Bull & Bear Research

Prolexus Bhd - an undervalued gem with solid track record

Steve Ong Wei Siang

Publish date: Mon, 19 Jan 2015, 06:10 PM

1.0 Summary

Prolexus is a long-time apparel manufacturer with customer from international brands like Nike. Prolexus's has a healthy balance sheet with net cash position of RM0.20 per share. Sales and profit growth has been solid and consistent in the past 4 years. The stock has been trading with low valuation ranging 3.5-8.0x P/E in the past 1 year despite 4 years PBT's CAGR of 45%. My target price to this stock is RM2.28 (Kindly refer to Section 7.0 Projection and Valuation for the basis of valuation). I expect Prolexus FY15's PAT to growth 58% (on my optimistic scenario) due to (i) better economy growth and consumption prospect of US (ii) Weaker RM to boost competitiveness and provide forex gain (iii) higher operating margin after a surge in production wages due to minimum wage implementation in 2014.

Prolexus is a long-time apparel manufacturer with customer from international brands like Nike. Prolexus's has a healthy balance sheet with net cash position of RM0.20 per share. Sales and profit growth has been solid and consistent in the past 4 years. The stock has been trading with low valuation ranging 3.5-8.0x P/E in the past 1 year despite 4 years PBT's CAGR of 45%. My target price to this stock is RM2.28 (Kindly refer to Section 7.0 Projection and Valuation for the basis of valuation). I expect Prolexus FY15's PAT to growth 58% (on my optimistic scenario) due to (i) better economy growth and consumption prospect of US (ii) Weaker RM to boost competitiveness and provide forex gain (iii) higher operating margin after a surge in production wages due to minimum wage implementation in 2014.

2.0 Business Background

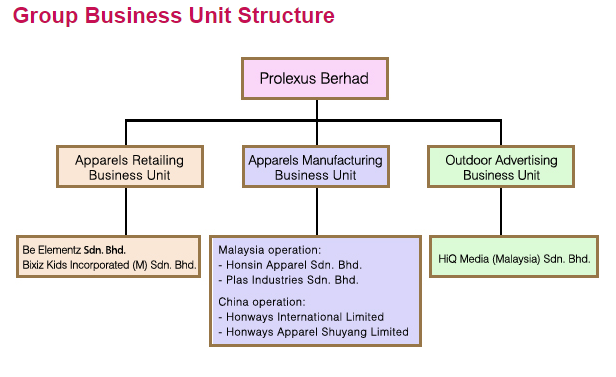

Core Business: Apparel Manufacturer

Established since 1976 and listed on Bursa Malaysia’s Main Market since 1993, Prolexus is mainly a garments manufacturer or Original Equipment Manufacturer (OEM) for internationally brands. In FY13, 2 major customers contributed to 87% of Prolexus total revenue. Nike Inc(Nike), is believed, to be the largest customer of Prolexus although the exact contribution is not known.

Porlexus has 3 factories in:

|

|

Location

|

Build-Up Area (Acres)

|

Plant Revenue (FY13)

|

|

i)

|

Batu Pahat, Johor

|

1.8

|

RM172m (Malaysia)

|

|

ii)

|

Seberang Perai, Penang

|

0.6

|

|

|

iii)

|

Jiangsu, China

|

3.0

|

RM57m

|

63% of the sales is from US customers, Prolexus enjoys forex gain advantage from the raising USD as seen from the previous financial results. (63% could be a good proxy to Nike’s contribution to Prolexus’s sales)

Other Business: Outdoor Advertising

Prolexus also provide outdoor LED screen advertising services under the brand name “PowerScreen” which contributed to 3% and 10% of the group’s revenue and PAT.

|

| Source: Company Website |

Besides the companies shown above, under the Group is also Novel Realty SB, which is an investment holding company that hold Prolexus's non-core investment real estates (i.g. bungalow house and vacant land). The company has over RM14m of asset currently (24% of the Group's PPE)

2.1 Management

- Ahmad Mustapha Ghazali, Executive Chairman - aged 66, appointed since 1993 and become chairman in 2002. Member of a few overseas and local accountant associations and institute including Chartered Association of Certified Accountants (UK) and others. Have directorship in Tambin Indah Land Bhd, Malaysia Packaging Industry Bhd amd Global Maritime Ventures Bhd.

