Good Articles to Share

Investor, Pay Attention Investor, Pay Attention - Vishal Khandelwal

July 6, 2015 by

Note: This is an except from the article Where Do Great (Investment) Ideas Come From, which I wrote for the May 2015 issue of our premium newsletter, Value Investing Almanack.

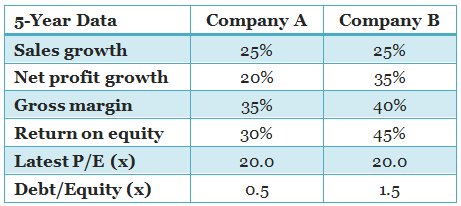

Consider that you are looking to buy a stock and the two that you come across on your screen are, say, Company A and Company B. Here are a few data points about the two companies, which are the only factors you would look at while making your decision. Look at them and think which one you would rather purchase –

Did you make a decision? Before you read on, jot down either Company A or Company B. Now I’m going to give you some more data points on these companies. No information has been changed, but some has been added.

Which stock would you rather purchase now? Again, write down your answer. I’m going to present the options a third time, again adding one new element.

Now, which of the two would you prefer?

Chances are, somewhere between the second and third lists of data, you switched your allegiance from Company B to Company A. And yet the two companies didn’t change in the least. All that did was the information that you were aware of.

This is known as omission neglect. We fail to note what we do not perceive up front, and we fail to inquire further or to take the missing pieces into account as we make our decision.

Some information is always available, but some is always silent – and it will remain silent unless we actively stir it up. In investing, such information that remains silent – or that you fail to notice – can be dangerous to your capital.

Consider my experience with the stock of Hotel Leela. I was in Bangalore sometime in early 2006 and visited Leela Palace to meet a friend who was attending a conference there. I was in awe of the property – it was grand, and amazingly beautiful.

On enquiring, I got to know that the hotel was one of the most expensive locations in India and was completely booked for the next few months.

The story was same everywhere – most of Leela’s properties were booked for months, despite their premium pricing.

“What an amazing business!” I told myself. “Just imagine the kind of profits these guys must be making. I must have this stock in my portfolio!”

The next day, without enquiring more about Leela’s business and financial performance, I bought the stock, expecting it to be a story that was waiting to be unveiled. My premise was – Great hotel + Premium pricing + Overbooked = Great profits.

Well, it was indeed a story waiting to be unveiled…and for me! When I glanced through the company’s annual reports after buying its stock, I saw a business that was badly managed.

The debt/equity was rising, much more cash was burned than was generated, return ratios were average at best, and the profit growth had followed a highly inconsistent path. As I included more information on the company in my analysis, I started ruing my decision to buy the stock more.

Anyways, by the time I had realized and then accepted my mistake, the stock was already down around 45% from my purchase price. But I still sold it off. And thankfully so, as the company remains in doldrums and so does the stock.

Now, my idea is not to lead you to conclude that you need to gather a world of information on a business while doing its analysis (in fact, the first 20% information will tell you 80% about the business), but it’s important to pay attention and include the most important information while doing your analysis.

Don’t suffer from inattention blindness bias, as shown in this invisible gorilla experiment.

To pay attention means to pay attention to it all, to engage actively, to take everything around us, including those things that don’t appear when they rightly should. It means asking important questions (like some I listed earlier in this post) and making sure we get answers.

Even when you do this, you may not be able to emerge with the entire situation in hand, and you may end up making a choice that, upon further reflection, is not the right one after all. But it won’t be for the lack of trying.

One of the biggest lessons I learned while reading this wonderful book from Peter Bevelin, A Few Lessons from Sherlock Holmes, was that, while analyzing situations, it’s important to not jump to conclusions and instead try to collect facts as open-minded as possible.

As Mr. Bevelin quotes Sherlock Holmes…

No one can give rules for methods of thinking but it is possible to carry certain principles into operation. One is to strive to be delivered from hasty judgments.

“Men see a little, presume a good deal, and so jump to the conclusion.”

How common this is needs only a little study of our mental processes. In some this is a habit, in others a fault of education.

So the takeaway for you is to observe to the best of your abilities and never assume anything, including that absence is the same as nothing.

http://www.safalniveshak.com/investor-pay-attention/

More articles on Good Articles to Share

Hyman: The best thing investors have going for them right now is bonds aren't broken anymore

Created by Tan KW | Aug 16, 2024

Why Goldman Sachs is jumping headfirst into crypto while rivals retreat

Created by Tan KW | Aug 16, 2024

What Walmart's results and the July retail sales data says about the state of the consumer

Created by Tan KW | Aug 16, 2024

Veru: The biggest risk for the markets is to focus on just one data point

Created by Tan KW | Aug 16, 2024

Casey: The Harris campaign has an opportunity to reset the narrative on the economy

Created by Tan KW | Aug 16, 2024

Discussions

Be the first to like this. Showing 4 of 4 comments

The truth is, none of the information is useful for predicting the future. I will rather focus on what the companies have or planning to do, that kind of thing. The future is the more important one. Even a company with a minus 25% sales growth is worth to be bought if they have someone that everyone would want in the future.

We only look at the ratios etc to gauge the survivability of the company for the period we want to lock our funds. That's about it.

2015-07-07 13:50

Post a Comment

Featured Posts

Latest Videos

.png)

.png)

Apps

Top Articles

1

Good Articles to Share

2

Good Articles to Share

3

save malaysia!

4

Mercury Securities Research

5

6

save malaysia!

7

Koon Yew Yin's Blog

8

https://dividendguy67.blogspot.com

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

YourMotherInLaw

i saw the gorilla and also counted it correctly lol.. the gorilla is so obvious @_@

2015-07-06 14:49