Koon Yew Yin's Blog

The Truth Will Set Me Free - Koon Yew Yin

Koon Yew Yin

Publish date: Tue, 11 Feb 2014, 11:19 AM

Koon Yew Yin

0 1,454

An official blog in i3investor to publish sharing by Mr. Koon Yew Yin.

All materials published here are prepared by Mr. Koon Yew Yin

All materials published here are prepared by Mr. Koon Yew Yin

The Truth Will Set Me Free

Koon Yew Yin

Investment success and human psychology are inseparable. After having read hundreds of commentaries of the articles I posted on this forum, I have a better understanding of human behavior. To illustrate the point I am making, allow me to quote a few relevant verses of the Christian bible.

The bible John 8:32 quote “You will know the truth and the truth will set you free” unquote. In the few days as the price of Jaya Tiasa was moving up, I notice the number of ‘Doubting Thomas’ was also reducing. I refer to those disbelievers.

A doubting Thomas is a skeptic who refuses to believe without direct personal experience—a reference to the Apostle Thomas, who refused to believe that the resurrected Jesus had appeared to the eleven other apostles, until he could see and feel the wounds received by Jesus on the cross. I refer to those disbelievers with strong opposing view.

Luke 23:34 quote “Father forgive them for they know not what they do” unquote. I refer to those who ridiculed me with abusive language.

I will take this opportunity to answer some of the questions:

1. Why should I buy Jaya Tiasa when it is selling P/E 87 while KLK P/E 27, SOP 20, TSH 30, United Malacca 20, Utd. Plant 16 ?

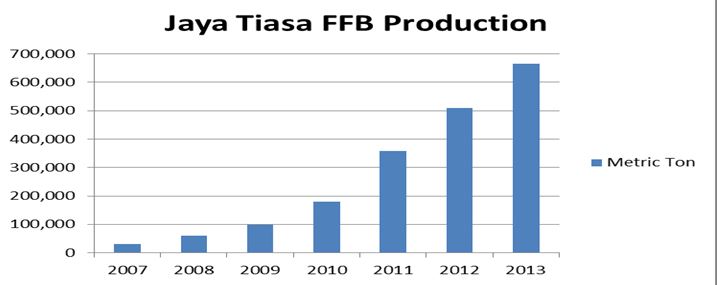

The superior performances of all these companies have been reflected in their share prices already and they are famous and no longer cheap. The price of JT has been depressed for a long time because the average age of their palms is only 5.6 years is currently showing poor earnings. Bearing in mind oil palm production peaks at the age of 11 years, JT has a far better profit growth prospect than the others which is the most important criterion for share selection.

2. Ta Ann is selling cheaper at P/E 26?

My short answer is to look at the following charts and use your imagination to figure out why JT is a better buy.

3. How can you use margin finance safely and avoid Margin Call?

As you know the interest rate for margin loan is only 4.6% pa. To be safe is to buy a share like JT which has a profit growth rate of more than 4.6 %. As long as I am sure that the share can produce more profit than 4.6% pa, I am safe.

To avoid margin call is to use about 70% of the margin and when you feel more confident of the shares you own and general market trend, you can take a little more risk by using more margin.

4. As all shares fluctuate in price, how do you take advantage of this phenomenon?

You must bear in mind that all share prices cannot go up or go down indefinitely for whatever reason. When the price is down, use margin finance to buy more shares and when the price has gone up, sell those shares which were bought with margin loan. With some practice, you can improve your technique in your buying and selling to maximize profit.

5. Jaya Tiasa has too much loan?

It is a good sign as long as the loan is properly use to expand its business. When companies are holding huge amount of cash in fix deposit, it only shows that the management cannot use the cash to generate more profit than the fix deposit rate of 3%.

6. Why don’t I buy shares which are always selling at low P/E ratio and high dividend yield?

Hexza and Symphony Life are 2 good examples. Their shares have been selling at low P/E and high yield for many years. The reason is that they do not have profit growth. Their profit remained the same for many years. Some people will buy these type of shares for their high dividend yield but my aim is different. I want to make money faster.

Note: Jaya Tiasa is my major holding and I am not asking you to buy. Since the start of 2014 it has performed better than the KLCI which indicates that more investors are interested to buy it.

