (THEG); and (iv) healthy balance sheet (RM0.39 NCPS end-2019). However, the potential of being delisted remains, should it fail to meet the public shareholding spread (end-2019 ~16%).

Undemanding valuations. After tumbling 41% from 52W high of RM2.93 to RM1.71, valuations are undemanding at 12.7x FY21 P/E (Ex-cash 9.8x) and 0.92x P/B, which are 22% and 51% lower than its peers, supported by a strong 19% EPS CAGR from FY19-21.

Steeply oversold with key support at RM1.55. Following the carnage, we believe UNISEM’s downside is limited amid steeply oversold indicators. We see near term sideways consolidation to build a base at RM1.55-1.60 levels. A strong breakout above RM1.76 (20D SMA) will spur greater upside to retest RM1.90 (neckline resistance) and RM2.02 (50D SMA) territory. Cut loss set at RM1.49.

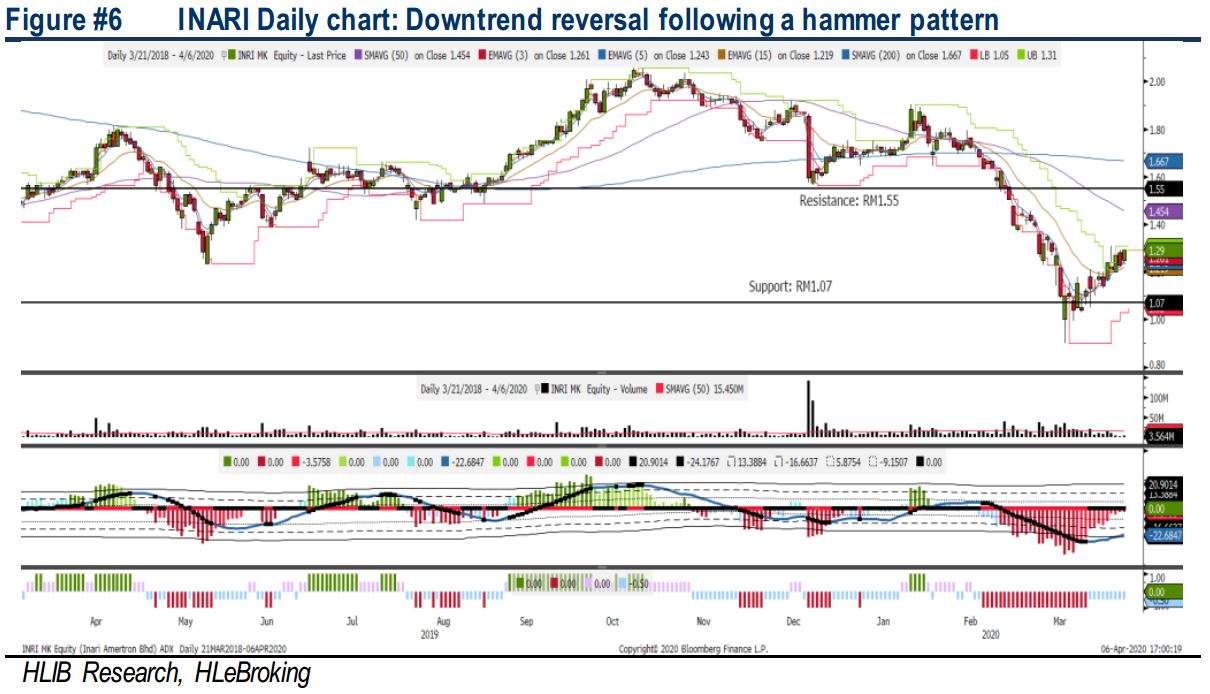

INARI – A Strong Proxy for 5G

Patience will be rewarded. While near-term prospects and earnings are challenging amid Covid-19 epidemic, INARI will potentially benefit from the mass deployment of 5G (which will only take place in 2021) with its expertise in fibre-optics chips and optoelectronics alongside higher RF content in next-gen smartphones.

