Shiba Capital

JHM , D&O. [Educational] Lets understand JHM and difference between JHM and D&O.

Shiba_Capital

Publish date: Sun, 01 Aug 2021, 12:13 PM

Shiba_Capital

0 20

A place to share and provide some updates in the market

**Disclaimer: This is purely for sharing information and educational purposes only.

This post is not intended in instructing/informing any personal to do buy / sell.

Please trade at your own risk or ask for advice from a qualified person.**

**Disclaimer: This is purely for sharing information and educational purposes only.

This post is not intended in instructing/informing any personal to do buy / sell.

Please trade at your own risk or ask for advice from a qualified person.**

**Disclaimer: Everything posted here is for infomational purposes only and do not constitue any investment recommendations.**

JHM - D&O. But are you a different animal and the same beast?

Catchy title? Today we're covering JHM.

JHM is often compared to D&O, but are they actually the same?

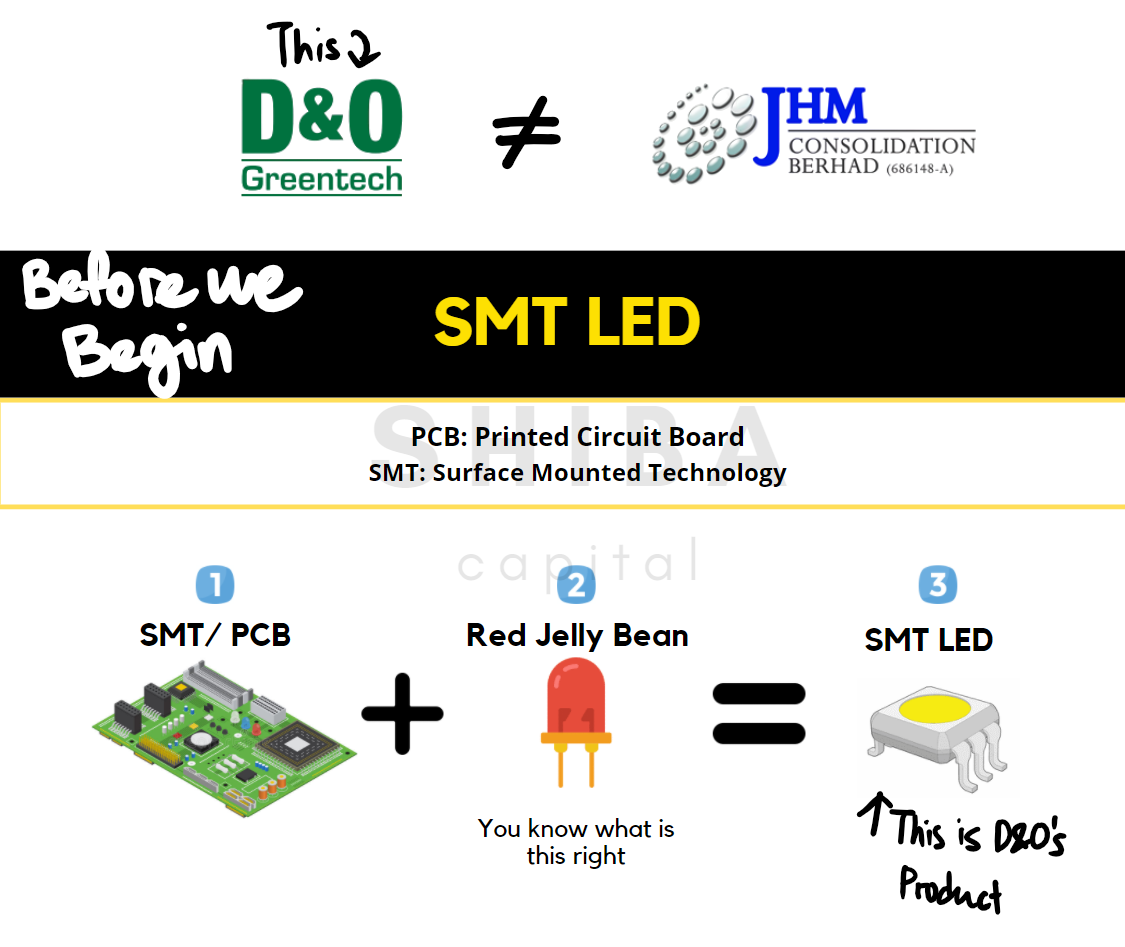

Wait, before we begin, take the jelly bean formula with you. It will be helpful later on.

