Bull & Bear Research

Signature International Bhd (SIGN) - At the sweet spot of booming housing completion

Steve Ong Wei Siang

Publish date: Wed, 08 Apr 2015, 02:18 AM

1.0 Investment Summary

Signature International Bhd, a branded distributor, manufacturer and retailer of modular kitchen system under the brand name of Signature Kitchen, is at the sweet spot of booming number of service apartment/condominium (SA/Condo) completion in 2015-2017.

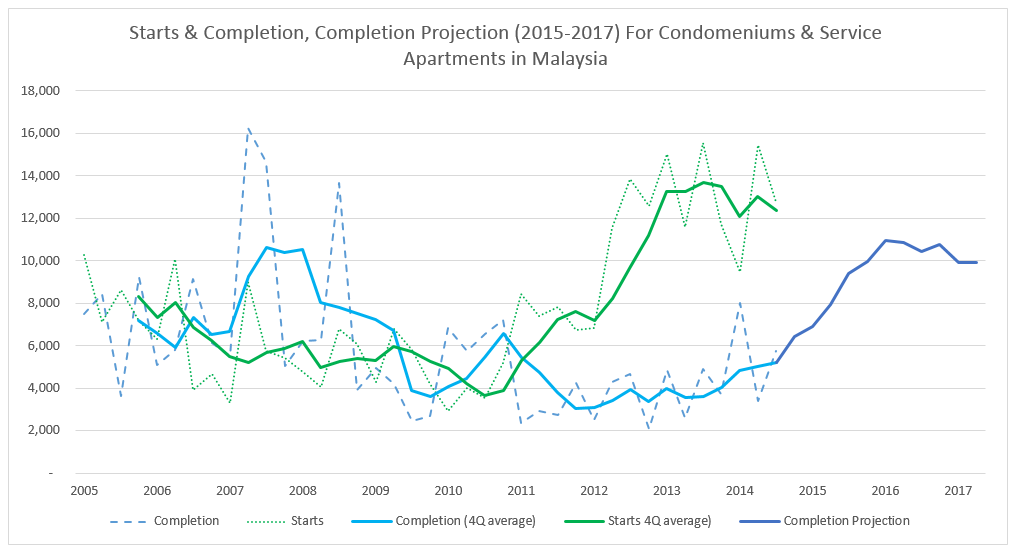

Housing starts for SA/Condo in Malaysia has plateuaed in year 2013-2014 while completion data is still below half-of-2008's peak. As historically, completion lagged starts 3 years, number of SA/Condo completion is set to boom beginning from year 2015 and is projected to overtake 2008's peak in 2016-2017. While this is a bad news for the property market, SIGN will be the clear winner from this development as 70% of SIGN's FY2014 sales is derived from Project Sales, where SIGN partners with Property Developers to provide kitchen systems to SA/Condo projects-near-completion.

I give a Buy rating on SIGN with TP of RM3.70 (64% upside) based on 10x FY16 earning, which is generally in line with forward PE given to furniture/particleboard and FBMSmallCap stocks. The Buy rating is based on:

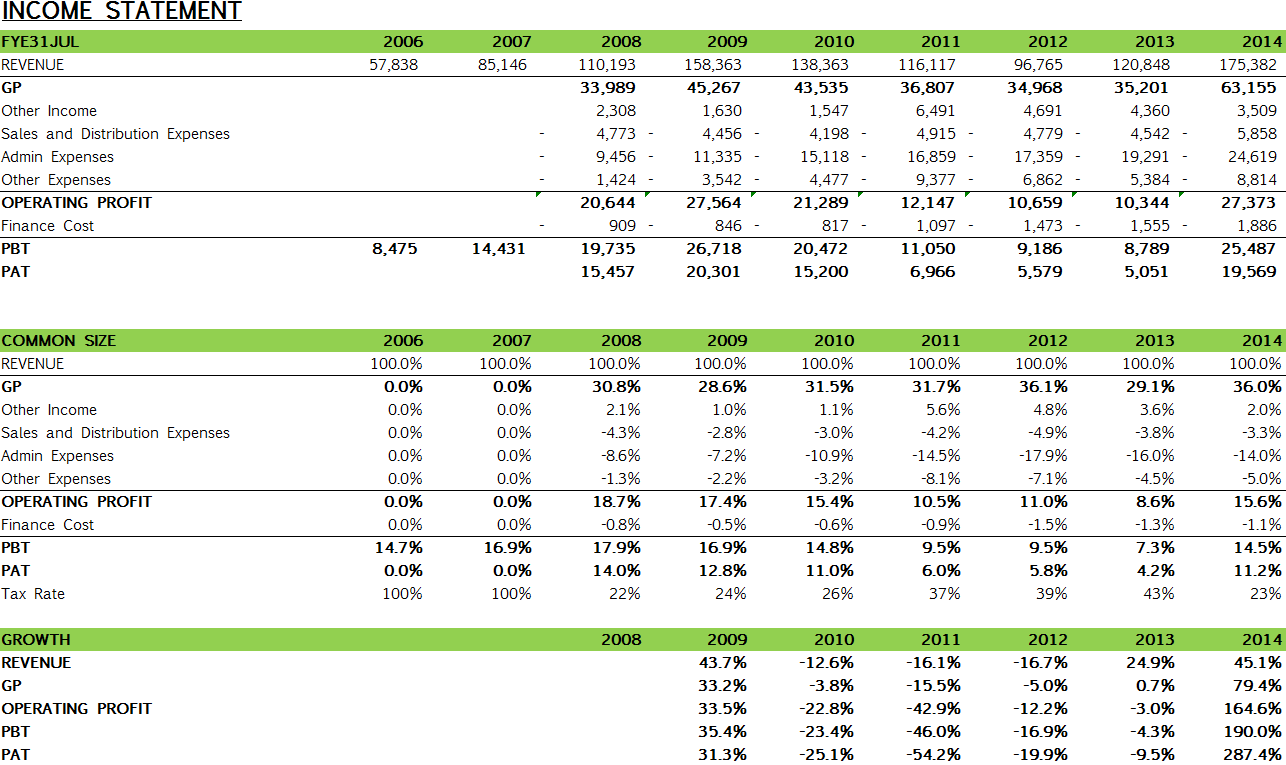

i. SIGN's PAT is projected to double in FY15 and grow at 2-Years-CAGR of 24% for FY16-17 as a) strong sales growth in FY15-17 (CAGR 22%) riding on the booming number of SA/Condo-to-be-completed b) margin improvement from greater economic of scale (Q2FY15 EBIT Margin at 24.7% vs FY14 at 15.6%)

|

|

|

Source: NAPIC |

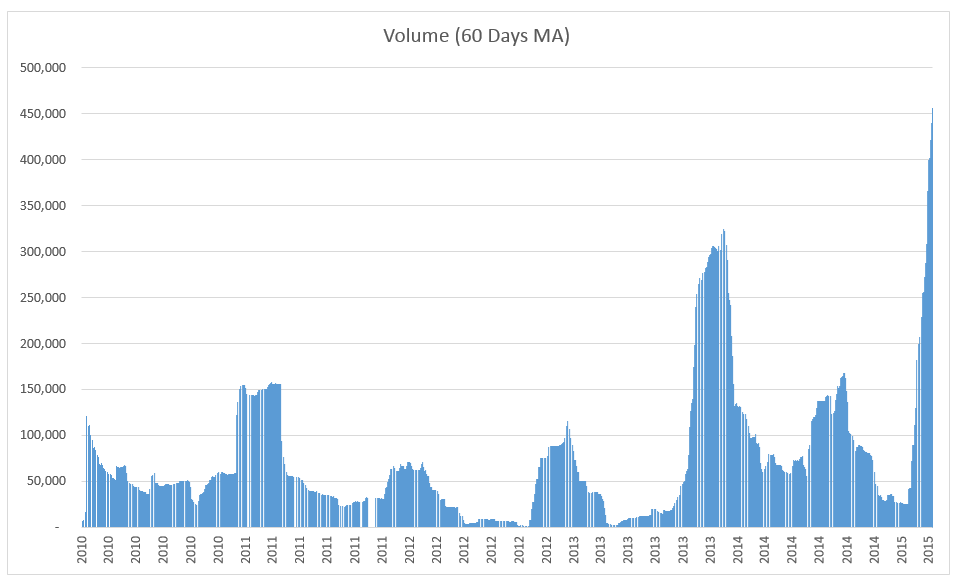

ii. Average trading volume recently surged to 5 years high. SIGN's stock used to have low liquidity.. The improved market interest will provides better trading liquidity and will support better valuation.