I have organized a talk at 11am on 16th Feb, Sunday at the Club House, Meru Golf Resort, Jelapang, 30020 Ipoh. Those who are interested please email to tell me the number of people who will be coming so that I can arrange a good lunch for you all. My email address: koonyewyin@gmail.com.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Koon Yew Yin's Blog

Plantation stocks comparison - Koon Yew Yin

Created by Koon Yew Yin | Dec 26, 2024

Indonesia is the biggest palm oil producer in the world. Indonesia plans to implement biodiesel with a mandatory 40% blend of palm oil-based fuel from Jan. 1 next year, a senior energy ministry offi..

All plantation companies will report historical record profit - Koon Yew Yin

Created by Koon Yew Yin | Dec 13, 2024

Indonesia remains committed to start implementing a 40% mandatory biodiesel mix with palm oil-based fuel, or B40, on Jan 1 next year, its chief economic minister said. Indonesia, the world's largest..

Who buys palm oil - Koon Yew Yin

Created by Koon Yew Yin | Dec 12, 2024

Indonesia is the world's largest producer of palm oil, producing an estimated 46 million metric tons in the 2022/23 marketing year. Indonesia also exports over 58% of its production, making it the w..

TH Plant is the best buy - Koon Yew Yin

Created by Koon Yew Yin | Dec 03, 2024

Indonesia is the largest palm oil producer in the world. Indonesia plans to implement biodiesel with a mandatory 40% blend of palm oil-based fuel from Jan. 1 next year, a senior energy ministry offi..

What is Bipolar Disorder? - Koon Yew Yin

Created by Koon Yew Yin | Nov 25, 2024

My younger brother who was a dentist had bipolar disorder. Unfortunately, he committed suicide about 12 years ago.

CPO price is rising rapidly as shown by chart below - Koon Yew Yin

Created by Koon Yew Yin | Nov 22, 2024

All plantation companies are reporting better profit for the quarter ending September when CPO price was about RM 3,800 per ton.

MHC Reported Increased Profit - Koon Yew Yin

Created by Koon Yew Yin | Nov 21, 2024

Indonesia is the biggest palm oil producer in the world. Indonesia plans to implement biodiesel with a mandatory 40% blend of palm oil-based fuel from Jan. 1 next year, a senior energy ministry offici

Why all plantation companies will continue to report more profit - Koon Yew Yin

Created by Koon Yew Yin | Nov 20, 2024

Indonesia plans to implement biodiesel with a mandatory 40% blend of palm oil-based fuel from Jan. 1 next year, a senior energy ministry official said recently, lifting prices of the vegetable oil...

Who will win the Presidential Election? - Koon Yew Yin

Created by Koon Yew Yin | Oct 30, 2024

Latest poll on 30th Oct 2024

Who will win the Presidential Election? - Koon Yew Yin

Created by Koon Yew Yin | Oct 30, 2024

Latest poll on 30th Oct 2024

Discussions

8 people like this. Showing 42 of 42 comments

Stock168 ANOTHER UNDERVALUED STOCK

Dutaland owed 12000 ha plantation Land worth 840m (12000xrm70000 per ha), Abandant Duta Grand Hotel totalling build up to 29th floor (surpose to build 52 storey height) worth 350 m situated In Jalan Tun Ismail and Jalan Ampang KL Town, holding of 52% of 73 acres prime Land In montkiara worth 345m( 73 x rm9.1m/acre x 52%) value at 9.1m/acre consider very prudence as recent transacted price of jalan Ampang current RM 3000/ft. And a Few piece Land In Kl centre, shan alam, Melaka centre etc etc worth 200m and further more with only 80m debt, NTA=1.97. (840m+345m+350m +200m-80m debt)/840m share. besides this, year production of 125,000 ton of FFB Now trade at RM 540/ton.

Dutaland coming quarter result around 5m profit. The turnaround result come from the completion of 38 Shop Houses In Seremban by wholely subsidiary and quarter production of 25000 ton FFB. The FFB price currently trade at 540/ton campare to last quarter 400/ton. Further reduced some interest due to sold out Olympia Plaza. Good rating By analyst can be foresee.