- Lau Mong Ying, MD – aged 65, is the MD since 1993 (21 years ago). Graudated with Bachelor of Commerce in Economics (Nanyang University of Sg)

Non-executive directors

- Lau Mong Ying, MD – aged 65, is the MD since 1993 (21 years ago). Graudated with Bachelor of Commerce in Economics (Nanyang University of Sg)

- Khadmudin bin Mohd Rafik - aged 61, appointed in 2003. Used to be a Senior Police Officer and Assistant Superintendent of Police.

- Lin Cheng-Lang – Taiwaneses aged 75, appointed in 1998. Used to be MD with various textile companies in Taiwan

- Chin Chew Mun – aged 43, appointed in 2012. A Chartered Accountant.

- Boo Chin Liong – aged 53, appointed in 2013. An advocate and solicitor.

3.0 Macro Outlook

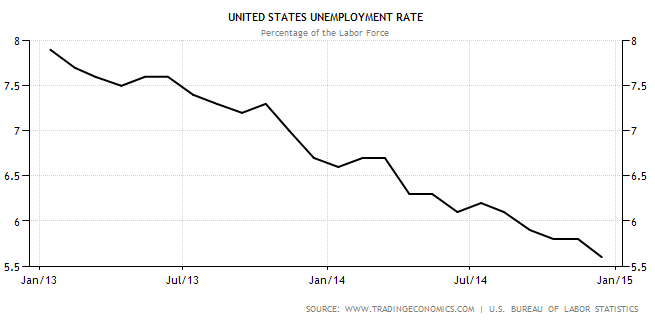

US – Overall improvement in consumer spending

A series of optimistic economic data showing US economics is growing fairly well and consumer spending is generally on the rise with lower unemployment rate, rising retail sales and better Consumer Confidence. Overall, US economic is growing and the consumer is spending more.

On a forward looking note, US consumers are expected to be spending even more due to (1) higher disposable income thanks to lower fuel and energy cost (2) strengthening USD boost consumer spending power on import goods (3) expected continuous improvement in US economy

Hence, Prolexus’s sales to US’s consumers is expected to growth at a higher rate in the next FY.

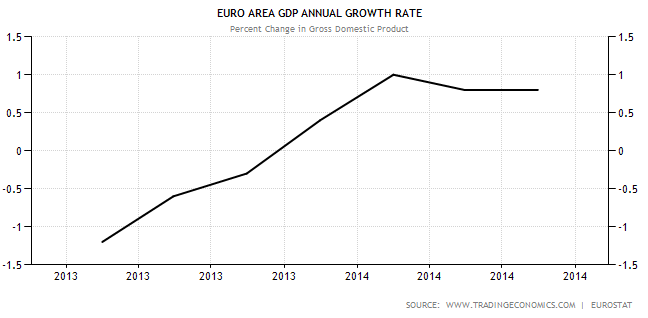

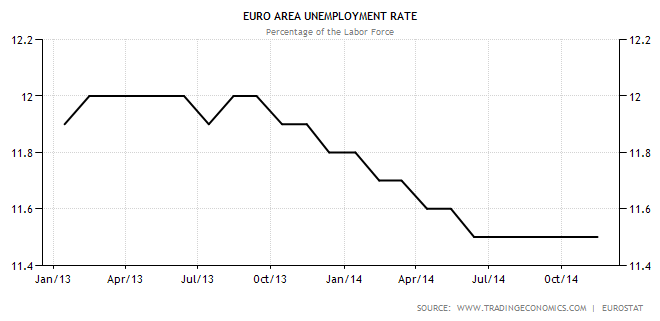

Euro – Slow growth ahead

With Unemployment rate still high above 10%, Euro economy is moving like a snail. Industrial production rose slowly, even the powerhouse of Eurozone, Germany see its Manufacturing PMI only slightly above 50.0 level (51.2 in Dec 2014). IMF expect a moderate Real GDP growth rate of 1.8% in 2015.

