We maintain our OVERWEIGHT call on the rubber products sector on the back of a favourable structural and macroeconomic environment. We believe earnings will be capacity driven while operating efficiency will be required to outperform peers. As such we like Hartalega and Kossan for their economies of scale, leadership in the nitrile glove segment and accelerated capex cycle.

Resilient demand. Global glove consumption is expected to remain strong, led by demand from the healthcare segment, and is anticipated to expand 8-10% per annum. Demand is often touted as inelastic due to the crucial protective role that gloves provide, especially for the healthcare sector. Thus, glove suppliers have a resilient earnings profile combining defensive qualities with steady earnings growth.

Additional capacity. We believe that the additional capacity from the expansion in nitrile production will be absorbed by the market. The commissioning of new production lines is being done progressively, which will enable the glove makers to time upcoming capacity to the prevailing demand landscape.

USD strength is a boon. The strength in USD/MYR will benefit the industry because revenue will have a greater sensitivity to the greenbackrelative to costs. A 3% increase in the USD/MYR exchange rate could liftthe industry’s earnings by ~2-4%.

Karex (KAREX MK). We maintain our BUY recommendation on the stock as we continue to like its organic and inorganic growth potential. We have a higher TP of MYR3.89 (from MYR3.43), ie 20x FY16F P/E and a 14.4% upside, on the back of an expected 3-year FY14-17F EPS CAGR of 23.8%.

Risks. Heightened competition among glove players could lead to lower ASPs and margins that, in particular, would not bode well for Top Glove(TOPG MK, BUY, TP: MYR5.06) and Supermax (SUCB MK, BUY, TP: MYR1.87) as both are margin laggards in the industry.

Maintain OVERWEIGHT. We continue to like stocks in the rubber products sector that have good earnings growth, strong balance sheets and decent dividend yields. Our Top Picks are Hartalega (HART MK, TP: MYR8.04), Kossan Ruber Industries (Kossan) (KRI MK, TP: MYR5.12)and Karex. Maintain OVERWEIGHT.

Demand – Supply Structure

Demand Structure. Global glove consumption is expected to remain resilient – led by demand from the healthcare segment – and the street anticipates this to expand 8-10% annually over the next few years. This demand will be supported by organic growth from the developed glove markets such as the US and EU, as well as the rising healthcare spending levels in the emerging markets. Glove demands are often touted as inelastic due to the crucial protective role that gloves provide, especially for the healthcare sector. This has been further reinforced by progressively stringent health regulations imposed by countries. Thus, glove suppliers have a resilient earnings profile that makes them suitable for a defensive theme play.

Overall increase in healthcare awareness and hygiene standards will continue to encourage glove consumption, especially in the emerging markets. Per capita consumption of gloves in the Asia and China markets is trailing, representing only 2.8% of the per capita consumption in the US (see Figure 2). Assuming that the glove usage in Asia and China reaches levels utilised in the EU, both Asia and China markets could potentially be as large as 470bn pieces. This is more than 2.5x the current global glove market.

Unpleasant catalyst. The recent Ebola virus outbreak in West Africa may create an unpleasant catalyst in glove demand. The latest official update on 26 Dec reported 19,000 cases of Ebola infection in Africa with 7,600 deaths. Nevertheless, our channel checks with sources indicate that they have not seen any surge in orders yet, though queries were increasing. Nonetheless, in the longer term, we thi nk that the epidemic will help to improve healthcare awareness, which, in turn, will contribute to resilient glove demand

Additional capacity. Amidst the robust growth in rubber glove consumption, the industry is also experiencing a shift in user preferenc e from latex gloves towards nitrile ones. This shift is due to the increasing rate of latex allergy among medical professionals. Major developed markets had experienced negative to minimal growth for the latex gloves segment while recording large positive growth for the nitrile equivalent in the last few years (see Figure 3). This shift is also reflected in Malaysian rubber gloves exports, which constitutes roughly 60% of the global glove market. Since 2008, nitrile gloves – as a percentage of Malaysian gloves exports – have seen their proportion increase to 50.2% in 2013 from 17.3% in 2008 (see Figure 4).

