CEO Morning Brief

M'sian Automakers Expected to Feel Pinch From Lower Sales, Higher Costs, and Rise of Chinese OEMs

edgeinvest

Publish date: Thu, 25 Apr 2024, 09:33 AM

KUALA LUMPUR (April 24): Malaysian automotive companies may see earnings decline this year as sales dip and operating costs rise amid the emergence of several Chinese brands offering attractive pricing, analysts cautioned.

Vehicle sales may fall below the Malaysian Automotive Association’s estimate of 740,000 units this year, research houses including UOB Kay Hian, Hong Leong Investment Bank (HLIB) and Kenanga Investment Bank warned as they kept the sector on “neutral”.

“We maintain our conservative view on the sector, given the sector’s limited catalysts,” said UOB Kay Hian which is projecting sales of 660,000 units.

Consumer sentiment may be hit by lingering concerns over fuel subsidy rationalisation, the increase in sales tax and the impending luxury tax, the house said.

For HLIB, which expects total industry volume of 720,000 units this year, sales are expected to slow due to softening order backlogs while aggressive promotions by Chinese carmakers intensify competition for existing marques.

Kenanga, meanwhile, is forecasting sales of 710,000 units and noted that fuel subsidy rationalisation could dampen demand for mid-market car models as the middle 40% household income group may delay purchasing new vehicles or opt for smaller cars to reduce fuel expenses.

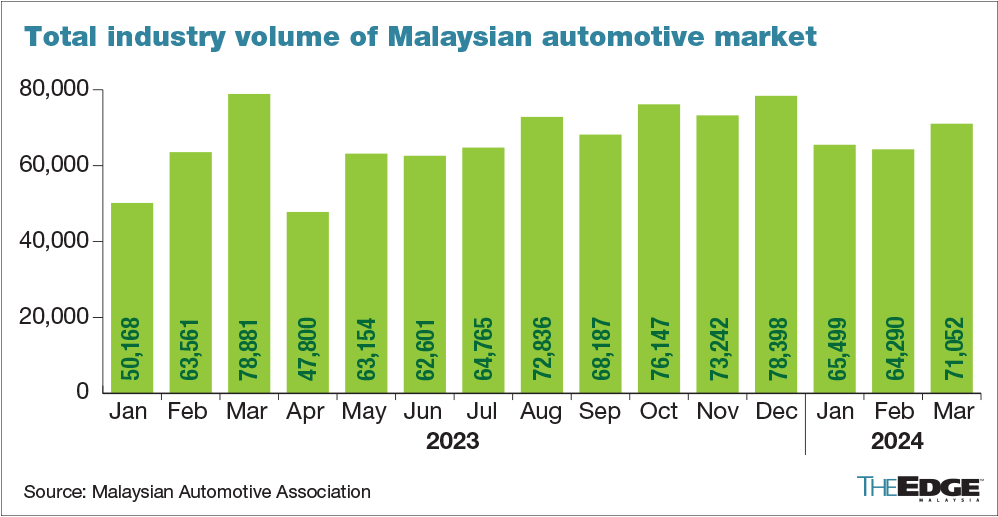

The comments follow the latest data showing a near 10% year-on-year decline in vehicle sales in March.

At 71,052 units, the total industry volume was 10.5% higher when compared to February, thanks to a delivery rush by companies with financial years ending on March 31 and Hari Raya campaigns.

To reduce its fiscal deficit, the government plans to remove the RON95 fuel subsidy, which contributed significantly to the previous year's RM81 billion subsidy expenditure.

Even with subsidy rationalisation challenges, Kenanga and HLIB see a possibility of growth from 2024's new model launches, with proactive sales and marketing efforts expected to maintain manufacturer sales.

