Jay's market diary

Prestariang and the game changing SKIN contract

Disclaimer

First of all, little bit of disclaimer, as there are very little details provided in the announcement, what I’m about to share is what I understand. Eventual recognition may turn out to be different. Please interpret it with your own discretion.

What we do know

From the little details we do know from the announcement are:

1. the contract is a concession, not pay per transaction like what MYEG or SCICOM usually earn. Prestariang does the job and government pay them, period.

2. SKIN will be a build, operate, maintain and transfer model. In layman’s term, Prestariang build the system for operations in the first 3 years, maintain it for the next 12 years (total 15 years) and eventually ownership will be transferred back to government at the end of the concession period

3. payment will be deferred whereby Pres will build and implement the system for first 3 years without receiving payment but government will pay them in 12 subsequent annual payments of RM294.7m.

What does the deferred payment mean?

Just imagine say your friend hire you to build a house for him, but instead of paying you upfront or by progress, he negotiated a deal so that he can pay you by instalment over certain number of years. Of course by now even the most naïve of you would be wondering why should I do him such a favour? So for him to broker such deal, he has to compensate me by including interest in the annual payments over the repayment period. Only then it’s fair. So RM294.7m x 12 years or RM3.54b in total is government’s payment to Prestariang not just for the SKIN contract but also the interest for the concession period.

What’s the effect on company’s financials?

Now comes the tricky part. I will try to apply my own accounting understanding on IFRIC 12: Service Concession Arrangements which explains accounting treatment for concession biz. I will try to make it as simple as possible. But certain essential parts may be difficult to understand by those who are unfamiliar with accounting in which case, you can simply choose to believe it or not. If you don’t, you can stop reading because the numbers below would be essentially garbage for you.

Key accounting questions

Key question 1: Should revenue and costs be recognised in the first 3 years, next 12 years or evenly over 15 years?

Accounting 101: accruals concept means that revenue and costs are recognised as and when they are incurred, not when cash payment is received or paid. So my interpretation is revenue and costs should be recognised in the first 3 years when work is done, not when payment is received in the next 12 years while maintenance revenue will be recognised in the 12 years maintenance period. In other words, my take is that the development revenue for the build and deployment phase should be recognised by progress for the first 3 years while maintenance revenue will be recognised when maintenance works are carried out.

Key question 2: If revenue and costs are to be recognised, how much of the amount?

Costs are straightforward where the exact amount should be recognised. Revenue is a bit trickier. We have established earlier that the RM3.54b includes both the contract value and interest element. So what should be recognised in the revenue would be the contract value without interest element/the fair value of the contract. Calculations will be shown later.

Key question 3: What about the interest element?

Yes, the government is also paying for the interest over the 15 years concession period so interest element should also be recognised as other revenue over the concession period with “unwinding of discount” method. Details to be provided later.

Key question 4: Impact on balance sheet and cashflow?

One big item will show on balance sheet which is receivables. Receivables will blow up in the first 3 years as government continues to avoid paying. By the end of 3rd year, the receivables amount should be equal to the fair value of revenue recognised and subsequently adjusted.

First 3 years there will be cash outflow without cash inflow (specific to SKIN). Logically speaking, it’s not sustainable, which means Prestariang will need to raise equity or debt financing.

Simply said, just imagine a credit sale with extremely long credit period. So your revenue is recognised when you make the sales (in this case, you need 3 full years to complete the sales), customers doesn’t pay you yet so you don’t get cash but there will be receivables. And because this is long term, so you are going to charge your customers for paying you in deferred terms.

For those who are interested in further reading, all the above is based on my understanding of IFRIC 12: Service Concession Arrangements. Concession companies like Menang Corp, Triplc are examples of companies who were awarded government concession to build government universities and they do adopt IFRIC 12.

So how much exactly is the revenue?

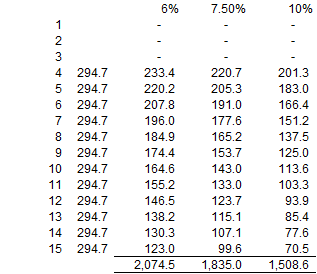

So now we have established the above, first on revenue. We know that we should recognise fair value so how much is it? Fair value is essentially the present value of the future payments aka contract value without interest element. So we need to establish a discount rate. Government payment should be relatively low risk so I think 7.5% is fair. If we discount the 12 payments by 7.5%, we get a fair value of RM1.83b. But if we discount it based on 6% or 10%, the fair value would be RM2.07b or RM1.5b.