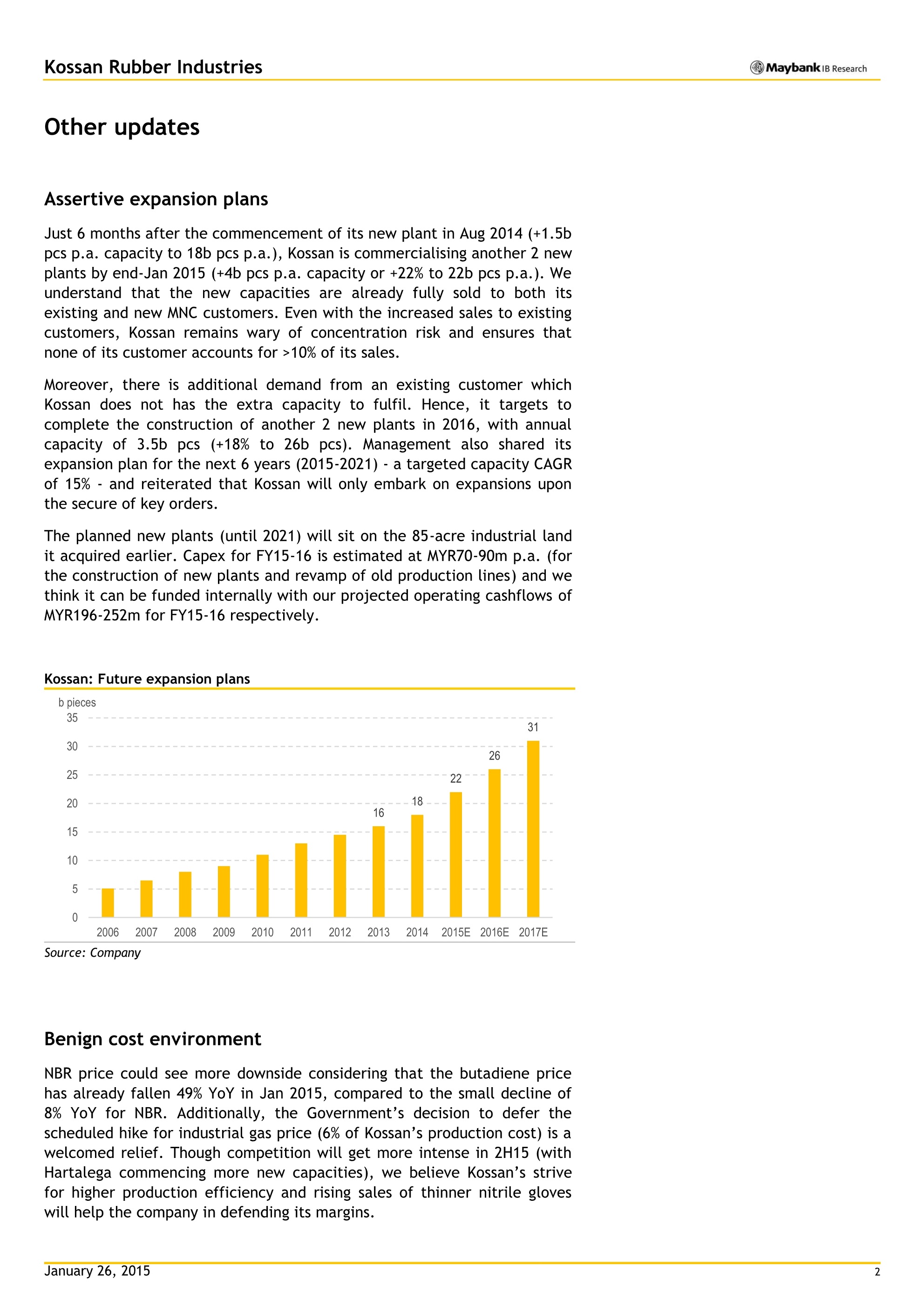

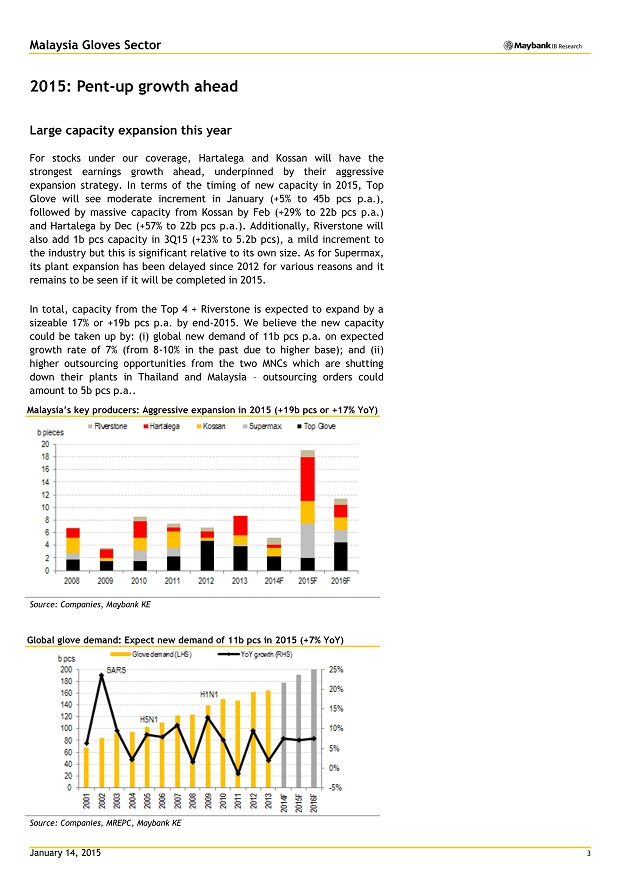

Major Malaysian glove suppliers have been aggressively expanding their nitrile production in light of this shift in user preference. We forecast a 19bn pieces capacity expansion in 2015, ie a 21% growth from 2014 numbers.

This expansion has sparked fears of a supply glut. Nevertheless, we believe that the additional capacity from the expansion in nitrile production will be absorbed as the commissioning of new production lines is being done progressively. This, in turn, will enable the glove makers to time upcoming capacity to the prevailing demand landscape.

Given the competitive operational environment, major Malaysian glove suppliers have thus far managed their respective expansion plans well to prevent an oversupply in the market. As such, we expect much of the same strategy from them going forward. We believe that the glove suppliers will be proactive with regards to their upcoming capacity should demand be softer. Furthermore, we believe that the advocates of an oversupply scenario have not fully discounted risks of possible capacity delays or unscheduled interruptions to existing capacity such as those that plagued Supermax in the last four years.

Halyard Health Inc, formerly known as the healthcare division of Kimberly-Clark Corp (KMB US, NR), has announced plans to shut down one of its glove manufacturing plants in Thailand that has 3bn pieces annual capacity by 2H15. This ought to help ease some of the additional capacity worries.

Margin Analysis

Competitive pressure on margins. While we do not expect a supply glut, we do forecast for competition between glove suppliers to heat up with the expected additional capacity. As with 2014, the increased competition will lead to lower ASPs as well as erosions in margins. Should heightened competition for sales volume lead to a price war, we believe that Hartalega – the industry leader in margins – will be poised to benefit the most. As such, we believe that improving efficiency will be the key to outperforming peers.