PCB is the object itself. SMT is the technology used.

SMT LED = surface mounted technology LED or sometimes known as SMD (Surface Mount Device).

Not rocket science here. Next![]()

Business Model Comparison

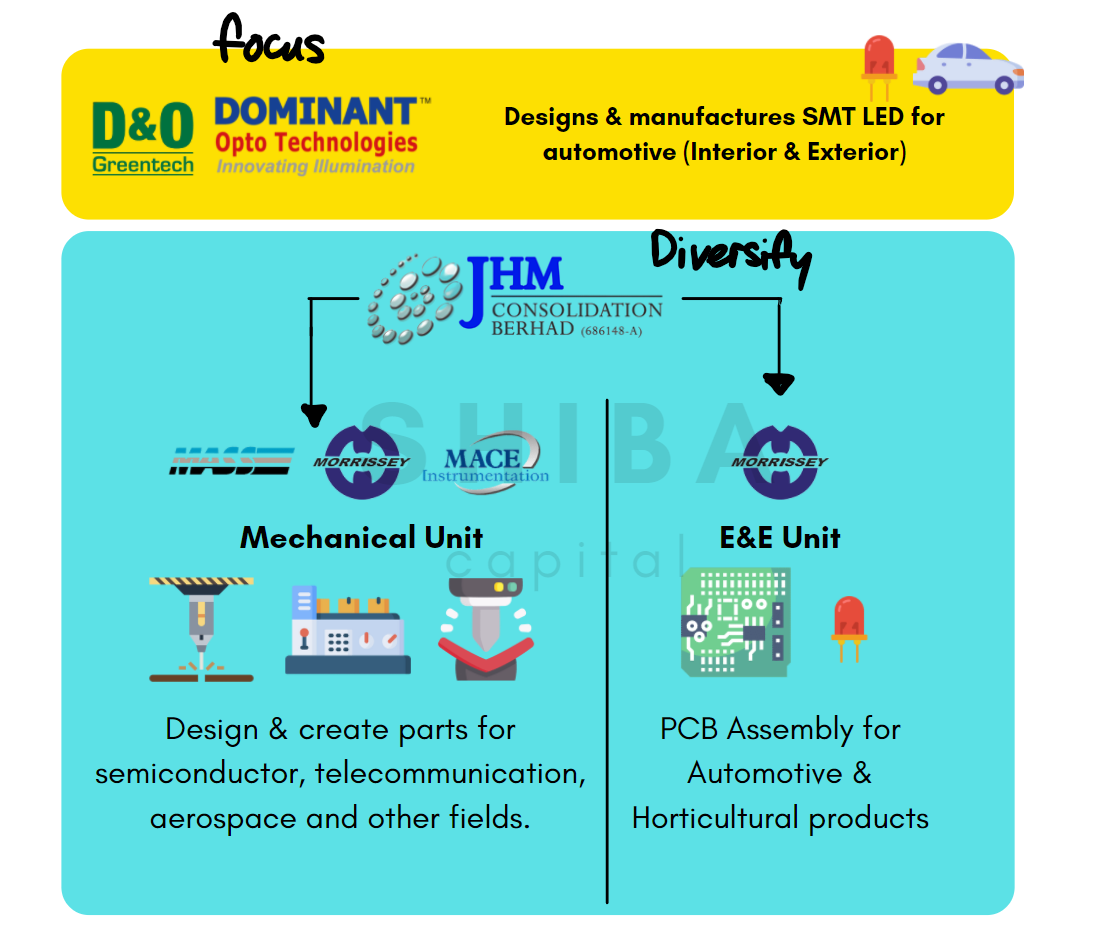

D&O is a pure automotive LED player. JHM is not.

