KLSE Technical Analysis

AZRB: I expecting it to fly high !!!

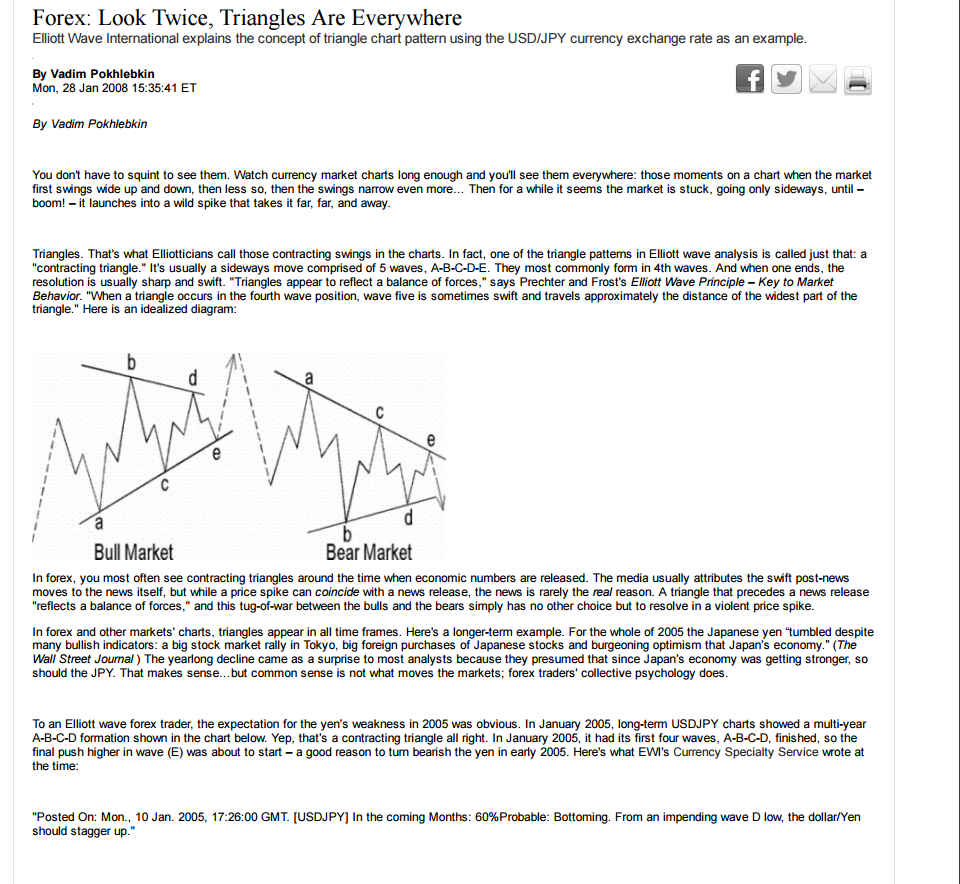

I bought in at $0.715-0.730, reason is it formed contracting Trinagle consolidation and it was ended with wave e, Likely impluse wave kicking in, I am anticipating it will break 0.750 and heading to test next resistance at 0.775/0.800, med term target I aming is et 0.870/0.900/1.00. My Stop loss it below $0.690.

What is Contracting Triangle ? refer to the article below

http://www2.elliottwave.com/freeupdates/archives/printer/2008/01/28/Forex-Look-Twice,-Triangles-Are-Everywhere-.aspx