Basically the lower the discount rate, the higher the fair value. But why is there such difference? Recall earlier we establish that RM3.5b includes fair value revenue and interest revenue. So if discount rate/interest rate is lower, which means interest revenue is lower while fair value revenue is higher. For example, if fair value revenue is RM1.8b, interest revenue is RM1.7b. If fair value is RM1.5b, interest is RM2b. Eventually, a total revenue of RM3.5b will be recognised over the 15 years period and match with cashflow, it’s just a matter of apportionment.

How much are the costs?

This we do not know. We would need to assume a pre-tax IRR for the project. For university concession usually it’s implied 12%, of course software development may carry much higher IRR compared to traditional university construction but let’s be conservative and just apply a slightly higher IRR of 13%. This means implied costs is around RM1.5b to be incurred over 3 years.

Interest element

The interest revenue will be dependent on what discount rate you use. For illustration purposes, if you use 7.5% to derive fair value revenue, so after first year you recognise RM610m fair value revenue (RM1.83b/ 3years), interest revenue would be RM46m (RM610mx 7.5%). If 10%, you recognise RM500m (RM1.5b/ 3 years) and RM50m interest (RM500m x 10%). Interest will continued to be charged on cumulative amount net of payment received, i.e. second year will be (RM610+610-0 payment received) x 7.5% so on and so forth until the whole receivables is cleared and entire RM3.5b revenue is recognised.

Plucking in the numbers

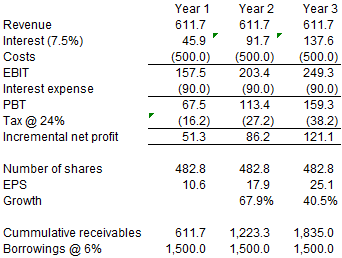

If we assume 7.5% discount rate:

Assumptions:

1. The above fair value and interest revenue is dependent on discount rate used (7.5% for illustration).

2. Costs to be incurred is dependent on IRR. If IRR is higher, then costs actually should be lower, vice versa.

3. Progress is assumed to be even, in reality it may not.

4. 100% borrowings are assumed to undertake the costs. 6% is used because Prestariang can easily issue a bond with the underlying backing of the 12 annual instalments by government. These type of bonds don’t carry high interest because payment is almost “guaranteed”.

Has market priced in the contract?

At closing price of RM2.45, the market cap is around RM1.19b. The current profit is around RM15-20m pa since its peak in 2013, which means a PE of above 60 times. But what we know from examples like MYEG or even Prestariang itself a few years back, market is willing to pay high PE for these government software stocks in anticipation for high growth.

Assuming current year ends up with RM20m net profit, once the SKIN project kickstarts, the net profit will multiply to around RM140m (RM120+20m) by the 3rd year or a CAGR of 91%.

For a combined (current biz + SKIN) forward EPS of 14.6c, target price will be dependent on how many times PE you think it’s fair. 20 times PE would be RM2.92 or 30 times would be RM4.38 and it could still be arguably not expensive if earnings indeed are growing at 91% 3-year CAGR.

Even after the 3 years “explosion” period, RM1.8b receivables at 7.5% would still give you RM135m EBIT pa in the 4th year (which will slowly go down as government pay the instalment over the years). In the most optimistic scenario, from what we have seen from MYEG’s case, after the end of concession, government may even extend the concession for the company to operate the system.

Alternatively, some may argue that concession is best evaluated based on discounted cashflow. If I apply same 7.5% discount rate, NPV of the project after full repayment of interest and borrowings is around RM340m or adding RM0.70 per share to the current value.

All the above are done without evaluating the existing projects of Prestariang as well as other potential future projects. If you are interested in the company’s prospects, please refer to the annual reports or analyst reports. All I tried to illustrate here is how huge this SKIN contract is to Prestariang. So I believe the market has priced in the award of SKIN to a certain extent (since it was announced last year) but haven't fully appreciate its magnitude (as award value is just announced and bottom line impact unclear).

Conclusion

SKIN is easily a game changer for Prestariang regardless of the eventual accounting recognition. Earnings and cashflow will definitely kick in, just depends on the point of time. Until the management provides guidance to the analyst, I believe sticking to IFRIC 12 would be the safest bet to gauge the impact of the contract. The assumptions I made on the discount rate, IRR, implied cost, financing etc. could be different when company eventually implement the contract but I believe they are not too optimistic or overly conservative.