JHM is more of a one stop EMS player for different sectors. Their business is super diversified. The simpler way to understand it:

1. E&E Unit:

They assemble PCBs for automotive LEDs. (PCBA)

2. Mechanical Unit:

Similar to peers like UWC, Wong, Dufu, Notion etc where they make precision parts, stamp metals and some CNC machining based on requests

Automotive segment takes most of their revenue.

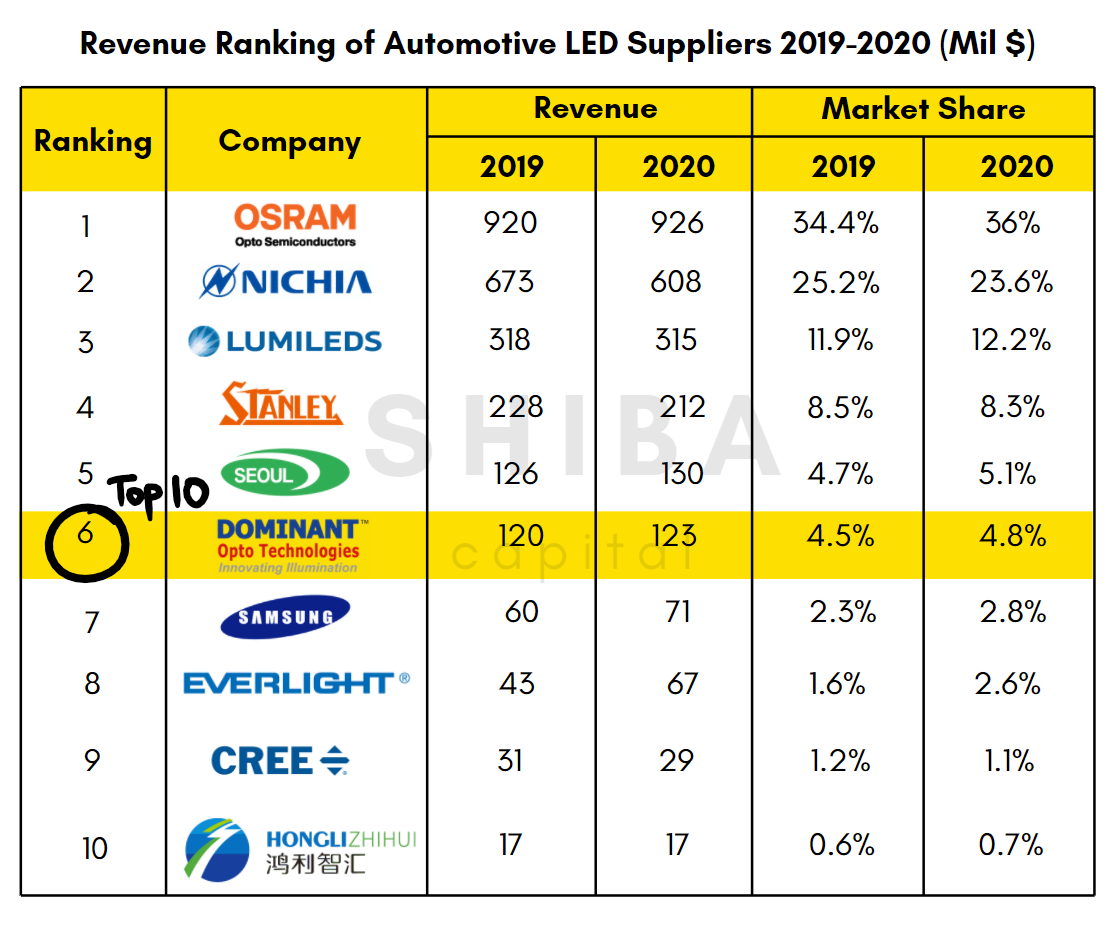

How focused is D&O?