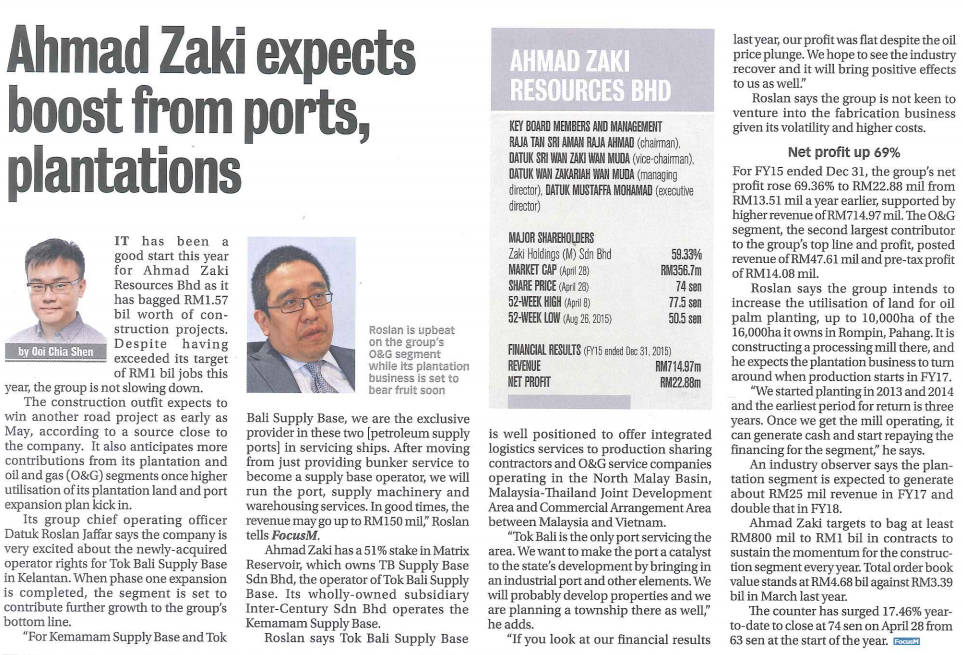

I do see an good FA article from Focus Malaysia write up.

FA Analysis do by the blogger .. you may refer below

Background (source from klseinvestor)

Ahmad Zaki Resources Berhad (AZRB) is a Malaysia-based company engaged in investment holding, providing management services and as contractors of civil and structural construction works. AZRB operates in four segments: construction, which is engaged in civil and structural construction works; trading in oil and gas and other related services, which include dealing in marine fuels, lubricants and petroleum-based products; cultivation, which is engaged in oil palm, and other operations, which is engaged in property development, investment holding, provision of management services and dormant companies. During the year ended December 31, 2009, AZRB's projects include Design and Built Complex Kerja Raya 2, Federal Road 3 Pekan to Kuantan, University Darul Iman Building Works, Maternity Hospital Terengganu, Rectification Works at Dataran Putra Precint 1and others. In August 2011, the Company sold 21.57% interest in Eastern Pacific Industrial Corporation Berhad.

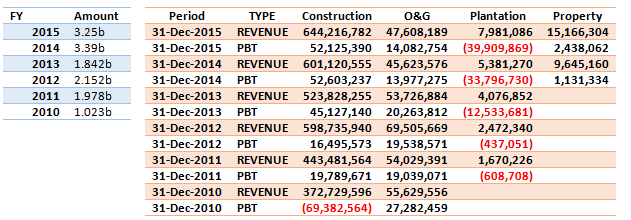

FINANCIAL PERFORMANCE AS OF 31st DEC 2015

For the year ended 2015, AZRB’s profit for the year nearly doubled to RM21.5m from previous year made possible by the substantially improved other operating income AZRB despite incurring RM46.7m interest expenses (more than 2x of previous FY.

In terms of balance sheet, AZRB assets had grew to RM1.7b from RM1.5b primarily from larger trade receivables (current) and additional capex + acquisitions. While its networth stood at RM338.7m

In the last 2 years AZRB had grown its order book substantially and its current order book able to sustain AZRB income for the next 3 – 4 years.

Construction, and O&G segment continued to generate profitability supplemented by property sector, while its plantation operations continued to incur substantial losses.

At current price level at RM 0.725 per share, AZRB is trading at nearly 16x P/E and its NTA stood at RM0.69 per share and more or less reflects AZRB’s current financial position. Base on current earnings level, NTA is expected to grow at 0.62 sen per quarter or 2.48sen per annum.

However it is AZRB future prospect that is more exciting, its profitability is expected to improve by leap and bound beyond FY2017, likely by end of FY2020 its net profit would be in excess of RM100m per annum. It is likely by end of FY2020 40% – 50% of its profits before tax would be from operations that generates recurring income.

Here are the facts that substantiate the above statement.

PROSPECTS

CONSTRUCTION SEGMENT

· AZRB is extremely connected and is likely to be able to secure construction jobs at regular basis to maintain healthy order book hence construction segment will at least maintain current profitability.

· Awarded part of MRT SSP line (4.5KM) worth RM1.44b that is expected to start in 2H 2016 and expected to be completed by 2022, estimated that translates to RM221.5m revenue per annum till 2022, expected to increase its construction segment revenue by at least RM110m in FY2016 to excess of RM800m.

PLANTATION SEGMENT

· (Palm oil) Plantation planting activities started in FY2013 and had planted 5,500 hectare by end of 2014. Planned to plant additional 5,000 hectares in 2015 and 2016. The first 5,500 hectares are expected to produce fruit bunches at 30 months age till 25 – 30 years old. Hence by end of FY2017, plantation segment will turnaround and generate income. It is likely by FY2017 planting activities may taper down reducing operating expenses.

· 1 hectare of oil palm trees estimated to produce around 3 tonne of CPO and 1 tonne of palm kernel. In FY2017 plantation segment is expected to generate around RM25m revenue and double in FY2018. Plantation revenue is expected to continue to grow markedly until 2020 as more oil palm trees matures.