Weakening RM a boost to Prolexus’s sales and earning

Against USD, RM is the biggest losers compared to some of other apparel exporters’ currencies. The RM depreciation will not only improve the attractiveness of Prolexus's products, strengthening USD will give Prolexus forex gain due to its exposure to USD-based asset and export.

|

| Source: bloomberg.com |

Rising China Manufacturing Cost

Cost of manufacturing in China has been rising in the recent years and eroding the profitability and attractiveness of China manufacturers. Minimum wages of China are rising at a double-digit rate. Base monthly wage of a factory worker in China is over $400, compared to $130 in Cambodia. Many factories has moved their operation to Vietnam and Cambodia, where operating cost is much lower.

Improving Nike’s Apparel Sales

As the largest customer of Prolexus, Nike’s apparel sales performance have a significant relationship to Prolexus’s sales. Nike apparel sales has been improving in the past few years. In Nike’s 2Q Quarterly report ended 30 Nov 2014, Nike’s worldwide futures orders (for Nike Brand footware and apparel) scheduled for delivery from Dec 2014 to Apr 2015 were 7% higher (11% if excluding currency changes). Accelerating Nike’s orders indicate a good prospect to Prolexus.

|

| Source: Company data |

4.0 Financial Analysis

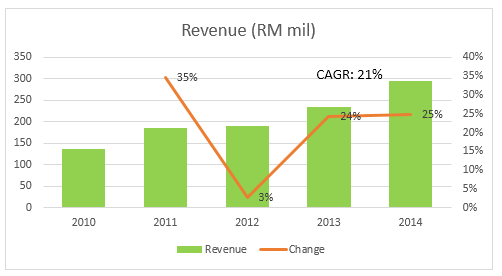

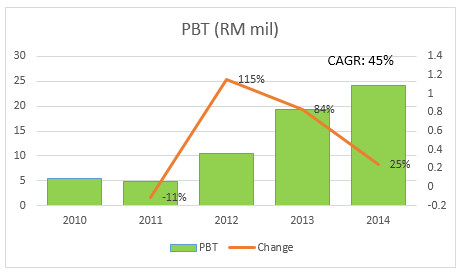

4.1 Past 5 Years Performance

Revenue growing every year in the past 4 years with CAGR at 24%. PBT’s growth was remarkable in FY2012 and FY2013 due to significant efficiency improvement, cost rationalization programmes as well as improvement in China’s plant profit. PBT’s growth normalized to 25% in 2014 (from 84% in 2013) as operating margin reach a plateau.

4.2 Financial Analysis

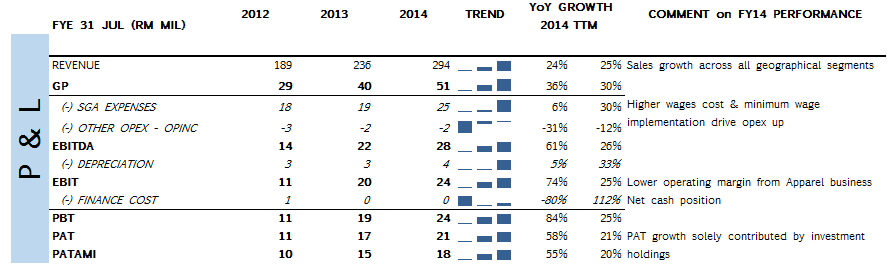

i) Income Statement

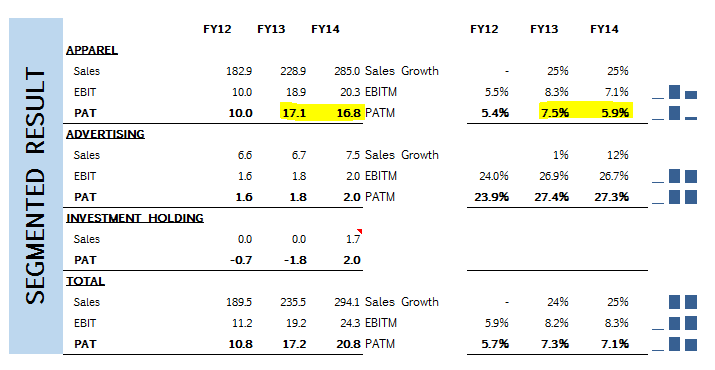

PAT growth decelerate to 21% in FY14 (FY13: 58%). PAT growth is contributed by Revenue growth and Gross Margin improvement but dragged by higher operating cost rise and higher effective tax rate.

