TECGUAN - Dividen? No Dividend?

TECGUAN - Dividen? No Dividend?

Such an exciting week for TECGUAN's holder isn't? Consolidating at price at RM2.10 and rising to almost RM 2.70 now.

Many might think, what would be the target price for this share as it does not pay dividend from the past record.

Personally, I really do like the article "Another Limit Up Share - Tecguan" written by Jokerforever21. He has performed a very extensive research covering the financial status and quality of the Company.

As such, in this article I will go into detail for the financial status and quality of the company, but would like to highlight 2 main factor that would drive TECGUAN earnings for the whole year.

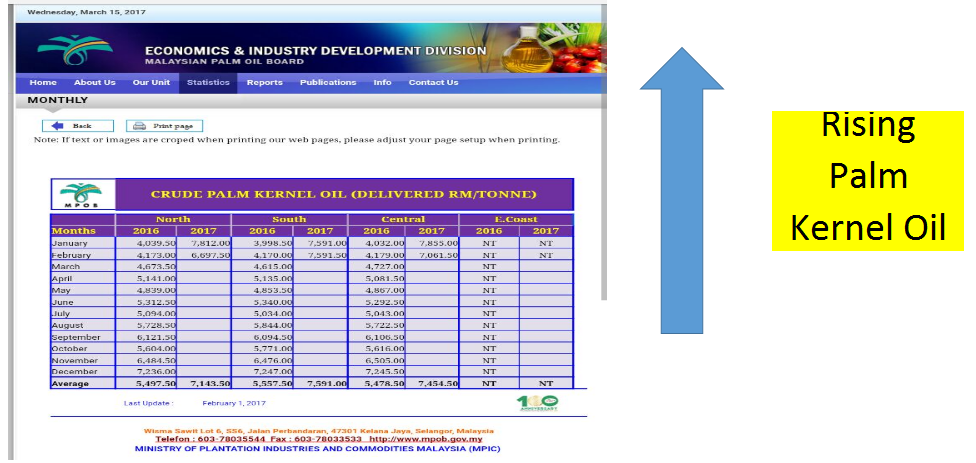

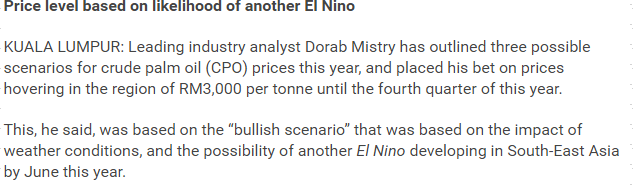

1st would be CPO price

CPO price remain resilent throughout the year. We could be seeing a real good year for CPO related industry as seen in article below.

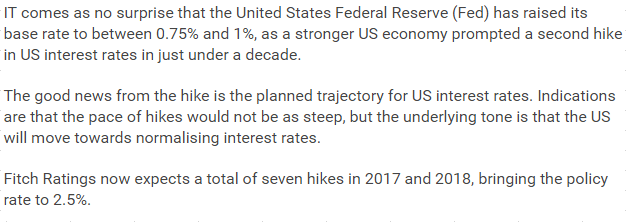

2nd USD:MYR

As United State have just increase interest rate last week and more interest hike are expected as stated in article below:

With this 2 factor, I believe TECGUAN would have a strong quarterly earnings ahead and for the year 2017.

DIVIDEND? NO DIVIDEND?

One good example would be TASEK cement, family owned business, paying high dividend every quarter.

With the strong earnings ahead, I believe DIVIDEND will be just a matter of time.

With strong earnings ahead seen in TECGUAN, there could be many surprises underlying.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Discussions

Be the first to like this. Showing 7 of 7 comments

lordng94

Why we expected better result for Tecguan on coming quarter?

1. USD has strengthen 5 % from November 2016, RM 4.2 to RM 4.45. According to Tecguan foreign exchange risk analysis, for every 5% strengthening of USD will contribute additional 5.36 mils to its profit. Wow!!

Please take note that 93% of sales of Tecguan are denominated in foreign exchange and 71% of costs are denominated in RM.

As such, we foresee Tecguan will benefits from weakening of Ringgit during this QR.

