CEO Morning Brief

Why Analysts Are Looking Past These Companies’ Falling Revenues

edgeinvest

Publish date: Fri, 06 Oct 2023, 08:47 AM

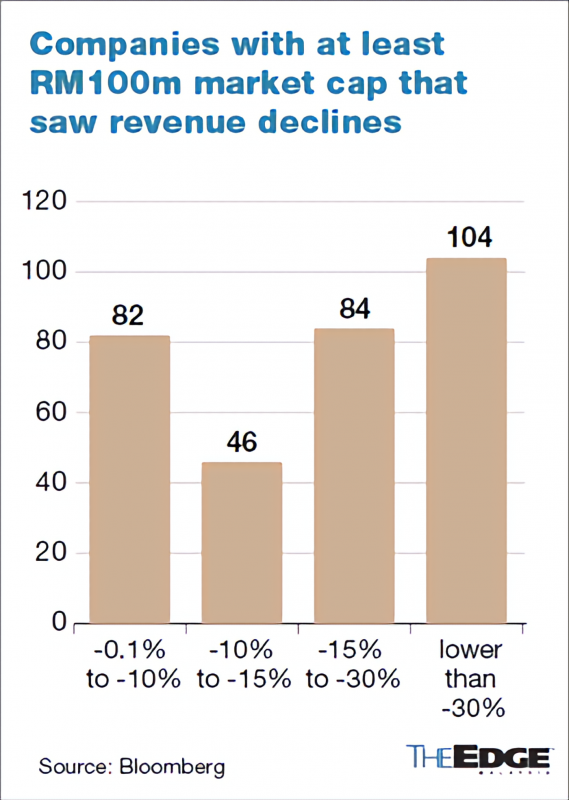

KUALA LUMPUR (Oct 6): Companies’ earnings for the first half of 2023 has been a mixed bag. Almost half or 48% of the 660 companies listed on Bursa Malaysia with a market capitalisation of at least RM100 million experienced revenue declines in the first half of the year.

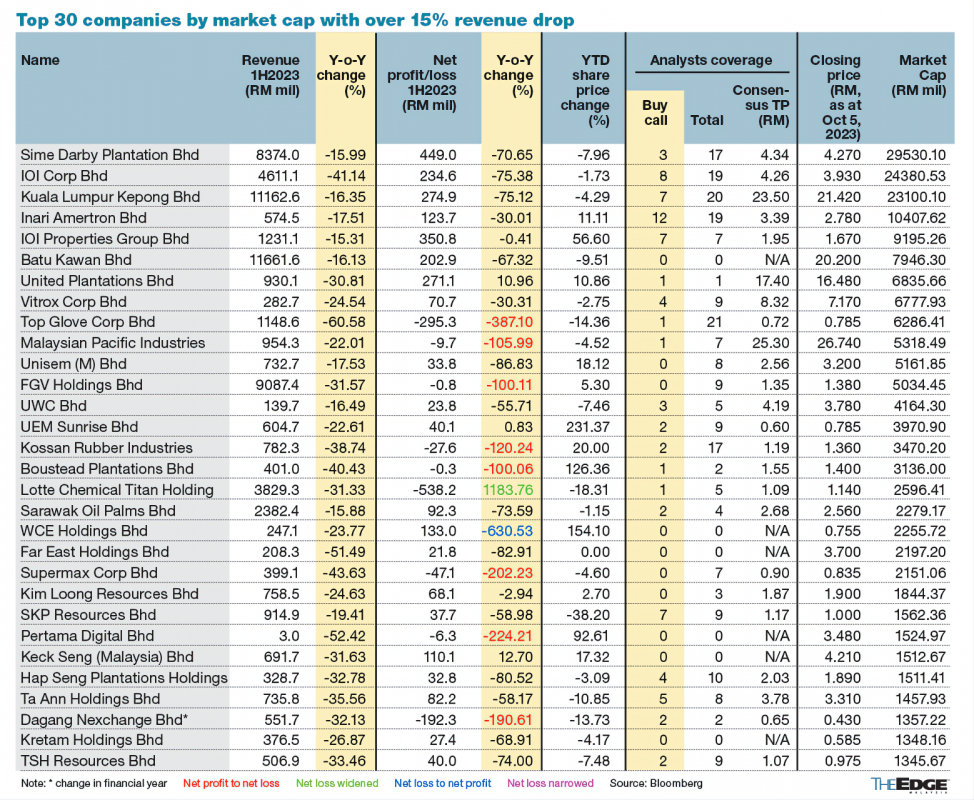

Among these 316 companies, 182 (excluding newly listed firms) saw their revenues fall by 15% or more.