|

|

|

Source: Yahoo Finance |

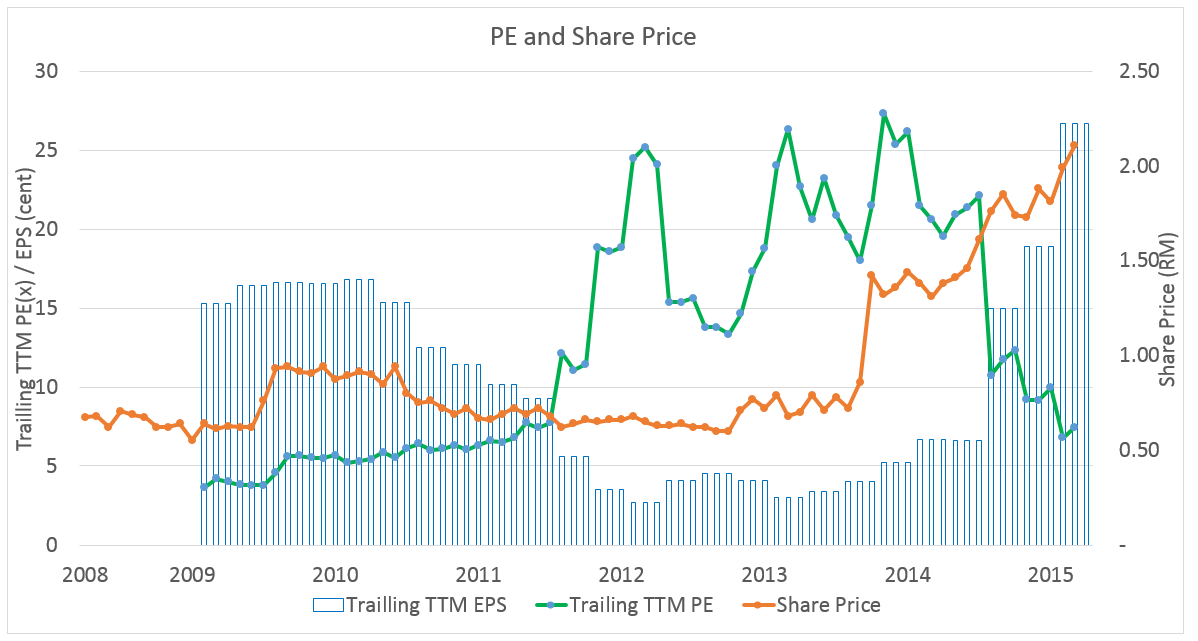

iii. SIGN's stock is still undervalued. Though gaining 190% in 2 years time, with TTM PAT have grown 785% for the same period, valuation is still at 3-years-low at trailing TTM PE of 8.4x and FY16 PE of 6.1x. The current valuation is unreasonable given FY15 will be a record-breaking year for SIGN for its sales, profit and margin. SIGN is an undervalued growth stock.

|

|

|

Source: Yahoo Finance, Company |

2.0 Business Description

The brand name of Signature Kitchen under SIGN is the largest and, in my view, most-well-known kitchen system provider in Malaysia. With over 20 retail showrooms in Malaysia as well as various marketing and branding activities, SIGN has built-up its name toward Malaysians. SIGN is also in the affordable kitchen market under brand "Kubiq" launched in 2009. Pricing of Kitchen set for Signature Kitchen starts from RM20,000 while Kubiq's starts from around RM5,000.

As in FY14, 70% of SIGN's sales derived from Project Sales where SIGN secures projects from developers to provide kitchen to SA/Condo units as part of the developers' promotional strategy to attract buyers. While there are others premium kitchen brands available in the market, the brand Signature Kitchen has a competitive edge over other competitors due to better branding and popularity. In the past, Project sales have been cyclical following housing market cycle. This is explainable as SIGN only come in to provide kitchen for a project near its completion stage. Hence, SIGN's project sales generally correlate with SA/Condo's completion volume as SIGN provide kitchen to SA/Condo projects.

The remaining 30% of sales contributed from retail business generated via its retail outlets. SIGN's key strength is its branding. As it adopt pull-marketing strategy, retail customers are generally walk-in customers. Hence, headcount in retail outlets can be minimized since sales activities are minimal for retail segment. This also provides better operational efficiency. Unlike project sales, retail sales are non-cyclical and have been stable at the range of RM40m-50m annually even during Global Financial Crisis in 2008-2009.

Over 95% of SIGN sales are from local market. Besides providing kitchen system, SIGN also provide kitchen white goods (appliances) to its customer under third-party brands as well as interior design services. These are mostly value-add service. Kitchen business is still the core income generator.

Based on Initiation report done by CIMB Research in Oct 2013, 75% of SIGN's production cost comes from raw materials, while the rest are subcontractor fees (14%) and kitchen white goods (11%). The major raw materials used are wood-based like chipboard and medium-density fibreboards (MDF), comprises of 40% of raw material cost. At the same report, also mentioned is that SIGN is able to adjust its production capacity quickly as most of the high-volume raw-materials (like MDF) are outsourced. Only the low-volume-high-value-added products are handled by own factory. SIGN is using sub-contractors for the kitchen installation.

