HLBank Research Highlights

Traders Brief - Bearish Sentiment Amid Hawkish Fed and Potential US Hard Landing

MARKET REVIEW

Asia/US. Tracking overnight fall on Wall St and ahead of the policy decisions from the ECB and BOE, Asian markets slid following Powell’s hawkish remarks, dispelling hopes for a rate cut next year despite signs of an imminent recession. Sentiment was also dampened by China’s sluggish November retail sales and industrial production reports coupled with skyrocketing Covid cases. The Dow extended its rout (-764 pts to 33,202) as downbeat retail sales and manufacturing coupled with a hawkish Fed intensified the risk of a US hard landing.

Malaysia. Tracking regional markets’ slump, KLCI tumbled 16 pts to end at 1,467.1, led by selling pressures on telcos (after the government in talks with MCMC & telcos on cheaper services) and banking (amid the hawkish Fed) stocks. Local institutions continued its buying spree for the 12th consecutive session (+RM135m; Dec: +RM1.23bn) followed by retailers (+RM44m; Dec: -RM40m) whilst foreigners resumed their net outflows (-RM179m; Dec: -RM1.19bn).

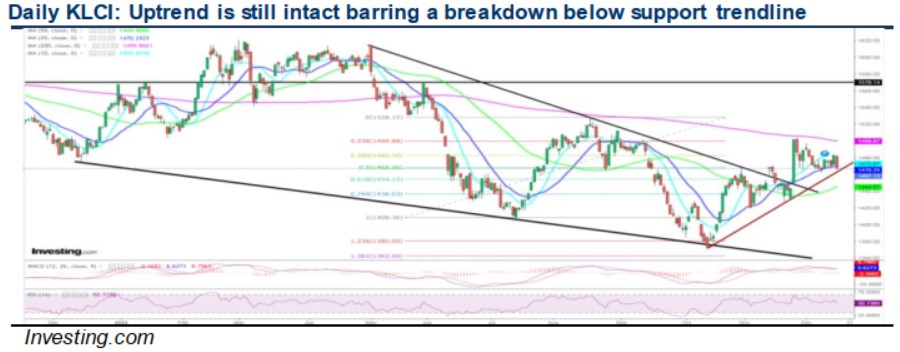

TECHNICAL OUTLOOK: KLCI

Following the bearish engulfing candlestick yesterday, the benchmark may consolidate lower in line with overnight Wall St rout. A decisive breakdown below the support trend line (from 2Y low of 1,373) may trigger further selloff towards 1,454 (61.8% FR) and 1,436 (76.4% FR) zones. Stiff resistances are situated at 1,482-1,500-1,528 levels.

MARKET OUTLOOK

In sync with the overnight Wall St slide, KLCI could experience an extended selloff today amid hawkish Fed and potential US hard landing. However, the fall could be cushioned near 1,436-1,454 support levels as investors look forward to i) more reform policies from the unity government, ii) further relaxations of China’s zero Covid curbs, iii) strengthening political stability as a coalition agreement involving all parties in the unity Government will be signed today, and iv) year-end window dressing in Dec (10Y/20Y: +2.6%/2.8%). DNEX (HLIB-BUY-TP RM0.93) could experience further selldown following another arbitration involving CGP, with major supports situated at 0.40-0.455-0.50 levels. Any oversold rebound is likely to be capped at RM0.55-0.58-0.62 zones.

Source: Hong Leong Investment Bank Research - 16 Dec 2022

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on HLBank Research Highlights

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Apps

Top Articles

1

2

Kenanga Research & Investment

3

4

6

https://dividendguy67.blogspot.com

7

BFM Podcast

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....