2014-02-11 11:04

First of all, u can't use quote from bible coz bible is all about tree of life. This forem is all about tree of knowledge. If u r Christian, pls b sorry n ask for God's forgiveness. 2ndly, it's true tat JTiasa has increasing production down the road. Bear in mind tat increasing production doesn't mean increasing profit. It's commodity n it's price fluctuates. Wat if someone bet heavily in JTiasa with margin loan n expect profit in few yrs time but cpo price plunge 2 unprofitable level? How r they going 2 service their loan? They might end up selling red.

2014-02-11 11:13

One would make money faster by buying Coastal Contracts. They have just announced winning a contract in Mexico which will set them ahead for RM155 million per annum starting year 2015. The contract would be for 8 years. In other words, Coastal is set for RM155 million per annum starting from 2015 for the next 8 years till 2023. On an average of 15 to 20% profit, Coastal is poised to make 23.50 to 31 million per annum just from this Mexican deal alone. Moreover, Coastal business module is you pay before they build. We foresee Coastal hitting RM6 or 44% increase from its current price of RM4.15 before year end. This is akin to buying the winning horse even after the race.

2014-02-11 11:18

I m a small holder myself n I've seen people fail in this bussiness. Some bought a plantation but fail 2 service the loan due 2 cpo price plunge. Some spent 5yrs time 2 cultivate but when it's time 2 harvest cpo price plunge. Again, share is equity. Oil palm is commodity. U r betting on commodity through equity. U r betting on uncertainties through uncertainties. U make it even more uncertain when it involve margin loan.

2014-02-11 11:19

Dutaland? Please check the chequered history of the principal before you promote his stock. How have minority shareholders fared? Can a leopard change its spots?

2014-02-11 11:36

dear cariyoyo,

I noticed that you have correctly predicted the rise of Coastal Contracts from RM2.20 in May 2013 or earlier. You have also predicted the rise of KSL Holdings. I note that you are predicting stocks like P&O and IJM Land. What make you so sure that the deal in Mexico would not turn sour for Coastal? Anyway, you have predicted Coastal correctly since early last year and hope you are right this time that it will hit RM6 before end year. Looks like Coastal Contracts is in a more stable condition than Jaya Tiasa going by KinSoon Kok's reading / analogy.

2014-02-11 11:37

what's your comment on Coastal Contracts, Mr. Koon. I noticed from the latest annual report that your buddy, Dato Yap Lin Sen holds more than 3 million shares in Coastal. Do you think Coastal is a better bet than Jaya Tiasa?

2014-02-11 11:38

Always buy at your own risks. we need to be fair to Mr Koon ( sharing his ideas) does NOT meant you need to follow his style. Cheers to everyone reading this blog. make money and stay healthy

2014-02-11 11:50

Mr Koon, fwe questions in my mind, that may be you can help to clear

1) Why the log concessionaire business is doing so bad in recent years? Is it due to poor log price?

2) The FFB is increasing but JT is still not posing good profit yet?

3) The cash situation in JT is quite poor. I am doubt if JT still can go thru if the cashflow doesnt come on time. JT has called for a cashcall not too long ago.

2014-02-11 12:50

JTiasa, get some insights here http://stockpip.com/is-it-time-to-buy-palm-oil-shares/

2014-02-11 13:54

I was studying JT earlier but did not go very far due to political strings/chains in there. Political connections can do wonders to a company but it can also do the reverse for their own gains. Appreciate your view and analysis on this political front, Mr Koon.

Thanks.

2014-02-11 14:50

Less than mediocre earnings in the last five quarters; high debt; current ratio less than 1; Calibre of management: incompetent to doubtful because of poor showings in earnings; dividend yield: less than 1. There are just too many red flags in the stock. Wait until you are close to the tunnel and can see the light more clearly. Better to buy high and sell higher than to buy low and sell high for those who do not have the financial muscle to buy and hold.

2014-02-11 14:57

Since more than 100 people have requested for seat reservation, I have to change the venue to Ipoh YMCA because Meru Golf Club is too small. The time and date remain unchanged. I will try to inform all those who have requested seat reservation.