Dominant Opto Technologies, which is under D&O, is actually one of the leading surface mount technology (SMT) light-emitting diodes (LEDs) manufacturers in the world, ranking 6th on the market share.

The products have a wide range of uses but are mainly focused on interior and exterior automotive lighting applications

✴️ Prospects - Automotive & Industrial

✴️ Part 1: Automotive

It's so chaotic that Shiba decided to split it into the automotive vs industrial sector. Be prepared. It's a long 455 read.

We're looking at the automotive prospects now.

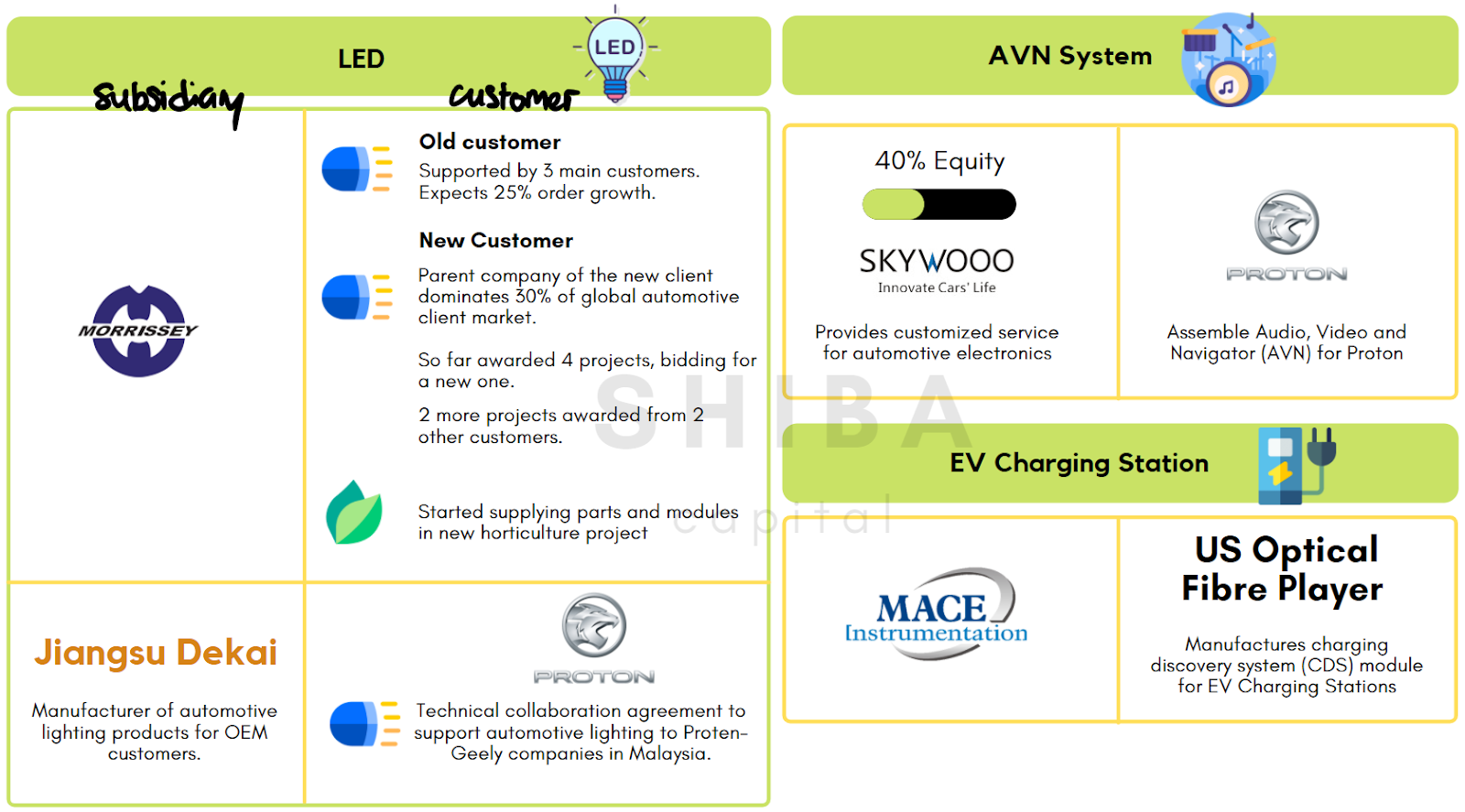

Left is the subsidiary or partners and right is the customer.

1. LED for Cars

Let's start with the LED. Old customers increased their orders and there's a new client who's parent company dominates 30% of the global automotive client market. Going back to the table earlier, it might be OSRAM. (Assuming its the right category)

Projects awarded by 2 other customers are worth US 1.8mil and US 1-1.5mil.

They are currently building samples for submission to the new customer. Some will begin production this year and some next year. JHM is currently bidding for another project worth about RM 21 mil a year.

Skywooo & Jiangsu Dekai are recent JVs and both are suppliers to Proton Geely.

Skywooo's target revenue stream is RM 20mil/ year which is not much but they provide extra business opportunities in the future. As for Dekai, JHM will supply automotive lighting to Proton-Geely companies.

2. LED for Horticulture

Horticulture is like using LEDs to produce artificial sunlight for plants. The Group collabed with the Singapore government which contributes a lil bit, but it might grow in the future.

3. EV Charging Station

EV charging module actually comes from the 5G customer (Next slide) and JHM is expanding its existing plant by 150% for this, which will be completed around this month.

✴️Part 2 : Industrial

Now the technology part and other industrial parts.