In contrast with 21% PAT growth in FY14, Apparel business actually recorded a 1.8% lower PAT despite sales and EBIT grow at 25% and 7.1% for the business segment. EBIT Margin is lower due to higher production wage cost while PAT is lower due to higher effective tax rate. Prolexus's effective tax rate is lower than Malaysian statutory rate at 25% as they have Unabsorbed tax losses (at RM18.5m in FY14), capital allowances and reinvestment allowance. Realization of tax benefit is lower compared to last year, hence the higher effective tax rate.

In fact, the Group's FY14 higher PAT (+RM3.6m yoy) is over-contributed by higher PAT from the Investment Holding segment (+RM3.8m). In 2014 Annual Report of the Group, the chairman attributed the higher PAT, among others, to better margin achieved through production efficiency. However, the number is telling a different story where the EBITM in FY14 is actually lower (to 7.1% from 8.3%).

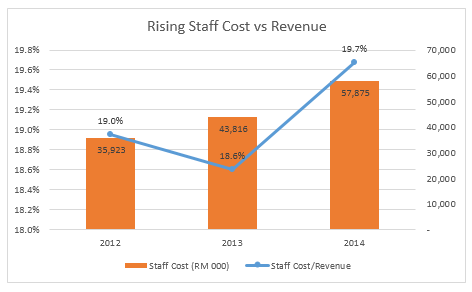

FY14 saw a staggering rise in staff cost to RM58m from RM44m in previous year, which is a 32% rise. Expressed at a percentage of Revenue, staff cost rised to 19.7% of FY14's revenue from 18.6% previously. The rise in staff cost is mainly due to implementation of minimum wage. There was no significant addition of Plant and Machinery in FY14 which indicate that the Group are not heading to automation aggressively to address the issue of rising wage.

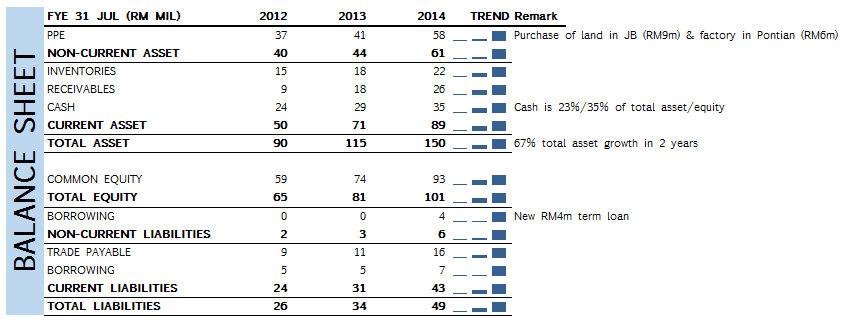

ii) Balance Sheet

FY14 saw an increase of Fixed Asset at RM17m to RM58m mainly due to purchase of a vacant land in Tanjung Kupang, JB (Land) with carrying amount at RM8.7m and a vacant factory in Pontian (RM5.6m). Both purchases are for investment purpose targeting capital appreciation.

Prolexus is very cash-rich with RM35m of total cash and deposit and 80% of it is in USD. Net cash at RM24m.Though the cash hoard, Prolexus do not provide high dividend payout nor cash distribution. Instead, they are constantly looking for investment opportunity.

