Target Invest - We Target, We Invest

THE LAST RIDING BET ON HENGYUAN REFINERY

For latest information, can join us at

Blog https://targetinvest88.blogspot.com

Telegram https://t.me/targetinvest88

Global energy prices are very volatile with Ukraine Russia war. The under investment on the oil and gas industry had also saw production not able to catch up with the demand as global economy reopen post pandemic.

The tension of the war had sparked strong rallies on the oil prices as well as oil refinery crack margin. Both saw strong rallies in prices back in the 1st and 2nd quarter of 2022.However, as of the last quarter earning report in May, Hengyuan apparently appear not to be able to capture the windfall in crack margin prices.

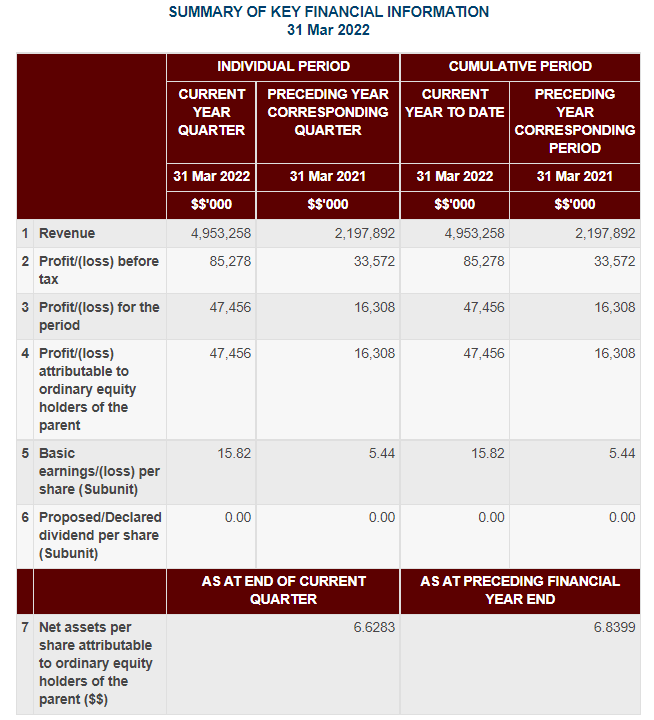

With almost RM 5 billion in revenue, Hengyuan only manage to get a profit of 47 million, turning into 15.82 in EPS. As many investor are expecting a big improvement in the result, the result being not up to the expectation lead to a major sell down of the stock from RM 7 to RM 4.A big chunk of gross profit being RM 508 million are knock down with big operation losses of RM 338.5 million.

Many predicted that the losses could be due to bad hedging, selling contract that are too low while crack prices go way above. While this argument can be a valid point, it can also be a important turning point moving forward.

Assuming that HENGYUAN spread out their monthly hedging by selling contract are a certain price range, for example is USD 20.

If the price continue to go up until USD 30, every contract stand to lose out USD 10. (That is losing money)

If the price go down to USD 10, every contract stand to profit USD 10 as they sold at USD 20.

MY ANALYSIS (All numbers are my own assumption for easy understanding)

One of the reason for the major operational losses or hedging losses could be due to HENGYUAN do a forward hedge of 1, 2, 3, 4, 5, 6 month probably around the price of USD 25, 22, 20, 18, 15, 12 respectively (price are example)

When the crack margin prices continue to go up, all the hedging done in the forward month will be in a losing position. However, as long as HENGYUAN DO NOT CLOSE THE CONTRACT POSITION until the contract end settlement, then there is still chance for it to make a profit.

I will give you an example.

During the month of MAY 2022, lets say HENGYUAN sell 100 contract at USD 20 for the month of AUGUST. The crack margin continue to go up until USD 35. On paper, that is a paper lose of USD 15 for every 1 contract, and accounting practice will need to recognize the "paper losses" into operation losses as the contract will result in such losses at that material time.

However, if HENGYUAN held on the contract and coming to AUGUST 2022, the crack margin now is USD 10. If HENGYUAN DID NOT close all the sell contract in the month of AUGUST, then HENGYUAN will be looking for a paper profit of USD 10 per contract now.

CONCLUSION

So, do you think HENGYUAN still have the last ride on this oil refinery saga? Do they have the golden hand where contract sold at high are still holding on to their hands until delivery?

I am not related and do not have any insider information in HENGYUAN operation. I am only a investor in HENGYUAN and still holding in HENGYUAN share as waiting for them to unveil the secret.

If you think HENGYUAN hedge master is very good and still hold a golden hand, the coming quarter report will be very powerful as it will reverse all the operation losses and turn into profit. But if the hedge master is so bad and got played up side down by the global oil syndicate, that is too bad for HENGYUAN.

For latest information, can join us at

Blog https://targetinvest88.blogspot.com

Telegram https://t.me/targetinvest88

More articles on Target Invest - We Target, We Invest

LCTITAN - A POTENTIAL MISSING PIECE OF JIGSAW PUZZLE FOR PETRONAS ?

Created by targetinvest | Aug 12, 2024

HOW LCTITAN CAN BE ROPING INTO THE GREEN HYDROGEN ECOSYSTEM WITH TOLUENE?

Created by targetinvest | May 20, 2024

IS CENSOF WORTH YOUR HOLDING FOR THE NEXT 3 YEARS? READ THIS BEFORE DECIDING

Created by targetinvest | May 17, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

{kind=link}

Top Articles

1

Mercury Securities Research

2

3

4

THE INVESTMENT APPROACH OF CALVIN TAN

5

Koon Yew Yin's Blog

6

THE INVESTMENT APPROACH OF CALVIN TAN

7

M+ Online Research Articles

8

TA Sector Research

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....