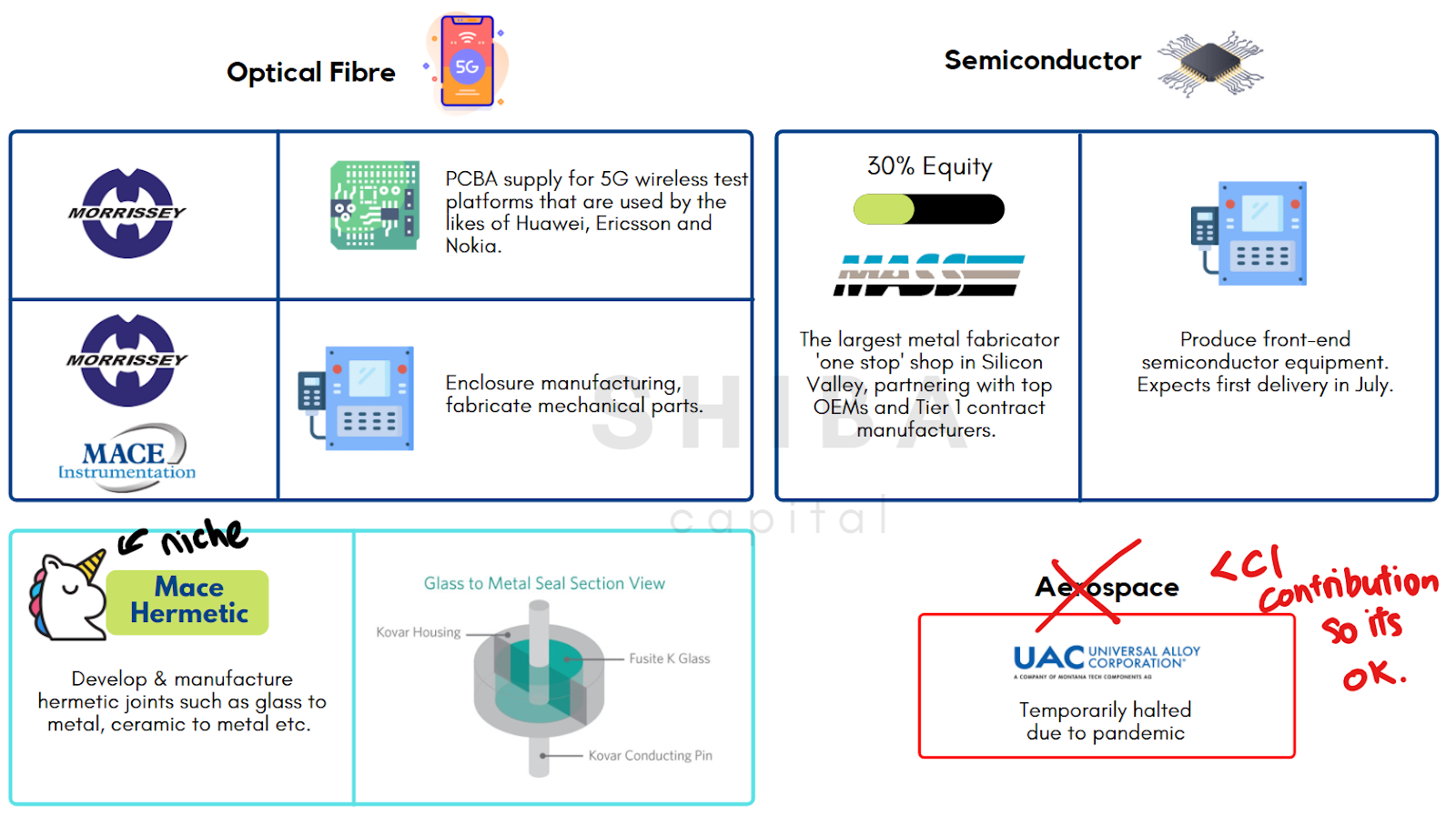

1. Optical Fibre (This customer)

JHM is expanding twice for the same US Optical Fibre customer. The other one is a 9 acre land in Batu Kawan Industrial Park (Penang). That's for the telecom equipment industry.