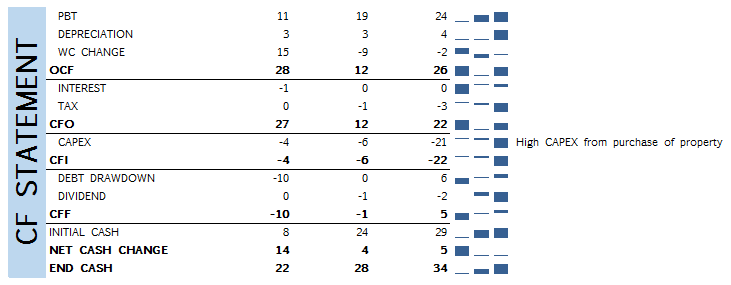

iii) Cash Flow Statement

Good Operating CF at RM26m compared to PBT of RM24m. FY14 saw a high capex at RM21m funded by CF from Operation and drawdown of new Term Loan. RM5m of net cash is generated in FY14, boosting the cash hoard to RM34m.

FY14 saw a better Gross Margin at 17.5% (from 16.8%) but EBIT margin unchanged at 8.3% due to rising operating cost. This lead to flat PBT margin YOY. Together with higher effective tax rate, Net Margin fall 0.2% to 7.1%.

iv) Ratios

ROE and ROA is remarkable at 20.6% and 13.9% respectively. Prolexus has good liquidity with Current Asset and Cash cover Current Liabilities at 2.1x and 0.8x. Cash-to-cash cycle improved to 29 days (from 33days)

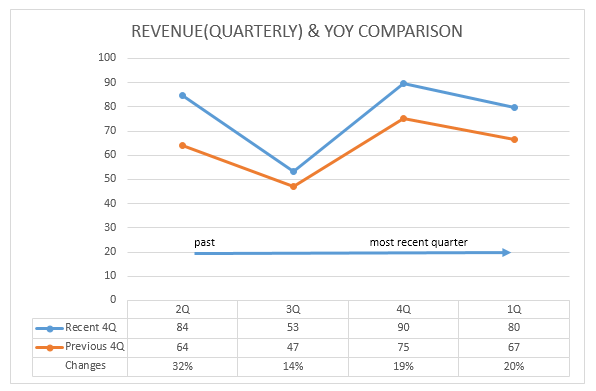

4.3 Recent 8 Quarters Performance Review

Revenue increased YOY in all of the past 4 quarters at 14 to 32%.

PAT rised 32 to 62% YOY in the past 4 quarters except a 12% YOY drop in 3QFY14 due to an Unrealized Forex Loss of RM1.7m from weakening USD at that period.

5.0 Future Prospect

i) Continuous growth in revenue

Prolexus has a good track record of sales growth in the past 4 years with CAGR at 21% and the increase is across customers from all regions. Moving forward, I am comfortable with the Group’s ability to secure more orders from existing customers. Besides that, with better prospect of US economy and consumption, orders from the US customer will have a brighter prospect.

ii) Weak RM against USD a gift to competitiveness and earning

RM has been weaken for over 10% against USD and generally against other currencies since FYE 31-Jul-2014. This will translate to higher sales value and Gross Profit in RM for orders to US and oversea counties in the coming quarters. In the longer term, oversea customers will request Prolexus for a lower selling price in their home countries to take a share of the benefit. Eventually, weak RM will boost competitiveness of Prolexus’s production in Malaysia and increase their sales. In 2014 Annual Report, the Group has net exposure to USD asset of RM29m and with every 10% strengthening of USD will increase Prolexus’s 2014 PBT by RM2.9m. Though this is just a one-time effect and may reverse itself if RM recover, but Prolexus 2QFY15 PAT is expected to be boosted by the forex gain. Prolexus’s China operation is generally not beneficial to the weak RM.

iii) Oversea operation expansion

With a stronghold of cash, good OCF and net cash position, Prolexus is financially capable of taking up big investment like setting up new plants in other counties like Vietnam and Cambodia where they can exploit the cost advantage. Should this happen, operation cost and depreciation charge will be higher in the near term before any earning contribution come in. However, it will facilitate the Group's long-term expansion.

iii) Oversea operation expansion

With a stronghold of cash, good OCF and net cash position, Prolexus is financially capable of taking up big investment like setting up new plants in other counties like Vietnam and Cambodia where they can exploit the cost advantage. Should this happen, operation cost and depreciation charge will be higher in the near term before any earning contribution come in. However, it will facilitate the Group's long-term expansion.

