HLBank Research Highlights

Dufu Technology Corp - Riding on the strong HDD markets

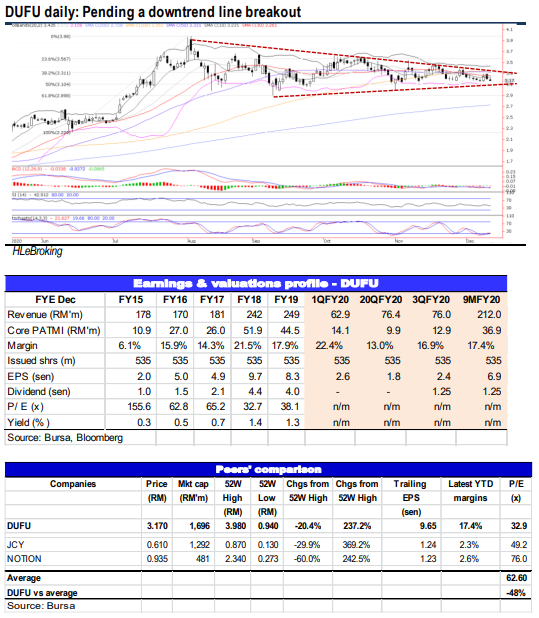

Dufu anticipates another strong 4Q20 results (translating into a better FY20 vs FY19), driven largely by the high HDD demand from the enterprise sector and cloud storage which require more spacers installed in one unit of HDD to equip themselves for 5G technology rollout, big data, powerful analytics, AI and other key innovations to drive growth. Meanwhile, Dufu’s risk mitigation strategy in 2015 to diversify into the nonHDD segment has started to bear fruits. DUFU is also optimistic with the ongoing new projects and potential new customers, which are offering high value creation and carrying better margins than the HDD segment. Valuation is undemanding at 32x trailing P/E (48% below peers), supported by a RM26m net cash.

Pending a downtrend line breakout. After hitting the all-time high of RM3.98 (4 Aug), DUFU share prices slipped 27% to a low of RM2.90 (9 Sep) before closing at RM3.17 yesterday. The stock has been hovering above the RM2.90-3.00 trend line in the last 3 months and is ripe for staging a downtrend line breakout soon. Breaking above the RM3.30 hurdle (downtrend line from RM3.98) will spur prices towards RM3.50 (upper BB) before reaching our LT objective at RM3.80 (monthly upper BB). Cut loss at RM2.88.

Source: Hong Leong Investment Bank Research - 11 Dec 2020

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on HLBank Research Highlights

Technical tracker - HLIB Retail Research –19 July 2024 (Short-Selling)

Created by HLInvest | Jul 19, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

2

save malaysia!

3

4

Good Articles to Share

How insuring a pet may save money in the long run: Spot Pet CEO

5

Good Articles to Share

6

Good Articles to Share

7

Good Articles to Share

North Korea vows 'total destruction' of enemy on Korean War anniversary

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....