· AZRB currently has an estimated 16,000 hectare land in West Kalimantan Indonesia, of which an estimated 7,500 had been planted. The oil palm plantation is estimated to worth USD80m which translates to around RM320m or around RM0.65sen per share.

Toll Concession (EKVE)

· EKVE construction began in FY2015 and expected to be completed in 3 years’ time, by FY2019.

· Expected 140,000 motorist will travel in EKVE, estimated to generate revenue in excess of RM150m.

PROJECTIONS

· Several assumptions were made base on the facts above to make the projections

o Construction Segment –

§ Revenue grow at 5% per annum

§ Additional revenue from MRT (SSP line) worth RM220m per annum

§ Maintain its current net profit margin.

o O &G Segment - growth at 4% per annum + maintain its current net profit margin.

o Plantation segment

§ – oil palm trees maturity in stages FY2016/1,500 hectare, FY2017/4,000 hectare, FY2018/6,500 hectare, FY2019/8,500.

§ Revenue calculated using CPO price at RM2,500 P/MT.

§ CPO production cost at RM1,100 per MT.

§ Planting activities continued at 2,500 hectare per annum cost RM35m.

o Property Segment – Growth at 10% per annum + maintain its current net profit margin.

o EKVE will start in 2H 2019, expecting at least 140,000 motorist per day averaging RM3 per motorist.

In summary AZRB’s profitability jumping several folds entirely dependent on

1. Turnaround in plantation segment with expectation that oil palm trees planted in 2013 and 2014 will mature in FY2016 and FY2017 until 10,000 hectare oil palm trees producing fruit bunches + CPO prices maintain at RM2,500 P/MT.

Maintain reasonable growth rate for all segments especially construction sector.

Trading Challenge

Many people committed to buy stock is very easy, when come to profit taking and cut loss is one of the most difficult part in trading world, talking about profit taking is dealing with greed and stop loss is dealing with fear, cutting loss is a must in trading world because it stopping my capital continue to loss, in order to stay alive in trading world... it is a must !!! it is not an option, else I suggest you get out of the trading and you are not suitable.

I wanted to used simple example to share on the cut loss ... you bought an egg and prepare to used it for fry rice, some how you notice/suspect the eggs you pick was/may turn bad.... the question now is shall out throw/scrap the bad one and pick another .... or nevermind bet or hope the suspicious "bad" egg will be good and risk the good rice which is ready to cook ? you make the call... I am believed in order to win I got to know how to prevent I am loss in the market... if I notice I am wrong... I got to admit and cut the loss and make a next move.

As a reminder for myself

I am always remind myself If the trend is go again me and violated my SL limit, I will cut loss base on the risk preference.

Stop Loss is painful process because I making loss, but it is necessary to take it, it is very important because it protect my capital to ensure I am stay in the market.

DISCLAIMER:

Stock analysis and comments presented on klseelwavetrading.blogspot.com are solely for education purpose only. They do not represent the opinions of klseelwavetrading.blogspot.com on whether to buy, sell or hold shares of a particular stock.

Investors should be cautious about any and all stock recommendations and should consider the source of any advice on stock selection. Various factors, including personal or corporate ownership, may influence or factor into an expert's stock analysis or opinion.

All investors are advised to conduct their own independent research into individual stocks before making a purchase decision. In addition, investors are advised that past stock performance is no guarantee of future price appreciation.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on KLSE Technical Analysis

Nov 20th : Market Report on Vivocom. Close $1.74 with volume 68.24m.

Created by mwong3 | Nov 21, 2020

Nov 18th : Market Report on Vivocom. Close $1.86 with volume 33.4m.

Created by mwong3 | Nov 18, 2020

Nov 18th :Morning Session Vivocom cosed $1.83 with volume of 23.1M.

Created by mwong3 | Nov 18, 2020

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2025-01-03 16:00:00

ADX

Hourly

BUY

2025-01-03 11:30:00

OBV

30 Mins

BUY

2025-01-03 10:00:00

ADX

30 Mins

BUY

2025-01-03 09:55:00

OBV

5 Mins

BUY

2025-01-03 09:55:00

TURTLE SYSTEM 55

5 Mins

BUY

Apps

Top Articles

1

2

CEO Morning Brief

3

CEO Morning Brief

4

Good Articles to Share

‘THINGS ARE GETTING WORSE’: Credit card debt skyrocketing to concerning levels #shorts

5

Mercury Securities Research

6

Good Articles to Share

Nvidia's Blackwell could propel 2025 revenue to $200B: Strategist

7

Good Articles to Share

Stock market today: Dow, S&P 500, Nasdaq fall as comeback bid falters and Tesla, Apple slide

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

riff

dont set high hopes on yalam companies, my 2 cents.

2016-05-13 00:28