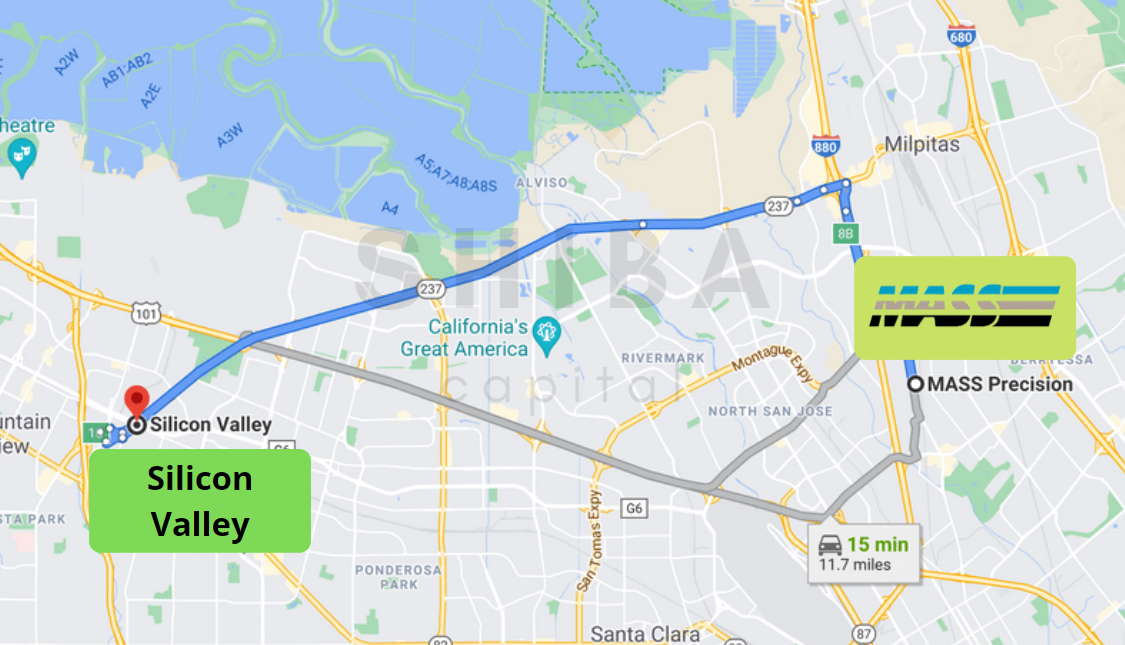

2. Semiconductor

Not much spotlight on the MASS Precision. But this company is actually only 15 minutes away from the Silicon Valley US and is one of the largest metal fabricators 'one stop shops' there. JHM is tasked to produce front-end semiconductor equipment and is expected to see its first delivery in July.

3. Hermetic Joints

As for MACE Hermetic, JHM is quite ambitious. It's a niche field (high margin) that joins glass/ ceramics to metals, used in environments that are sensitive to noise and in autonomous vehicles, aerospace cockpits and military components. The production was delayed to Nov/Dec.

4. Aerospace

This segment was originally quite exciting. The initial project has low margin but opens up opportunities for niche and high profit projects.

On 25 March 2021, the MOU expired with UACE due to the impact of COVID to the aerospace industry. This might still be a potential play in the future when covid subsides.

✴️ EV Battery & Profit Guarantee

As for the EV battery, it's not going to happen anytime soon. JHM is planning to gain more exposure in EV through assembly of battery packs.

According to the news, a recent partnership with China's Geely Proton could open up the door to such ventures. Geely has few EV models that they might introduce in Malaysia maybe by the end of 2022.

For the next QR coming out. There's a profit guarantee of RM3.4mil. This is because when JHM entered into a share sales agreement (SSA) to acquire Mace Instrumentation (MISB), the promised aggregated PAT should be RM 21mil as compared to RM 17.5mil.

Thus, JHM had on 28 May requested the vendors to pay the amount within 14 business days which will be reflected in Q2.