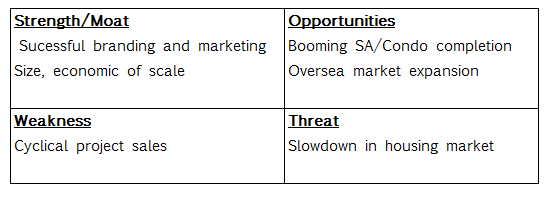

2.1 SWOT Analysis

3.0 Financial

4.0 Projection & Valuation

5.0 Risks

Project delay

SIGN come into a property development project at its final stage. Any delay in project completion will defer SIGN's sales.

Material cost hike

As time from securing projects to work start for project sales can be long, any increase of material cost during this period may not be transferable to the customers.

http://bullandbearresearch.blogspot.com/2015/04/signature-international-bhd-sign-at.html

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Bull & Bear Research

Prolexus's key customer earning's update - Nike Inc. Profit Beat Analysts' Estimate

Created by Steve Ong Wei Siang | Mar 20, 2015

Prolexus Bhd - an undervalued gem with solid track record

Created by Steve Ong Wei Siang | Jan 19, 2015

OKA - Driven by steady sales growth and efficiency gain

Created by Steve Ong Wei Siang | Jan 14, 2015

Discussions

1 person likes this. Showing 3 of 3 comments

Ya, i read that. They have been recommending the stock since 2013. But the liquidity and market interest were always low since then. But since HSC has sold over 10% of the stock, liquidity has since improve significantly. The stock should be the next big thing soon. It's my favorite stock now.

2015-04-09 19:43

Post a Comment

Featured Posts

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-05 15:40:00

EMA 5

5 Mins

SELL

2024-07-05 15:30:00

EMA 5

10 Mins

SELL

2024-07-05 15:30:00

ADX

5 Mins

SELL

2024-07-05 15:30:00

TURTLE SYSTEM 20

5 Mins

SELL

2024-07-05 15:10:00

EMA 5

10 Mins

BUY

Apps

Top Articles

1

TA Sector Research

BWYS Group Berhad - A Leading Sheet Metal and Scaffoldings Manufacturer

2

Kenanga Research & Investment

3

4

save malaysia!

5

TA Sector Research

6

Kenanga Research & Investment

7

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

RonnieKimLondon

CIMB

8 April 2015

Malaysia

Company Flash Note

Signature International | PDF

The signs are here

SIGN MK / SGNA.KL | ADD - Maintained | RM2.25 tp:RM4.23

Mkt.Cap:US$74.19m | Avg.Daily Vol:US$0.25m | Free Float:41.00%

Construction | Author(s): Nigel FOO +60 (3) 2261 9069,

▊ Signature International was one of the top small-cap gainers in Mar, up 14.7% mom (FBMSC was down 2% mom). Even after the recent rally, the stock’s valuation is still attractive at only 6x 2016 P/E, with a 5-6% dividend yield. We maintain our EPS forecasts and target price, based on an unchanged 30% discount to SOP (to reflect its small cap and tight trading liquidity). Securing major jobs and expanding profit margins are potential re-rating catalysts for the stock. Signature remains an Add.

What Happened

Among our small-cap universe, Signature International was one of the major outperformers in Mar, with its share price up 14.7% mom compared to FBMSC’s 2% decline and KLCI’s 0.4% gain during the month. Other major small-cap gainers in Mar included GHL, HeveaBoard and MyEG.

What We Think

We believe Signature’s strong share performance since the start of the year (share price up 21% YTD) was mainly driven by two factors: i) Rising quarterly net profit (refer to Figure 2). 2QFY15 net profit was RM9.1m (after excluding RM3m in provision write-backs) compared to only RM2.9m in 2QFY14 as its order book continued to grow. Signature’s kitchen system production and installation only start when the main contractor completes its job, usually three years after a property is sold. As such, Signature’s current revenue and order book comes from property sales in 2011/2012. The outstanding order book is consistently above RM200m. As the domestic property market peaked in 2014, we expect Signature’s earnings to only peak in FY2017/18. ii) Higher free float. Signature’s free float has improved by around 11% to around 41% currently as one of its major shareholders, HSC Healthcare S/B, has reduced its stake in the company from 20.9% to 9.1%. We view HSC’s selldown in Signature as positive as it has helped improved the stock’s liquidity. In the past, institutional investors had complained about Signature’s lack of trading liquidity. Average daily trading volume in Signature shares in Feb-Mar was 0.67m compared to only 0.01m in Jan

2015-04-09 13:34