If you have any alternative views on the above, please feel free to share.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Jay's market diary

Further explosing FundMyHome and how the scheme shortchanges property buyers

Created by Jay | Nov 17, 2018

Why I think someone have insider news on Budget 2019 and P2P lending for homes may not work

Created by Jay | Nov 05, 2018

Why I think capital gains tax could be disastrous for Bursa and the country

Created by Jay | Oct 14, 2018

Discussions

Be the first to like this. Showing 22 of 22 comments

my take is that the development revenue for the build and deployment phase should be recognised by progress for the first 3 years

Since nowadays % of completion method is being paced out how about not by progress but upon completion by the end of the 3rd year?

2016-11-21 21:14

I don't know about % of completion method being phased out. personally I think the method is not perfect but is the closest we have for now to reflect the underlying economic reality. recognising everything at completion doesn't reflect the work done over the years for long term contract and create unnecessary earnings volatility

2016-11-21 23:52

Very informative. I think can be enhanced if consider depreciation of hardware and licensing for software as life circle for both roughly also 3 years. Another consideration is the support cost for the next 12 years. My 2 sen worth as I am not an IT expert.

2016-11-22 01:12

@BLee as the payment amount is guaranteed and not contingent upon usage, the SKIN software would be recognised as a financial asset instead of intangible asset, so there won't be any amortisation. the support cost would be recognised in the 12 year maintenance stage which is not explicitly covered here.

One assumption made here is also that the RM1.5b cost covers all the necessary costs for SKIN development during the first 3 years. A gross margin of 17% assumed here is not overly aggressive, in my opinion

2016-11-22 08:01

Thanks for answering. I do not view SKIN as financial asset as B.O.T. concept carries risk of changing technology and software/hardware update unlike physical assets which can consider 'new' after completion in 3 years time. Just my view..Thanks again.

2016-11-22 09:37

@BLee no problem. here in this article my view is that Prestariang should follow IFRIC 12 for accounting recognition. For BOT contracts with guaranteed payment it is specified that they should be recognised as financial assets under the standard. Essentially I think the rationale of the standard is under BOT, eventual ownership belongs to government, not the company so it's essentially a FA/receivables, not PPE. that's why there is no amortisation. hope this clarifies.

2016-11-22 10:17

Worldwide % of completion method is the exception not the norm and in Malaysia it is being phased out even for normal housing construction due to the build and sell concept.

Moreover for concession agreement where do you see provisions for progress payment during the initial construction and deployment period like in a normal SPA for buying a house?

2016-11-22 10:21

@PurplePain IAS 11 is still using % of completion method for construction. Personally I like % of completion rather than one-off recognition for reasons explained above, but it's up to the standards setter.

For SKIN contract, it is very clear cash payment will only start in the 4th year, no progress payment. What is in this article is on earnings recognition based on IFRIC 12. essentially you are doing work in the first 3 years to be entitled to receive the cash from 4th year onwards. that's why the standards is asking company to recognise revenue and profit in the development stage

2016-11-22 10:34

Profit ought to be recognised at construction stage but only upon completion by the end of 3rd year not based on % of completion method.

Moreover untill completion do you really have the goods/services to sell?

If no how can recognise revenue moreover when there is no provision in the agreement for progress payments??

2016-11-22 10:56

@Jay

You are positive with Ekovest, Triplc and now Prestariang. It seems like you like to invest in companies where the future is secured but details are not so straightforward and very complicated to work out.

Am I correct ? Any comment on WCE ?

2016-11-22 11:49

@PurplePain long term contract is not really equal to direct sales of goods and services. imagine a contract staff, do you pay him at the end of his contract? that would be the most conservative way but doesn't really reflect his services throughout the year

the concession agreement already specify the terms and payment so I don't see why they can't recognise the revenue. if government eventually default or the company fails to fulfill their obligation then that will be a separate event whereby they should recognise a writedown of the financial assets

2016-11-22 12:33

@chonghai I like Ekovest and Triplc because I see them as deep value with short to mid term catalyst. Roughly I can estimate their value, it only depends on timing when the values are realised. Prestariang comparably I'm not so positive yet because all the above are still essentially my assumptions and the PE is still high (although it may be normal for software company).

The details are not so complicated actually, once you know the components inside. Haven't had time to look at WCE, anything interesting? may look at it if I have time

2016-11-22 12:38

At least the first 2 years will not have income from this concession till the completion of the construction and deployment.