Interestingly, the semiconductor sector that was adored by investors not too long ago appeared to be the worst performer in 1H2023, with many in the sector reporting both weaker revenues and profits, as slower demand continues to plague the industry.

A common refrain among the companies reporting their earnings is that the economic landscape has been challenging as rising inflation has taken a toll on business activities, thereby weighing on their performance for the first half of the year.

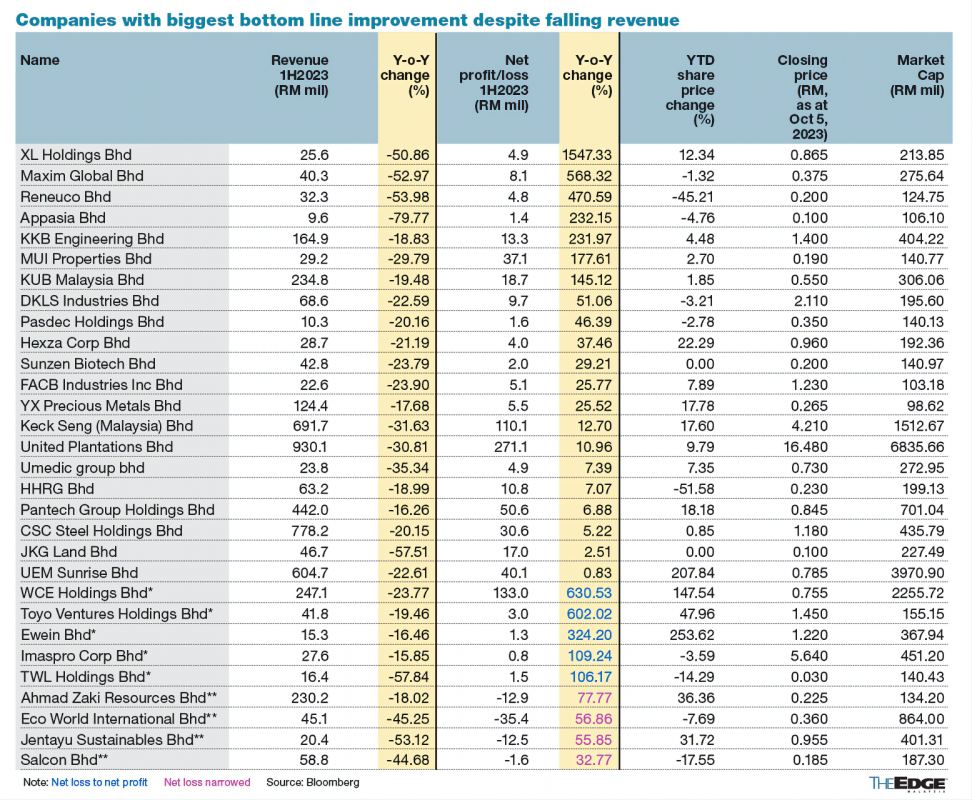

Still, 33 or 18% of those 182 companies managed to improve their bottom lines despite the revenue contraction, with disposal gains, higher foreign exchange (forex) gains and lower operating expenses among the reasons cited for the improvement.

Among these 33 are a few standouts that analysts still favour despite their falling revenues.

Falling revenues but better bottom lines

Sarawak-based KKB Engineering Bhd’s core business is in steel fabrication. For the six months ended June 30, 2023 (1HFY2023), KKB Engineering saw better contribution from its steel fabrication division, which aided the jump in its net profit to RM13.29 million from RM4 million previously.

The increase in net profit came despite revenue dropping 18.8% to RM164.86 million from RM203.1 million previously, due to lower revenue recognition from its civil construction division.

The 1HFY2023 net profit came within analysts’ expectation. In a note dated Aug 21, RHB Research maintained its 'buy' call on the counter and upped its target price to RM1.90 from RM1.80 previously, on the back of stronger earnings prospects for the second half of this year, backed by higher recognition of its engineering projects.