Covid-19 selloff opportunity. Following a 41% meltdown from 52W high from RM2.09 to RM1.24, the stock is trading at FY21E P/E of 17.7x (ex-cash RM0.17) vs the 5-year average of 23x, supported by decent 4.3% DY. Besides, its strong net cash of RM540m (end 2019) puts the company in a healthy position as the Covid-19 pandemic and protracted US-China trade war will continue to reverberate through the sector, given significant weaknesses in the supply chain and global demand.

Bottoming up following the hammer pattern. Following the Covid-19 plunge to a low of RM0.90, INARI had staged a 43% rebound to end at RM1.29 on Monday. MACD and RSI continue to signal upside bias towards RM1.40 -1.50 (LT target at RM1.55) zones after neutralising the overbought stochastic reading. As long as share price is able maintain its posture above immediate support of RM1.10-1.14, the uptrend remains intact. Cut loss set at RM1.07.

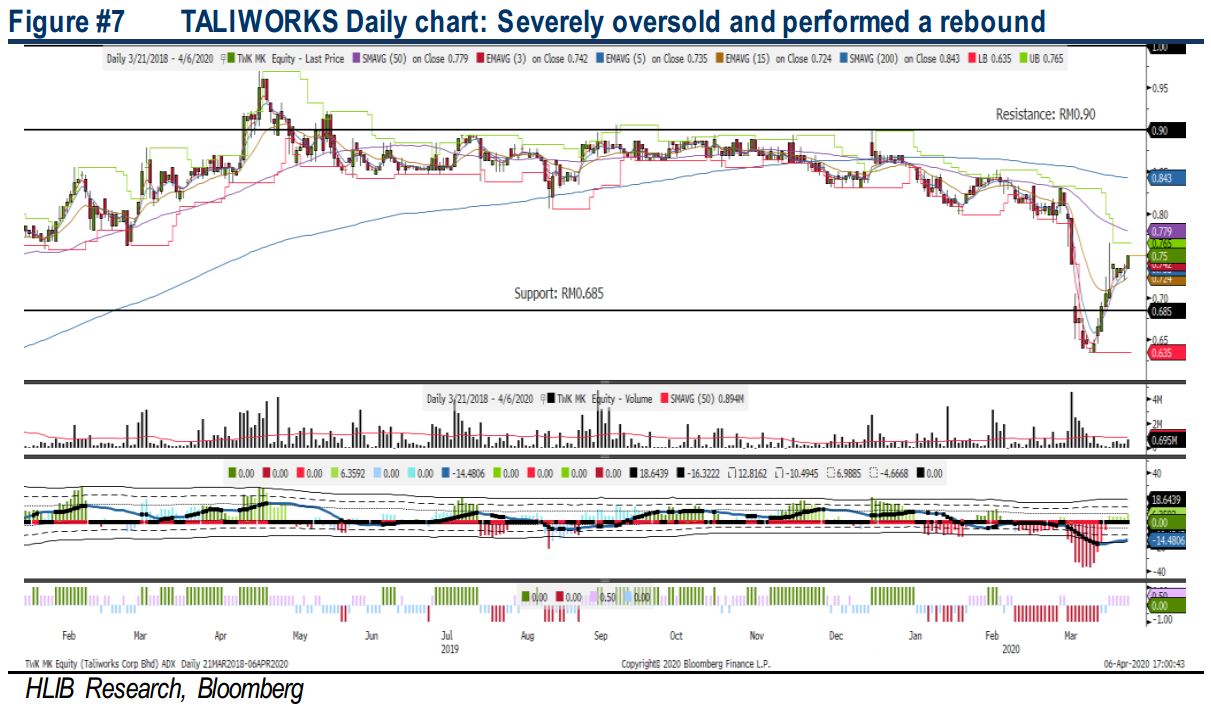

TALIWORKS – Sustainable Water Utility and Toll Roads Player

Mostly neutral to Covid-19. We believe TALIWORKS water operations shouldn't be affected by the Covid-19 event, but its toll road business should see a drop as only essential business are utilising the toll roads during the MCO period.

Sustainable dividend yield from SPLASH receivables. Over the years, TALIWORKS has been a stable dividend paymaster. Given the total securitisation sum of SPLASH receivables is RM660m, management guided that the amount will be deployed through sustainably higher dividend payouts. Should we annualised the 1.65 sen paid out in the recent quarter, it may translate to 8.0% yield based on share price of RM0.75.

