Intelligent Investing

What's the correct multiple - Growth Rate, ROIC & Multiple

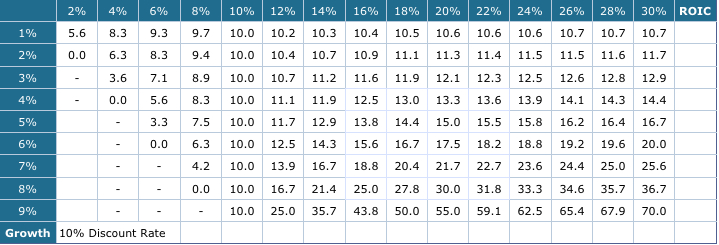

This is a simple table that shows the 'appropriate' multiples i.e P/E or EV/EBIT given a level of constant growth rate & return on invested capital (ROIC) using a 10% cost of capital or discount rate.

Horizontal is the ROIC rate whereas growth rate is on vertical. Please do not use this for valuation because it assumes a constant ROIC and growth over a very long ( > 20 years ) time frame. But it does provide a few important thing.

- Contrary to popular belief, if ROIC = Discount Rate, in this case at 10%, growth does not matter because the business fails to create any value. Therefore all growth rate deserve 10x.

- When ROIC is less than discount rate, growth destroys value. The higher the growth the faster it is that value is destroyed, hence multiple gets lower as growth turns faster. Understand this will help you avoid value trap.

- Another popular myth is that only companies showing really high growth deserve a high multiple. Companies with high ROIC can just as easily command a high multiples without strong growth. Public Bank is a perfect example that the stock consistently trade around P/E 17-20 at a 5-7% growth rate.

- Always look at return before growth. Growth itself doesn’t tell you anything. The best of the best are companies that can grow really fast and generate a high return at the same time, but those are rare breed. The next best ones are those that can maintain high return over a long long time.

If you find this helpful, please share it and subscribe to our list http://eepurl.com/b93qbH

More articles on Intelligent Investing

Discussions

Be the first to like this. Showing 8 of 8 comments

and also...isn't higher the ROIC...its more prone to erosion (deterioration in ROIC) due to competitions in the future? Reversion to the Mean...around 10% ROIC matching the COC?

Figuring out the MOAT is not that easy...

and perhaps...its even more safer betting on the mean reverted companies having ROIC at 10%?

2016-11-19 15:20

How you get discount rate? Based on management estimation on the industry? That is subjective figure applied on accounting figure then..

2016-11-19 18:45

It is not that straight forward but more of something that improve thinking. High ROIC is prone to erosion or reversion to mean when there's no moat to protect it. Didn't quite get the safer bet part?

Cheoky yes it is very subjective, 8-12% is a safe range, one of the weakness of DCF.

2016-11-19 20:01

Posted by Ricky Yeo > Nov 19, 2016 08:01 PM | Report Abuse

It is not that straight forward but more of something that improve thinking.

Ans: agree. the great thing about high ROIC business is that u need to fork out a small fraction of the Earnings as Reinvestments for the same growth.

High ROIC is prone to erosion or reversion to mean when there's no moat to protect it. Didn't quite get the safer bet part?

Ans: when a business or specifically the 'IC' has a high return 'EBIT', i.e high ROIC (without much MOAT)...it will attract many others (competitors) to follow the same path and go for such investments and sell their products at a reduced margin...as the payback is still attractive unlike an already low ROIC business.

So the Margin will thin out much quickly.....the 20 years forecast assumption on the ROIC wont be valid - the impact on its RONIC and thus the growth = RR.RONIC may be much significant causing the above EV/EBIT multiple to shift significantly away from the derivation presented on above table.

2016-11-19 21:03

say you have done some studies and estimates company A with ROIC of 30% with growth of 5% and company B with ROIC of 12% and growth of 8%.

From the above table, you will give both an EV/EBIT of ~ 16.7 right?

Now...what i am saying is you may have some bias toward company A and tempted to give an even higher valuation considering that you had given it a lower g = 5% only compared to B...by being 'fair'.

But...who knows...it may be riskier to go for Company A than B as the chances of the ROIC of company A dropping from 30% to 12% within the early stages in the time frame of valuation may be higher (causing the multiple to approach 11.7 - from table) compared to the growth rate of company B dropping from 8% to 5% (approaching the same multiple 11.7 from table)....

I am comparing the possibility of ROIC erosion in company A with the loss of potential for Reinvestment in company B..

If you ask me frankly i am still in favor of company A...but we should not forget about the above possibilities..

2016-11-19 21:33

this table is not ideal for most companies because it assume things never changed. But companies with strong moat does have the ability to maintain their ROIC for 10-30 years or even longer without being eroded. While some might have 5 years, some 1 years, rest none.

Or if you can find one that is building their moat, you get an even longer runway.

2016-11-21 06:44

Post a Comment

Featured Posts

Apps

Top Articles

1

Kenanga Research & Investment

2

3

BFM Podcast

4

5

BFM Podcast

6

BFM Podcast

7

RHB Investment Research Reports

8

PublicInvest Research

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

probability

thanks for sharing Ricky...good overview.

Somehow i still think we are getting biased (a little) based on the absolute value of the ROIC or the Growth itself....it still comes back to EV/EBIT should be (given above for each scenario) relative to what market is giving currently.

I think the table just says...IF the ROIC or the Growth is as such X & Y...your valuation relative to current EBIT is Z...that is all it is saying.

How about ROIC below cost of capital...with a negative growth? i.e they sell of the Invested Capital in stages...?

Perhaps the certainty for reliable growth on a lower ROIC is higher...example Plantations...

it appears not so straight forward to 'see the bargain' one gets from the market though one can have a reliable information on the ROIC of the company.

2016-11-19 14:58