The research house also lifted its earnings forecast for the group for the financial year ending Dec 31, 2023 (FY2023) by 11% to RM28 million, and for FY2024 by 6% to RM32 million, and for FY2025 by 4% to RM36 million. KKB Engineering’s net profit came in at RM11.71 million for FY2022.

“A medium-term catalyst would be the rollout of the second phase of Sarawak Water Supply Grid Programme (SWP) in 1Q2024. KKB Engineering had secured RM200 million worth of jobs under the first phase of SWP,” it added.

According to Bloomberg, KKB Engineering’s 12-month consensus target price stood at RM1.74, implying an upside of 23% over its closing price of RM1.41 on Sept 27 (Wednesday). Year to date (YTD), the stock has risen by 5%.

Similarly, Pantech Group Holdings Bhd’s earnings have been resilient despite sliding revenue.

While revenue dropped 10% to RM244.77 million from RM270.68 million in the first quarter ended May 31, 2023 (1QFY2024), its net profit remained steady at RM26.98 million, compared with RM26.4 million previously.

Pantech, a specialist in the manufacturing and trading of pipes, valves and fittings and other components for the oil and gas sector, said its prospects will be backed by robust oil price as increased spending in facilities maintenance and upgrading activities in the oil and gas industry improve the demand for the group’s products in both domestic and international markets.

Notably, it declared its first interim dividend of 1.5 sen per share for FY2024, in conjunction with the release of its quarterly result.

In its FY2023 ended Feb 28, 2023, Pantech paid an annual dividend of six sen per share, which translated into a dividend yield of 6.8% based on its last closing price of 88.5 sen on Sept 27. This beat the 5.35% dividend declared by the Employees Provident Fund for its conventional savings' members in 2022.

In FY2022, it paid shareholders four sen worth of dividends, up from FY2021's 2.3 sen.

Over in the plantation sector, despite moderating crude palm oil (CPO) prices, United Plantations Bhd and Keck Seng (Malaysia) Bhd stood out among their peers as they bucked the trend of both declining revenues and net profits by recording improved net profits.

United Plantation’s cumulative net profit grew by 11% to RM271.11 million for the six months ended June 30, 2023 (1HFY2023) from RM244.33 million, lifted by higher other operating income, interest income, lower operating expenses and income tax expense. This was despite revenue shrinking 31% to RM930.06 million from RM1.34 billion.

As for Johor-based palm oil producer Keck Seng, its improved bottom line was due to its diversified business portfolio — which includes a hotel and resort division as well as a property development segment — which shielded the group from weak CPO prices, while higher forex gains added to earnings.

Keck Seng’s net profit rose 13% to RM110.11 million in the six months ended June 30, 2023 (1HFY2023), up from RM97.7 million a year before while revenue contracted 32% to RM691.66 million from RM1.01 billion.

In the property sector, developers UEM Sunrise Bhd and Eco World International Bhd (EWI) stood out for similar achivements, as higher forex gains and lower expenses cushioned their earnings.

It is worth nothing that RHB Research has a 'buy' call and a target price (TP) of 92 sen for UEM Sunrise as it believes the group remains the best proxy for the Johor thematic play and that it should benefit from greater commercial activities and population flow with more job opportunities expected to be created in Forest City in the future, given its sizeable exposure to the state’s property market.

Inari, IOI Corp have the most 'buy' calls

Among the 182 companies with significantly lower revenues (down 15% or more) and a market cap of at least RM100 million, Inari Amertron Bhd has the most number of 'buy' calls, a total of 12, with six 'hold' calls and one 'sell', and an average TP of RM3.39.

While some analysts are still rather pessimistic on the semiconductor sector’s near-term prospects due to ongoing demand weakness in consumer electronics that could pose downside risks to their earnings on top of unappealing valuations, Inari stood out with the dozen buy calls it has gained from analysts.

Inari’s average TP of RM3.39 implies an upside of 21.9%, based on its closing price of RM2.78 on Thursday.

TA Securities upgraded Inari to 'buy' from 'hold' with a higher TP of RM3.50 (from RM3.15 previously) on improved optimism on the group’s core radio frequency (RF) segment and the group's progress in some new projects.

TA Securities’ TP for Inari is based on a price-earnings (PE) multiple of 30 times, premised on its FY2024 earnings per share which is close to parity with the stock's five-year mean. It deemed this as fair, given Inari's growth prospects catalysed by the 5G theme, traction with customer diversification efforts, above-industry average profitability, expansion plans, and robust balance sheet.

