This update mainly focus on Nike's performance that facilitate projection of Prolexus's future performance and Q2FY2015's performance, due to announced tentatively on today (20 Mar). Keynotes as below:

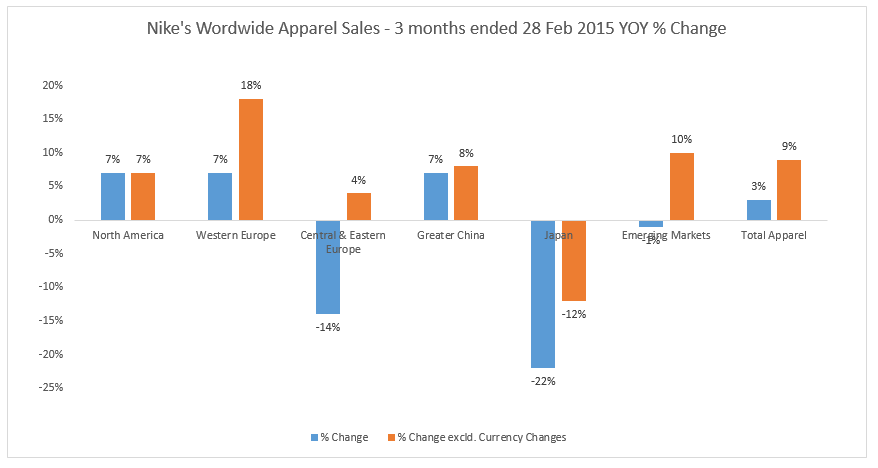

- Nike's Worldwide Apparel sales growth 9% yoy excluding currency changes (ex-forex) or 3% if inclusive of currency changes

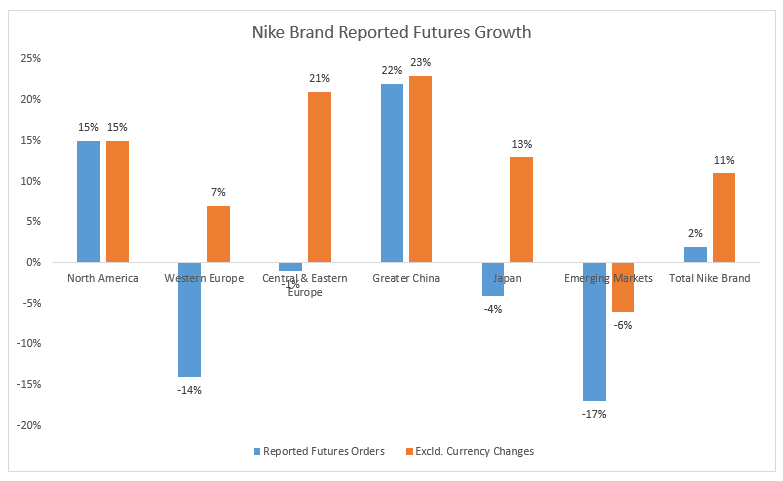

- Future orders of Nike Brand growth 11% ex-forex or 2%

- Future orders growth would have been even higher if not compared to strong growth last year due to the soccer World Cup

- Inventories up 12% due to higher inventories in wholesale business and growth in Direct to Customer

- Wholesale inventories increase 17% in units, but offset 5% by changes in average product cost and Forex change.

Positive implication of Prolexus's earning:

- Higher growth in current sales and future orders indicate strong apparel orders to Nike's worldwide suppliers. Prolexus should be one of Nike's supplier that receive strong order, hence boosting potential sales growth

- Nike's reporting of market-beating earning result shows, one again, Nike's continuous ability in growing its business worldwide, even amid challenging macroeconomic condition. This indicate Nike need to rely on its supplier in the long-run to achieve sustainable success.

Risks:

- Strong demand from Nike may not be met by Prolexus due to capacity constraint or any delay in production expansion. Hence, risking losing order or damping relationship with Nike.

Opportunity:

- Given the opportunity to ride on Nike's high sales growth, Prolexus should expand aggressively to (i) fulfill Nike's higher demand (ii) expand its market share of Nike's order (iii) but most importantly, to achieve a better economic of scale to stay competitive among this competitive industry. Apparel industey is very competitive. In order to stay relevant and competitive in the long-term, Prolexus has to gain a competitive edge in production cost through better economic of scale. Although aggressive expansion to cater Nike's need increase its risk due to higher fixed cost and higher reliance on single-customer, this is a necessary step to strengthen its relationship with Nike. Besides that, Prolexus's strong balance sheet and OCF allow them to take the necessary risks of expansion.

View on Investment:

Prolexus's share price has appreciated significantly (+63% YTD) and now have a valuation of TTM PE at 9.35x, which is relatively high compare to its PE in the past 2 years. Market is giving a high valuation due to expectation of impressive Q2 earning result (to be announced tentatively today). Q2 have been one of the best quarter of Prolexus in term of revenue achieved. The strong expected revenue is further boosted by strengthening of USD (around + 8% QOQ).

At this valuation, I would give Prolexus a HOLD rating pending on the earning announcement later of today due to:

i) concern on its ability to make timely production expansion to meet the higher demand

ii) relatively high valuation - which has exceeded my previous DCF/SOP-based TP of RM1.89

iii) although its key customer's demand is growing rapidly, but the positive macro-situation is offset by its production capacity constraint and the risks due to (i) intense competition (ii) high customer concentration risk

JT Yeo

I am amazed that you use Nike's earnings to gauge Prolexus earnings. Nike has 600+ factories making contract manufacturing for them, does that means all those companies will report increase in earnings as Nike?

2015-03-20 10:22