6.0 Risks

i) Customer concentration risk

Sales of 2 major customer contributed to over 80% of the Group sales. Loss or significant reduction of order from one of these 2 customers will have a serious impact to Prolexus’s financial. This is a low-risk-high-impact event.

ii) Competition risk

Apparel manufacturing is a globalized business. Just like manufacturing, competition is always happening among the major manufacturing counties like China, Vietnam, Cambodia, North America and other counties. Any sudden or systematic rise in competitiveness for their competitors from other counties may cause the Group loss in market share. The weaken RM is an example of the change in competition environment, though it is in favor of Prolexus.

iii) Rising production wage cost

A continuous rising wage cost in China manufacturing will erode Prolexus's China profitability and competitiveness. Besides that, the Group has constantly facing difficulties in recruiting production operators, which may cause higher wage cost in order for the operation to recruit enough operators.

iv) Investment risk from non-core asset

As noted earlier, the Group's investment holding has RM14m worth of investment real estate in the form of vacant bungalow and several vacant lands. It is 9% of the total asset. Prolexus has low dividend payout rate (14% in FY14) but choose to invest the cash generated from operation in non-core real estate. The investment is not expected to generate much shareholders'value in the medium-term as it is not cash-flow generating (due to its vacant condition). Shareholder can only see value if there are sales of the asset or revaluation done in the future. Should the management distribute the cash to shareholders and let them decide what investment is more proper to them? Besides that, lower asset base also give financial reporting benefit and support better valuation.

7.0 Projection and Valuation

7.1 Current Market Valuation

|

| Based on closing price on 16-Jan-2014 |

As on 16-Jan-2014, the market give Prolexus a 7.5x P/E valuation, way lower than FBMSmallCap P/E of 14.77 despite good track record of growth in the past and bring prospect ahead. EV/EBITDA at 5.2x shows the acquisition cost of the Group can be recouped with 5.2 years of FY14's EBITDA. That seems to be cheap considering the Group's ability in generating cash and stability of EBITDA in the past.

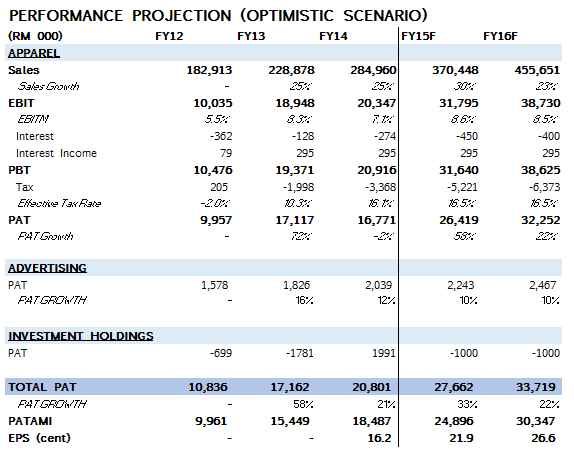

Optimistic Scenario is based on:

i) Higher sales value in RM due to depreciating RM.

ii) Stronger sales order from customer due to stronger demand from US customers and lower price of Malaysia goods (due to weak RM)

iii) After implementation of minimum wage in 2014, wage cost rise normalized. EBIT Margin improved to 7.8% (before considering forex gain)

iv) Forex gain of RM2.9m

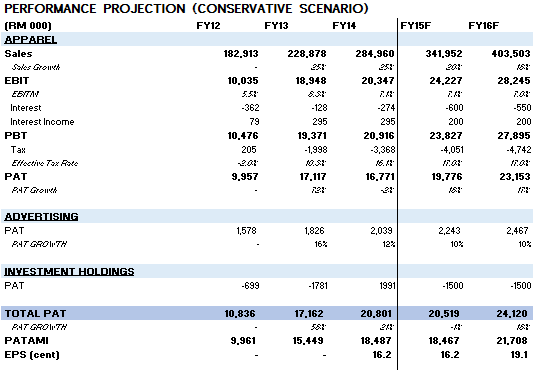

Conservative Scenario is based on:

i) Lower sales growth despite weaker RM

ii) Higher EBIT Margin due to continuous rise in wage cost.

iii) New capex that cause higher operating cost, depreciation charge, higher interest cost (new borrowing) and lower interest income (from cash drawdown).

iv) Lower forex gain of RM2.0m

v) Higher effective tax rate.