Come join our telegram at : https://t.me/shibacapital

Come join our facebook at: Shiba Capital

That's all! Thanks for reading

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Shiba Capital

The Big Energy Crunch - Coal, Oil & Gas (Feat- $ARMADA, $HIBISCS, $YINSON, $DIALOG)

Created by Shiba_Capital | Oct 06, 2021

Quick recap of what happened this week! *Full of Volatility and excitements*

Created by Shiba_Capital | Sep 26, 2021

What happened to Evergrande and its impacts to the steel industry

Created by Shiba_Capital | Sep 20, 2021

Weekly Recap - $SCIENTEX, $JAKS, $KGB, $GREATEC, $QES, $TOPGLOV & 5G

Created by Shiba_Capital | Sep 19, 2021

Macro-roni of the week- Commodities (Alum & LNG), Semiconductor index SOXX

Created by Shiba_Capital | Sep 15, 2021

Discussions

5 people like this. Showing 9 of 9 comments

Your post is good but you need to highlight the value difference...

One is odm (D&O). one is oem (JHM). Cannot compare. D&O is a component owner, JHM is just a contract manufacturer.

One is a Nike, another is Magnitech.

One deserve much higher valuation as compared to the other.

2021-08-02 00:43

It is true. JHM will gain more and more exposure and traction, and it will eventually be the best investment for the tech super bull rally.

2021-08-03 14:09

jhm ni terbaik kikiki. banyak mau observe dulu, ok... dont miss rocket ya. hehehhe

2021-08-04 07:35

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

.png)

Apps

Top Articles

1

Koon Yew Yin's Blog

3

Koon Yew Yin's Blog

4

6

7

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Mimimomochi

very good sharing. Dint know that JHM had so much involvement not only in the LED business.

2021-08-01 13:08