2014-02-11 14:58

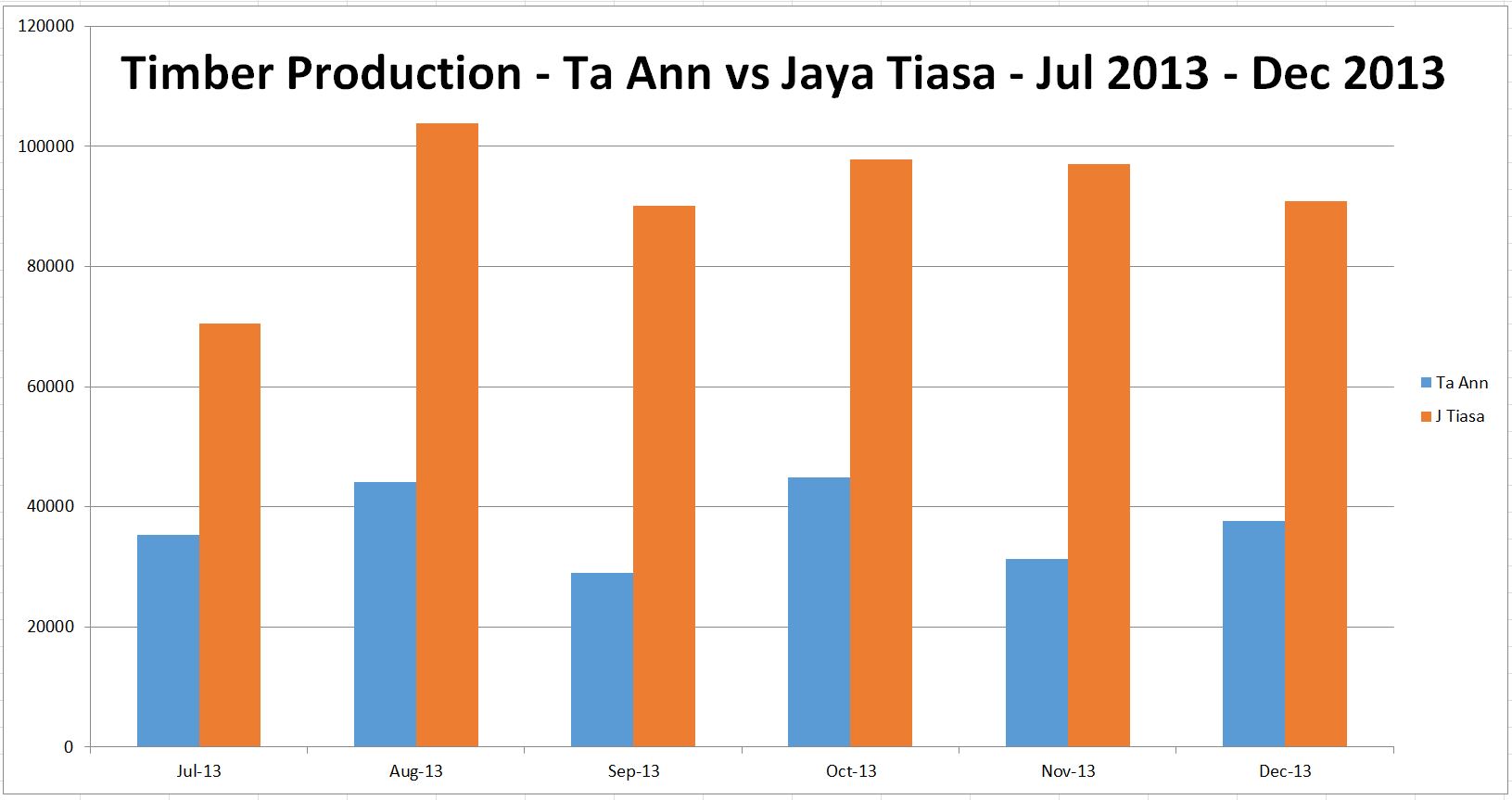

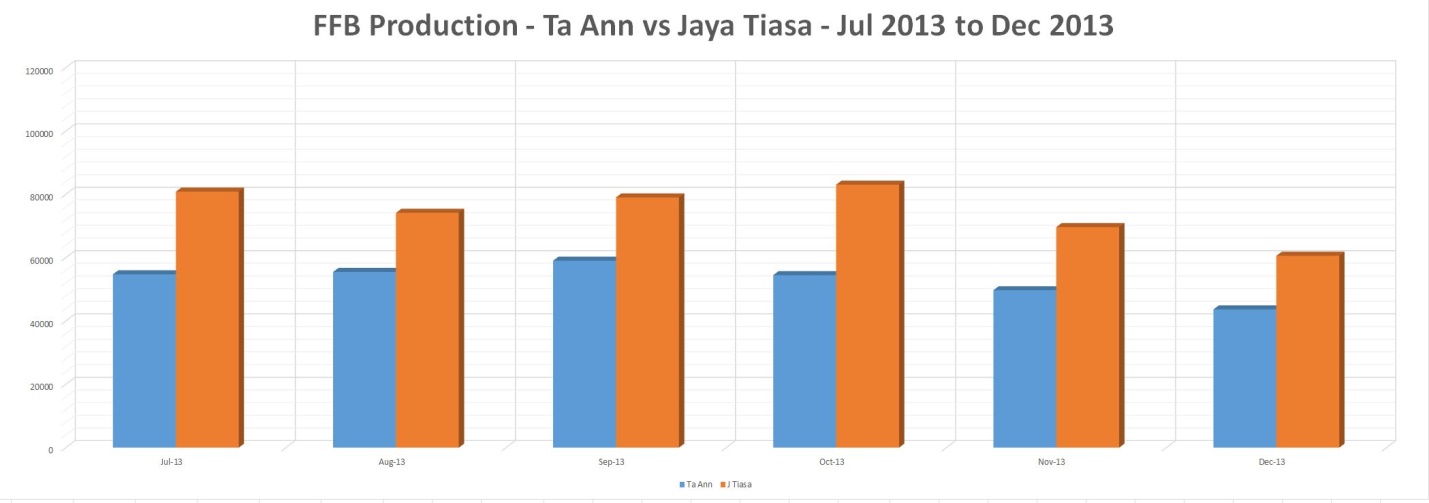

High FFB production doesn't automatically translate into higher profit.

JTiasa's plantation division was managed to produce high FFB of 708,859 tons for the past 12 months but it suffered a loss.

Look at TAAN, with FFB production of 531,744 tons for the past 12 months, it was able to deliver a profit of 61 million.

The latest financial results of both companies shows a profit. Jtiasa's plantation unit was delivered a minimal profit but its FFB production 38% higher comparing with TAAN. It seems something not right.

JTiasa

Quarter ended 30 Sep 2013 ( Palm oil segment )

FFB production - 234,052 tonnage

Turnover : RM 77,761,000

Profit : RM 9,577,000

Palm oil segment ( past 12 months )

FFB production: 708,859 tonnage

Turnover - 251,806,000

Loss before tax - ( 12,247,000 )

TAAN

Quarter ended 30 Sep 13 ( Palm oil segment )

FFB production - 169,326 tonnage

Turnover - 88,495,000

Profit before tax - 29,582,000

Palm oil segment ( past 12 months )

FFB production - 531,744 tonnage

Turnover - 274,257,000

Profit before tax - 61,497,000

2014-02-11 17:11

I have accepted 120 people to attend my talk. Since all the seats are taken, I have no more seats for new applicants. Thank you for showing your interest.

2014-02-11 17:53

Mr Koon,

For the benefit of those who cannot make it to the gathering, possible to video tape it for wider audience? Or a copy of your slide presentation?

Thanks.

2014-02-11 18:28

TAAN

Weight average number of shares: 370,537,000 ( 38.3% of Jaya Tiasa )

Information as at 31 Dec 2012

Land bank: 97,855 hectare

Planted area : 35,345 hectare ( 55.6% of Jaya Tiasa )

Mature area: 26,161 hectare ( 47.2% of Jaya Tiasa )

Some may have a perception that Jtiasa is better than TAAN because Jtiasa would yield high FFB production given its large planted land. If you look into more detail analysis, you would see the difference.

Let say, price of CPO up by RM 100. Both Jtiasa and TAAN would enjoy higher profit from the price increase. But the number of ordinary shares of TAAN is lower than 61.7% comparing with Jtiasa. To achieve the equal EPS of both companies for the contribution from palm oil segment , Jtiasa would have to produce 61.7% higher of FFB.