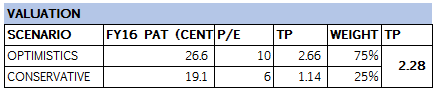

My target price is set at RM2.28 (61% upside from 16-Jan-2014 closing). I think the optimistic scenario is 75% possible as (i) Weak RM situation will sustain longer to benefit Prolexus (ii) Operating cost growth should normalize in FY2015 after a big jump in FY2014 (iii) No significant action or plan in capex yet.

Factors for revaluation:

My TP will be revised if:

i) There are announcement of significant capex

ii) Stronger than expected RM recovery

iii) Actual result deviate significantly from my estimate as review quarter by quarters

Disclaimer: This research is not a recommendation to buy or sell the securities, but only for informative purpose to help reader to understand the company better. Despite my target price is higher than current market price, the stock price may not reach the target price due to various factors, including significant deviation of my estimate with the actual figures. Readers are advised to perform due diligence before making any investment and after reading my research as my estimation and projection can be highly fallible.

http://bullandbearresearch.blogspot.com/2015/01/prolexus-undervalued.html

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Bull & Bear Research

Signature International Bhd (SIGN) - At the sweet spot of booming housing completion

Created by Steve Ong Wei Siang | Apr 08, 2015

Prolexus's key customer earning's update - Nike Inc. Profit Beat Analysts' Estimate

Created by Steve Ong Wei Siang | Mar 20, 2015

OKA - Driven by steady sales growth and efficiency gain

Created by Steve Ong Wei Siang | Jan 14, 2015

Discussions

6 people like this. Showing 21 of 21 comments

cipapo, why u say tipu? I am new to writing research, if you spotted any area of my research is wrong, over or under estimate, bias or anything else. Feel free to comment. It's not the best, just hope my research can be better and better.

2015-01-19 19:18

Wont go too far from $1.50-1.60 , except there are corporate action that can lead to revaluation of current price or new catalyst exploited.

2015-01-19 19:40

Have bought since 3Q 2012. 1 share split & 1 bonus issue. What next coming...Huat aar...

2015-01-19 20:21

Steve, nice work. If you pay attention to recent announcement from Prolexus, Prolexus could be on expansion mode again.

http://www.bursamalaysia.com/market/listed-companies/company-announcements/1792373

http://www.bursamalaysia.com/market/listed-companies/company-announcements/1842557

If these are really signs of expansion, we can expect bountiful harvest three years from now!

2015-01-19 20:48

A very detailed analysis - maybe you can discuss the impact of TPPA? ESOS and low dividend yield are issues for me. Its closest peer Magni-Tech also trades at similar TTM PER with 4.6% yield, although the management was not investor friendly. Prefer Luen Thai (311 HK) for its 3-4x forward PER and ~8% yield.

2015-01-19 20:53

Just my opinion, Ive gone through Magni and Prlexus last January but end up giving both a miss. From quantitative point of view, both companies would be "B+". When it comes to corporate governance and disclosure, Prlexus would be a "D" and Magni an "E". Prlexus fair better in management discussion and analysis but most information are general numbers like how much revenue/earnings changes, nothing about the business. Magni even worse, statement seems to be copy and paste every year which is less than 3 sentences.

As for the TP, I think assigning the optimistic scenario PE of 10 is abit too optimistic given that historical record has shown that Prlexus has always been valued at PE6-7 level, a PE of 8 in one year would be realistic, a 10 would require a huge shift in investors' expectation towards the company. Although in saying that, doesn't mean it is not undervalued.