Recovering trend after plunged more than 25% YTD. As the share price has rebounded off the recent low of RM0.635, we believe it is heading for a recovery as suggested by the indicator. The resistance is pegged around RM0.80-0.85, followed by a LT target at RM0.90. Support is set around RM0.70-0.71, with a cut loss point set at RM0.695.

OPENSYS – Solutions Provider for Financial and Solar Industries

Dominant position in CRMs and CDMs. OPENSYS has installed >2600 Cash Recycling-ATM (CRMs, ~80% market share in Malaysia) and is a leading supplier of Cheque-Deposit-Machines (CDMs, ~85% of the market). Banks migrated to CRMs due to substantial savings as cash being received from depositors and dispense them to withdrawers. In the last five years, the total number of CRMs in the market has grown exponentially at ~40% CAGR.

OPENSYS launched buySolar, a one-stop online marketplace, partnering with TNB that enables both residential customers and commercial business consumers to purchase solar panels. Also, under the economic stimulus package, TNB will invest RM13bn (RM11bn capex and RM2bn, which includes projects such as LED street lights, transmission and distribution network projects and rooftop solar installations.

Turning into uptrend mode after forming base along RM0.31 -0.325. OPENSYS could have found a decent support along RM0.25 and rebounded above RM0.31. We expect traders to accumulate along RM0.32-0.325 level and the indicator is still suggesting that OPENSYS might charge higher after a mild breather in the near term. Resistance is set around RM0.40-0.42, with a LT target around RM0.445, support is located around RM0.325-0.32, with a cut loss set below RM0.31.