Currently, the FFB production of Jtiasa is 38% higher than TAAN. Base on the existing planted area ( 55.6% of Jtiasa) of TAAN , It's unlikely Jtiasa would produce 61% more FFB than TAAN in the end.

Is It Jtiasa better than TAAN?

2014-02-11 18:44

What is the longer future development for Jtiasa & TAAN?

Jtiasa owns 7,326 hectares of vacant plantable land and will be fully planted its 70,900 hectare of land in 2 years.

TAAN owns 97,855 hectares of land bank. It acquired 30,989 hectares of vacant land in year 2012. Plantable is of course more than 70,900 hectares. TAAN has the potential to double its planted area till 70,900 hectares in the next few years.

Further more, the costs of planting RM/hectare for TAAN is much lower. It costs about RM 9,000 to plant an hectare of oil palm land. To achieve 70,900 hectares of planted land, TAAN may have to spend additional RM 320 million ( 35,555 hectares x RM 9,000/hactare ) only. The total plantation expenditure would be RM 639 million.

What about JTiasa? It may spend another RM 157 million ( 7,326 hectares x RM 21,500/hectare ) to plant the remaining 7,326 hectares land. The total plantation expenditure would be RM 1.525 billion.

What a huge difference for planting the same size of land of two companies. It may costs RM 639 million to TAAN but RM 1.525 billion to Jtiasa.

2014-02-12 12:10

I don't really know how the business run in Jtiasa. By looking at the past 12 months performance and planted costs/hectare, I would say Jtiasa's business has not been run effectively by the existing management team.

2014-02-12 21:07

I have to changed the venue to Ipoh St. John Ambulance hall which is opposite the Ipoh YMCA. The time 11am and date 16th Feb Sunday remain unchanged. All the 150 seats have been taken and I cannot accept any more new applicants.

2014-02-12 22:23

I wish to invite Up_down to my talk so that we can discuss because he seems very analytical and knowledgeable where as I just look at the broad picture.

2014-02-12 22:31

Uncle Koon! just joking ya.....life is boring without joke but of course Transformer is a joke on his own....lol

2014-02-12 22:40

Just don't make uncle Koon transform lah.....he is not just a proven super investor for no reason......don't make him turn green, you transformer cannot handle lar

2014-02-12 22:53

I wonder if I say I love uncle Koon , I will get a flag......but I truly do......

2014-02-12 22:58

My sifu make enuf 15 yrs ago n bought a bank in oversea n retired liao... more super duper than him la.

2014-02-12 22:59

But my uncle make so much he bought a plantation......but he cannot retire....aiya

2014-02-12 23:00

Mr Koon, I did learn a lot from your article on how to become a super investor. In order to be more successful in investing, I have to think from the business perspective with the help of margin financing to increase my returns.

2014-02-12 23:33

Wilmar to stop buying CPO fom Sarawak

February 14, 2014

Land Development minister James Masing said the livelihood of the people in the rural areas was not to be negotiated with the international community

KUCHING: Sarawak may lose some RM400 million in sales tax revenue a year from oil palm products following the decision of a multinational refinery company’s refusal to buy crude palm oil (CPO) from mills in the state.

A Singapore-based company, Wilmar International Limited, which has its refinery plant in Bintulu, has written to the state government to inform that the company would stop buying CPO produced from oil palm trees planted in forest areas and peat swamp land in the state from 2015 onwards.

2014-02-15 01:42

Seminar at 11am on 16th Feb Sunday at Ipoh St John Ambulance hall. I have rearranged the seating and now I have an additional 40 seats to offer to those who are interested. Please write to me especially those whom I have turned down.

2014-02-15 12:24

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

Dragon Leong blog

2

Stock Market Enthusiast

Feng Shui Market Outlook for FBM KLCI in the Year of the Wood Snake (2025)

3

The Alpha Trader

5

Stock Market Enthusiast

3 Resilient Stocks That Defied Malaysia’s Market Slump in January 2025 - #GCB, #ABMB, #CDB

7

THE INVESTMENT APPROACH OF CALVIN TAN

REPOSTING: BUSINESSES THAT LAST TILL THE END OF TIME IN BIBLE PROPHECY, Calvin Tan Blog

8

MQ Market Updates

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

haikeyila

Please stop quoting the bible unnecessarily.

2014-02-11 11:02