2016-11-22 14:52

no cash inflow. whether there will be income I'm afraid it's not up to you and me, there are accounting standards that regulates earnings recognition

2016-11-22 15:28

You are talking accounting standards I am talking financial reporting standards, let's see how it will turn out.

2016-11-22 21:45

more like you are speculating on how the future standards will be while I'm talking on current standards which are effective for now. from conception to effective implementation of a new standards will easily take years, good luck waiting for that

2016-11-23 07:58

Now the next question is, what is the value of prestariang's continuing current business

2016-11-23 17:26

In fact, "progress payments" will start only after completion and commission.

Since there is no provisions for progress billings in the concession agreement for the construction and deployment stage, say, if the construction got stuck by the 2nd year due to unforeseen do you think the goverment your progress billed "receivable" will pay you?

If not how can you recognise revenue during the construction and deployment stage based on progress?

2016-11-24 08:34

http://klse.i3investor.com/blogs/bfm_podcast/111859.jsp

now RHB is also saying that there will be profits recognised in the initial period

2016-12-16 19:42

Jay. I don't think revenue and costs can be recognized for the first 3 years. Service is not considered rendered while a project falls under development stage. All the costs incurred during the development stages would be capitalized and amortization starting to apply when service is provided for receiving payment from the government.

Accounting 101: accruals concept means that revenue and costs are recognised as and when they are incurred, not when cash payment is received or paid. So my interpretation is revenue and costs should be recognised in the first 3 years when work is done, not when payment is received in the next 12 years while maintenance revenue will be recognised in the 12 years maintenance period. In other words, my take is that the development revenue for the build and deployment phase should be recognised by progress for the first 3 years while maintenance revenue will be recognised when maintenance works are carried out.

2016-12-16 21:38

I get where you are coming from. That's what I thought as well before I understood concession contracts accounting. the concept where no revenue and profits are recognised during development stage is the essence of intangible assets where development cost, like what you said, are capitalised and amortised when products/services started to be sold

but if you read IFRIC 12, then you can understand where the accountants are coming from as well. concession contract in essence, is different from usual products/services development.

normal product/services you don't recognise R&D costs because there's no sales transaction happening, so it would be wrong to recognise revenue and profit. there's no customer, you don't know how much revenue can you get from the R&D costss incurred

concession contract on the other hand is a bit like construction contract. just imagine MRT Corp (government) awards a contract to Gamuda (Prestariang) to undertake the construction. in this case, there's already a customer (MRT Corp/government). When Gamuda (Prestariang) starts work, they are not trying to invest and develop something and hopefully make a sale in the future, they are fulfilling a sales already made. They know the contract value (revenue) and minus the costs incurred, they will get their profit.

that' why Gamuda don't wait until full construction is completed only they recognise revenue and profit. the rationale behind IFRIC 12 is almost identical with IAS 11. other examples would be highway concessions or university concessions. revenue and profits are recognised even though the highway/university is still being built

but what if they fail? similarly, if Gamuda has built the MRT line but it collapsed in the 3rd year before full completion, MRT Corp can choose not to pay them or ask for damages, but that's a separate event. Gamuda still did their job in the first 2 years and they didn't reasonably think that it is probable for it to fail, that's why it won't be wrong to recognise revenue and profit in the first 2 years and recognise a rectification cost or an impairment in the 3rd year.

2016-12-20 01:11

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2025-01-09 15:30:00

EMA 5

5 Mins

SELL

2025-01-09 15:10:00

EMA 5

5 Mins

BUY

2025-01-09 14:35:00

EMA 5

5 Mins

SELL

2025-01-09 12:10:00

EMA 5

5 Mins

BUY

2025-01-09 12:00:00

EMA 5

5 Mins

SELL

Apps

Top Articles

1

2

THE INVESTMENT APPROACH OF CALVIN TAN

US 60% TARIFF ON CHINA: CHINA FDI INTO MALAYSIA & INDONESIA WILL BENEFIT THESE STOCKS, Calvin Tan

3

Good Articles to Share

US Fed’s Waller supports further cuts, says inflation moving lower

4

M+ Online Research Articles

JB-SG Special Economic Zone (JSSEZ): 1+1 > 2: Harnessing the Multiplier Effect

5

Mercury Securities Research

6

Good Articles to Share

Explainer: Why does Trump want Greenland and could he get it?

7

Mercury Securities Research

8

Good Articles to Share

Tariff policy done well can help grow the economy, GOP senator says

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Flintstones

Good article

2016-11-21 20:37