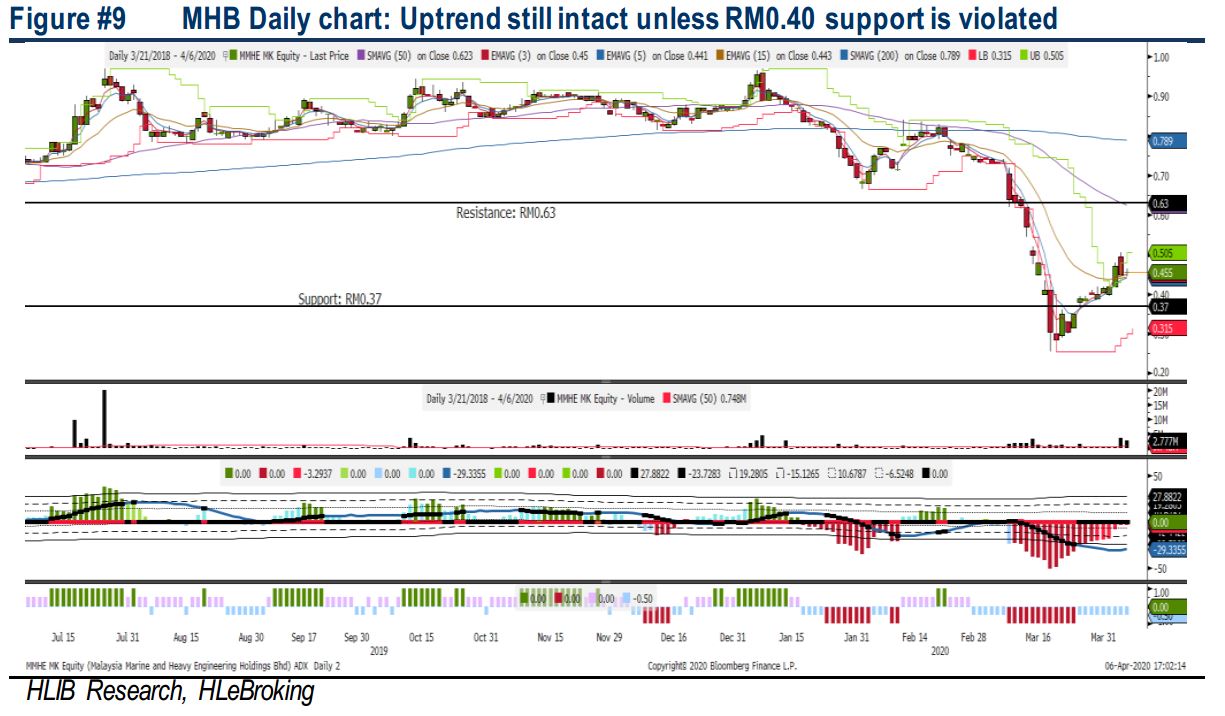

MHB – Solid order book and net cash to weather challenging times

Back to black after FY18/19 losses and solid orderbook Following the recent Bekok EPCIC and Bergading CPP-MRU project wins, its HED’s orderbook stood at healthy RM2.96bn as of end-FY19 (~70% can be attributed to the Kasawari EPCIC award), whilst MHB’s tender book is at a solid RM12.9bn (bulk of them coming from offshore windfarm and onshore module fabrication projects). On the other hand, its MRC segment is likely to improve in the coming quarters on the back of higher dry docking activities coupled with upgrading and retrofitting work for LNG vessels with the implementation of IMO 2020. Dry Dock 1 recorded a 91% utilisation, while Dry Dock 2’s recorded utilisation rate of 78% in FY19 respectively. Dry Dock 3 is at 86.6% completion stage as of 4Q19 and is expected to commence operations by 3Q20.

Undemanding Valuations Supported by Attractive DY and Net Cash Position.

Despite surging 78.4% from low YTD, we are betting of further legs in the stock in anticipation of improving FY20/21, supported by (i) undemanding valuations of 0.3x P/B (5Y average 0.6x), (ii) net cash of RM493m or RM0.31/share (end-2019), could provide stability while awaiting more work orders during these trying times, (iii) enjoy strong parental support (via MISC’s 66% stake) and (iv) could be beneficiary of PETRONAS’ future developments. Also, the recent rebound in crude oil prices could cushion the downside risk of MHB’s share.

Uptrend intact to test RM0.50-0.63. Following the 74% collapse in share prices to a low of RM0.255 from 52W high at RM0.97, MHB had staged a 78.4% rebound to end at RM0.455 on Monday. MACD and RSI readings continue to exhibit neutral to positive trend but the stochastic reading is getting overbought. We may witness a mild pullback near RM0.40-0.42 zones to neutralise overbought positions before resuming uptrend again. Stiff resistances are located at 0.50/0.54/0.63. Cut loss set at RM0.37.

Source: Hong Leong Investment Bank Research - 7 Apr 2020

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

2024-11-15

GTRONIC2024-11-15

UNISEM2024-11-15

UNISEM2024-11-15

UNISEM2024-11-15

UNISEM2024-11-15

UNISEM2024-11-15

UNISEM2024-11-14

INARI2024-11-14

INARI2024-11-14

INARI2024-11-14

INARI2024-11-14

MHB2024-11-14

MHB2024-11-14

MHB2024-11-14

MHB2024-11-14

MHB2024-11-14

MHB2024-11-14

MHB2024-11-14

MHB2024-11-14

OPENSYS2024-11-13

UNISEM2024-11-13

UNISEM2024-11-12

INARI2024-11-12

INARI2024-11-12

INARI2024-11-11

INARI2024-11-11

INARI2024-11-08

INARI2024-11-08

INARI2024-11-08

INARI2024-11-07

PHARMA2024-11-07

PHARMA2024-11-07

PHARMA2024-11-07

PHARMA2024-11-07

PHARMA2024-11-07

UNISEM2024-11-07

UNISEM2024-11-07

UNISEM2024-11-07

UNISEM2024-11-07

UNISEM2024-11-07

UNISEM2024-11-07

UNISEM2024-11-07

UNISEM2024-11-06

INARI2024-11-06

INARI2024-11-06

PHARMA2024-11-06

PHARMA2024-11-06

UNISEM2024-11-06

UNISEM2024-11-06

UNISEM2024-11-06

UNISEM2024-11-06

UNISEM2024-11-06

UNISEM2024-11-06

UNISEM2024-11-05

INARI2024-11-05

INARI2024-11-05

INARI2024-11-04

GTRONIC2024-11-04

GTRONIC2024-11-04

INARI2024-11-04

INARIMore articles on HLBank Research Highlights

Discussions

Be the first to like this. Showing 1 of 1 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

6

7

8

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

RainT

read

2020-04-08 19:13