If consider PE of 10 as the fair price to pay for it's NTA. And consider that the ROE of 20-22% is sustainable, NTA 0.86 x ROE 20-22 = RM1.70-1.90 would be a fair price. Returns come from = PE Expansion + Assets/Earning appreciation + Dividend increase. The hardest of all 3 to estimate is PE expansion, although earnings estimate are already a challenge, thats why even analysts misses their estimates, and consider that we human is always over confident in our judgement, a 15% discount to your own TP make sense. Last thing, considering that during the bullish cycle of 2009-2013, Prlexus PE barely changed considered it's solid growth record over the years, so what is the probability that the PE will notch up by 3 in 2015, and if your 50% growth estimate is accurate?

Lastly, the reason i gave both a miss because I have no idea about their competitive advantage, although ROE number does indicate there is one. How does Nike choose manufacturers, how long are their contracts, how/who are the competitions/tors? Is it on price, quality? etc. And of course because I dont have these information, my margin of safety has to increase to offset those unknown risk. Thus I give them a pass.

2015-01-20 06:41

JT Yeo, salute, appreciate your comment. You are right, PE estimation is more like a guestwork, especially smallcap company with a more short-term investor than institution investor, PE can fluctuate in a large range. Perhaps i should not put a fixed PE to the stock (and put myself on the chopping table), maybe a range of possible PE or just stay away from setting a TP. I think Prolexus is a good investment though not informative, but one should not overweight too much in their portfolio as their 2 major customers contributed to over 80% of sales, which can be very dangerous if anything happen from this 2 customers.

2015-01-20 10:34

Ven Felix: 10x times forward P/E is quite high considering the stock hardly touched 10x TTM P/E before. Will relook into the historical P/E and find any catalyst to review my valuation.

CCCL: The next quarter report should be explosive. With 10% USD/MYR appreciation, there could possibly be a RM2-3m of forex gain with their USD asset exposure. Gross Margin could possibly gained over 5%. Is an overall big pushed to the PAT. But trader have to be careful, Smart Money may take this opportunity to push the price high before the earning announcement to stimulate retail trader's buying. Then they can sell-on-news after the good news that lead even more retail buying.

Chonghai: thanks for bringing out. Maybe it's still on seed-stage, but will look into it.

kaonryou: TPPA? A new perspective for me, will review. The company like to keep cash. They prefer invest in vacant land rather than give it to the shareholders. Are they very ambitious because they think the cash can be invested more efficiently with them? Or are they simply another chinaman company who like to hoard all the wealth?

2015-01-21 09:56

kklow77. You are welcome. Carepls seems interesting due to its capacity building story. But there are a lot of capacity coming from the big competitors as well. The industry is very competitive now with price war happening, Supermax is doing badly. But the recent financial seems doing well for Carepls. But to gauge the future better, a deep analysis is still necessary. I haven't done that, so can't comment too much. It's in a situation of either very good (if margin & market share can sustain) or bad (if Avg Selling Price is low like Q3 happen again).

2015-03-01 23:59

Hi JT Yeo and Steve Ong Wei Siang,

May I make friend with you guys? If you're willing to, please kindly drop me an email at bosx8989@gmail.com for further connection.

Nice to meet you all.

2015-03-18 23:59

Post a Comment

Featured Posts

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-05 16:50:00

EMA 5

10 Mins

SELL

2024-07-05 16:35:00

EMA 5

5 Mins

SELL

2024-07-05 16:25:00

EMA 5

5 Mins

BUY

2024-07-05 16:20:00

EMA 5

5 Mins

SELL

2024-07-05 16:00:00

ADX

5 Mins

SELL

Apps

Top Articles

1

TA Sector Research

BWYS Group Berhad - A Leading Sheet Metal and Scaffoldings Manufacturer

2

Kenanga Research & Investment

3

4

Kenanga Research & Investment

5

save malaysia!

6

TA Sector Research

7

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Icon8888

Like

I have this stock

2015-01-19 18:54