Cost pressure. Nonetheless, unlike 2014 where the margins of rubber glove industry were beset by tariff hikes in electricity (+15%) and natural gas (+21%), we do not foresee significant cost headwinds for glove suppliers in 2015. Prices of raw materials are forecasted to remain subdued. The weaker demand and stronger supply situation in the rubber market is expected to persist, thus keeping prices of natural latex low. Meanwhile, the current oil price weakness, from which nitrile is derived, is expected to keep prices of the latter favourable as well.

The introduction of goods and services tax (GST) will have minimal impact on the rubber glove industry, as a significant amount of production is exported, thus it is a zero-rated output tax.

Strength of USD/MYR is a boon. Expectations of interest rate normalisation in the US as well as a weaker Malaysian fiscal position, led by the fall in oil prices, have caused the MYR to weaken against the USD. As at 26 Dec, the USD/MYR exchange rate has appreciated 10.6% since 1 Sep 2014. The strength in USD/MYR will benefit the rubber glove industry because: i) the rubber glove industry is predominantly export oriented – we predict 85-95% of total production is earmarked for export and quoted in USD, and ii) the cost structure of these producers is largely denominated in MYR.

Further, the MYR has weakened against major competing rubber gloves producing nations such as Indonesia and Thailand. This ought to help boost competitiveness of Malaysian rubber products vs those of Indonesia and Thailand.

Our sensitivity analysis indicates that, should the USD/MYR exchange rate strengthen by 0.10, Malaysian rubber gloves producers could benefit from an increased earnings level of around 2-4%.

Source: RHB