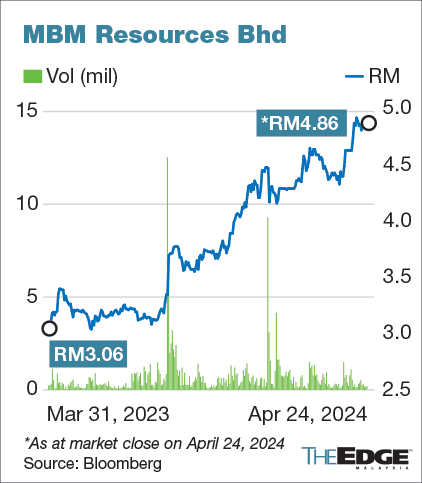

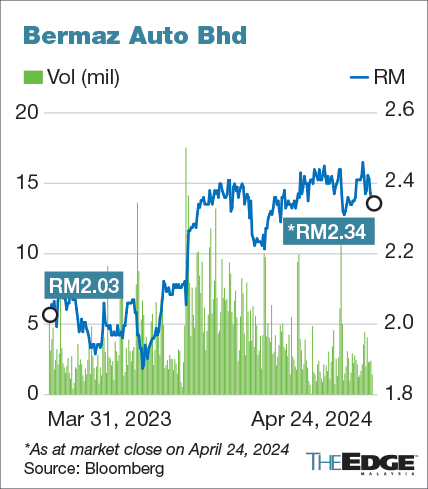

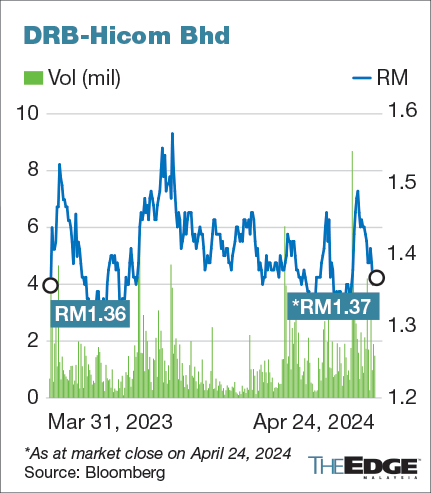

Top picks are MBM Resources Bhd and DRB-Hicom Bhd for their strong leverage of national brands like Proton and Perodua, benefiting from more stable sales volumes and potential long-term growth through exports.

Shares in MBM Resources hit a record high of RM4.95 earlier this month and have gained 16% so far this year, valuing the company at RM1.90 billion. DRB-Hicom is valued at RM2.65 billion after a 1.43% year-to-date loss.

There are four “buy”, six “hold” and one “sell” calls on MBM Resources, with a 12-month target price (TP) of RM4.60, according to Bloomberg, and two “buy” and two “hold” ratings for DRB-Hicom with a 12-month TP of RM1.70.

Source: TheEdge - 25 Apr 2024

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on CEO Morning Brief

KNM Explores Fresh Options to Sell Italian Unit After Another Failed Attempt

Created by edgeinvest | Jul 03, 2024

Jamaludin Jarjis' Asset Dispute Trial Put on Hold as Family to Discuss 'serious Settlement”

Created by edgeinvest | Jul 03, 2024

Bar Says It Is Challenging Pardon’s Board’s Decision in Najib’s Case, Not Agong’s Power

Created by edgeinvest | Jul 03, 2024

Najib Allowed to Intervene in Malaysian Bar's Challenge of Pardons Board's Decision

Created by edgeinvest | Jul 03, 2024

Malton Buying Land in Genting Highlands to Build Apartments, Luxury Villas

Created by edgeinvest | Jul 03, 2024

Selangor Records 25.9% Contribution to 2023 National GDP — DOSM

Created by edgeinvest | Jul 03, 2024

Apex Court Grants Leave for Govt to Challenge Pre-2015 Lawmakers' Pension Payment

Created by edgeinvest | Jul 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Latest Videos

Apps

Top Articles

1

2

AmInvest Research Reports

3

How to become a resilient trader

4

TA Sector Research

5

6

TradeMasterT

7

8

save malaysia!

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....