Behind Inari in terms of the number of 'buy' calls is IOI Corp Bhd. IOI Corp has eight 'buy' calls, nine 'hold' calls and two 'sell' calls, with an average TP of RM4.26; its property arm IOI Properties Group Bhd has seven 'buy' calls, with an average TP of RM1.93.

IOI Properties’ average TPs stands at RM1.93, implying an upside of 16% compared to its closing price of RM1.67.

In its report dated Aug 29, TA Securities shared that the property sector is experiencing renewed investor optimism due to a number of factors, including the anticipated end of Bank Negara Malaysia's overnight policy rate hike cycle, potential land value enhancement from major infrastructure projects such as high speed rail, rapid transit system (RTS), the mass rapid transit line three (MRT3) as well as the establishment of special financial/economic zones and the possibility of homeownership-friendly policies.

This upbeat outlook is anticipated to continue, which could result in ongoing gains for property stocks, it said. As such, TA Securities upgraded its recommendation for IOI Properties to 'buy' from 'hold', with a higher TP of RM1.88, from RM1.19.

It may also come as a surprise that the plantation sector, which has been on a downtrend in line with weaker CPO prices, has received the most 'buy' calls from analysts.

Apart from IOI Corp Bhd, Kuala Lumpur Kepong Bhd got seven 'buy' calls with an average TP of RM23.5, followed by Ta Ann Holdings Bhd with five 'buys' and an average TP of RM3.78.

Hap Seng Plantations Holdings Bhd and Sime Darby Plantations Bhd follow close behind, with four 'buy' calls and three 'buy' calls, respectively. The average TPs for Hap Seng Plantations is RM2.03, while Sime Darby Plantations' is RM4.34.

The second half of this year (2H2023), outlook for the plantation sector should improve on the back of better output and lower unit costs, as well as benefits from firmer soy pricing, said MIDF Research analysts.

“Going forward, planters are hoping for volumes to pick up in 2H2023, on restocking and switching activities. CPO is now trading at a significant US$605/tonne discount to soybean oil, which should make palm oil products more attractive to buyers,” MIDF Research's report dated Sept 12 read.

The research house's top picks are IOI Corp, Ta Ann and Sarawak Oil Palms Bhd. It expects CPO prices to stay at RM3,900 per tonne for both 2023 and 2024, and to drop to RM3,800 for 2025.

Significant upside potential among the beaten down

Cold chain logistic company Tasco Bhd’s average TP is RM1.47, implying a huge upside of 84% over its closing price of 80 sen on Thursday. The stock has dropped 22% from this year’s peak of RM1.02 recorded in February. The stock has four 'buy' calls.

Among those with a 'buy' on Tasco is RHB Research, which is expecting stronger earnings quarters ahead for Tasco on improved trade activities amid global growth recovery in 2H2023. On top of that, it anticipates maiden contributions from Tasco's new warehouses, which would yield a better margin compared to its currently rented warehouse and provide the group with a lower effective tax rate.

In terms of valuation, the research house said Tasco’s current valuation of 7.34 times its price-earnings is well below local and regional peers’ average of 13 times and 19 times, respectively, which justifies the 'buy' call. It has pegged Tasco’s TP at RM1.70.

Dagang NeXchange Bhd (DNeX), whose stock has fallen 37.2% to 43 sen from this year’s peak of 68.5 sen in February, also offers substantial upside potential of over 50% based on its average TP of 65 sen. The stock has two 'buy' calls.

BIMB Securities Research is of the opinion that DNEX remains attractive given its long-term prospects as the group is set to ride on strong demand growth in semiconductors, leveraging on the potential of the new fabrication plant deal with iPhone's manufacturer Foxconn.

Electrical & electronics plastics contract manufacturer SKP Resources Bhd, whose share price has depreciated 35% YTD to RM1.04 on Sept 27, has seven 'buy' and two 'hold' calls from analysts, with an average TP of RM1.17.

TA Securities, in a note dated Aug 28, said it remained sanguine on the group’s medium-to-longer term prospects, supported by its customer's new model launches and product portfolio expansion, along with opportunities from the China Plus One strategy — a business strategy that encourages companies to diversify their operations by expanding outside of China while maintaining a presence in the country.