2. Average price of CPO has increased from RM2800 to RM 3100 (Peak on January),

increase of 10% in price again is another exciting factor that leads the surging of price for past two days.

3. Management team didn't disclosed much information of their company operation is drawback for Tecguan. However, based on almost all of the their plantation areas are located at Tawau, Sabah which make us have chance to use Cepatwawasan's Quarter Report as the guideline to evaluate Tecguan.

As you can observe for past three years, their profit line charts are in tandem.

Which further make me strongly convinced that Tecguan will delivers stronger result for coming quarter reports.

(Cepatwawasan lastest QR was from Oct to Dec 2016, CPO and USD were not at Peak. As such, Tecguan quarter result which is covered from Nov to Jan 2017 will has better profit than Cepatwawasan)

(No idea on how to upload my chart analysis here, someone please enlighten me).

4. All Tecguan export is to Tecguan (China) which is believe is the major turnaround factor for Tecguan.

Their have pare down the sales to Golden Calf Ltd for past two years and had stop the sales to Golden Calf Ltd during year of 2016.

Tecguan has shifted the full focus to China market which I believe China market has better profit margin which leads to Tecguan consistently make profit for recent quarters.

Not here to promote Tecguan and will not put any TP, but is just to share my opinion on undervalued Tecguan which many people will overlook. It is just valued at PE of 8 with their average 13 to 14 years old palm oil tree, which means Tecguan still have at least another 3 years of Prime Peak Yields to harvest!!

13/03/2017 10:13

2017-03-21 13:37

Kwantas, another palm oil company located in Sabah has delivered a strong performance for 4th quater FY2016. Turnover surged by around 50% compared to 4th quarter 2015. This has assured the profit margin, volume and yield of palm oil and related crushing activities still well maintained at decent level. However, due to weakening of Ringgit had caused Kwanstas faced the unrealized foreign exchange loss of RM 14.7 million from the USD denominated borrowings and receivables + loss of derivative financial instruments of RM 5.4 million. If we excluded USD strengthening factors, Kwantas latest quarter profit margin is actually surged to RM 42.6 million or EPS of 13.6 cents, almost 10 folds of increment compared to 4th Q FY2015.

Again, all the plantation peers operating in Sabah have delivered the strong quarter results, Tecguan should performed in same direction or even stronger than its peers because of 93% of sales of Tecguan are denominated in foreign exchange (USD) and 71% of costs are denominated in RM.

According to Tecguan foreign exchange risk analysis, for every 5% strengthening of USD will contribute additional 5.36 mils to its profit. Tecguan is only few plantation company which is benefited from weakening of Rinngit, unlike Kwantas and IOI.

2017-03-21 14:12

Again, not here to ask you to buy tecguan here. Is just the sharing of my study and analysis based on all the Sabah plantation companies. You need to do your own study before you buy in the counter.

2017-03-21 14:21

http://www.mpoc.org.my/monthly_sub_page.aspx?id=7220ebe4-64f4-4d1c-91c3-2053ef0de02b

See at export to China during January had increased 60% during January, to cope the CNY demand and replenish the stocks.

2017-03-21 14:30

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2025-01-03 12:05:00

EMA 5

5 Mins

BUY

2025-01-03 12:05:00

ADX

5 Mins

BUY

2025-01-03 12:05:00

MACD/RSI

5 Mins

BUY

2025-01-03 12:05:00

TURTLE SYSTEM 20

5 Mins

BUY

2025-01-03 12:05:00

TURTLE SYSTEM 55

5 Mins

BUY

Apps

Top Articles

1

2

CEO Morning Brief

3

CEO Morning Brief

4

Good Articles to Share

‘THINGS ARE GETTING WORSE’: Credit card debt skyrocketing to concerning levels #shorts

5

Mercury Securities Research

6

Good Articles to Share

Nvidia's Blackwell could propel 2025 revenue to $200B: Strategist

7

Good Articles to Share

Stock market today: Dow, S&P 500, Nasdaq fall as comeback bid falters and Tesla, Apple slide

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

newbird33

Got to sell b4 June

2017-03-21 12:39