Source: TheEdge - 6 Oct 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

2024-07-22

DNEX2024-07-22

INARI2024-07-22

INARI2024-07-22

INARI2024-07-22

INARI2024-07-22

INARI2024-07-22

IOICORP2024-07-22

IOIPG2024-07-22

KLK2024-07-22

KSENG2024-07-22

SDG2024-07-22

SDG2024-07-22

UTDPLT2024-07-22

UTDPLT2024-07-22

UTDPLT2024-07-21

INARI2024-07-20

KLK2024-07-19

INARI2024-07-19

INARI2024-07-19

INARI2024-07-19

INARI2024-07-19

INARI2024-07-19

INARI2024-07-19

IOICORP2024-07-19

KLK2024-07-19

SDG2024-07-19

SDG2024-07-19

UEMS2024-07-19

UEMS2024-07-19

UEMS2024-07-19

UEMS2024-07-19

UEMS2024-07-19

UTDPLT2024-07-18

INARI2024-07-18

INARI2024-07-18

INARI2024-07-18

INARI2024-07-18

IOICORP2024-07-18

IOICORP2024-07-18

KLK2024-07-18

SDG2024-07-18

SDG2024-07-18

SDG2024-07-18

UTDPLT2024-07-18

UTDPLT2024-07-18

UTDPLT2024-07-17

DNEX2024-07-17

DNEX2024-07-17

DNEX2024-07-17

INARI2024-07-17

IOICORP2024-07-17

IOICORP2024-07-17

IOIPG2024-07-17

KLK2024-07-17

SDG2024-07-17

UTDPLT2024-07-17

UTDPLT2024-07-16

INARI2024-07-16

INARI2024-07-16

INARI2024-07-16

INARI2024-07-16

INARI2024-07-16

INARI2024-07-16

INARI2024-07-16

INARI2024-07-16

INARI2024-07-16

INARI2024-07-16

INARI2024-07-16

IOICORP2024-07-16

KLK2024-07-16

KLK2024-07-16

UTDPLT2024-07-16

UTDPLT2024-07-15

INARI2024-07-15

INARI2024-07-15

INARI2024-07-15

INARI2024-07-15

INARI2024-07-15

IOICORP2024-07-15

IOIPG2024-07-15

KLK2024-07-15

SDG2024-07-15

SDG2024-07-15

SDG2024-07-15

SDG2024-07-15

SDG2024-07-15

SDG2024-07-15

SDG2024-07-15

UTDPLT2024-07-15

UTDPLT2024-07-12

INARI2024-07-12

INARI2024-07-12

INARI2024-07-12

INARI2024-07-12

INARI2024-07-12

INARI2024-07-12

INARI2024-07-12

IOICORP2024-07-12

IOIPG2024-07-12

KLK2024-07-12

KLK2024-07-12

KLK2024-07-12

UTDPLT2024-07-12

UTDPLT2024-07-12

UTDPLT2024-07-11

KLK2024-07-11

UEMS2024-07-10

DNEX2024-07-10

IOICORP2024-07-10

IOIPG2024-07-09

IOICORP2024-07-09

KLK2024-07-09

SOP2024-07-09

TASCO2024-07-09

UEMSMore articles on CEO Morning Brief

Zafrul: Malaysia Aims for 5% Approved Investment Growth in 2024

Created by edgeinvest | Jul 19, 2024

U Mobile: No New Data Breach, Data Sample on Hacking Forum From 2014 Incident

Created by edgeinvest | Jul 19, 2024

Scoot Confirms Jet Operations Out of Subang Airport From September

Created by edgeinvest | Jul 19, 2024

AmanahRaya REIT Signs Alfa International College as New Tenant for Subang Jaya Property

Created by edgeinvest | Jul 19, 2024

Alpha IVF Set for Stronger Earnings, Current Valuations Unjustified — Analysts

Created by edgeinvest | Jul 19, 2024

Semicon and Tech-linked Stocks Fall on Fresh US Export Curb Jitters

Created by edgeinvest | Jul 19, 2024

High Court Sides With T7 Global's Unit in Dispute With Consortium Partner

Created by edgeinvest | Jul 19, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

https://dividendguy67.blogspot.com

2

save malaysia!

3

save malaysia!

4

save malaysia!

5

6

7

Good Articles to Share

Bill Gates on Elon Musk: I Hope He'll Talk More About Climate

8

Good Articles to Share

LGBTQ+ supporters march through far-right German town | REUTERS

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....