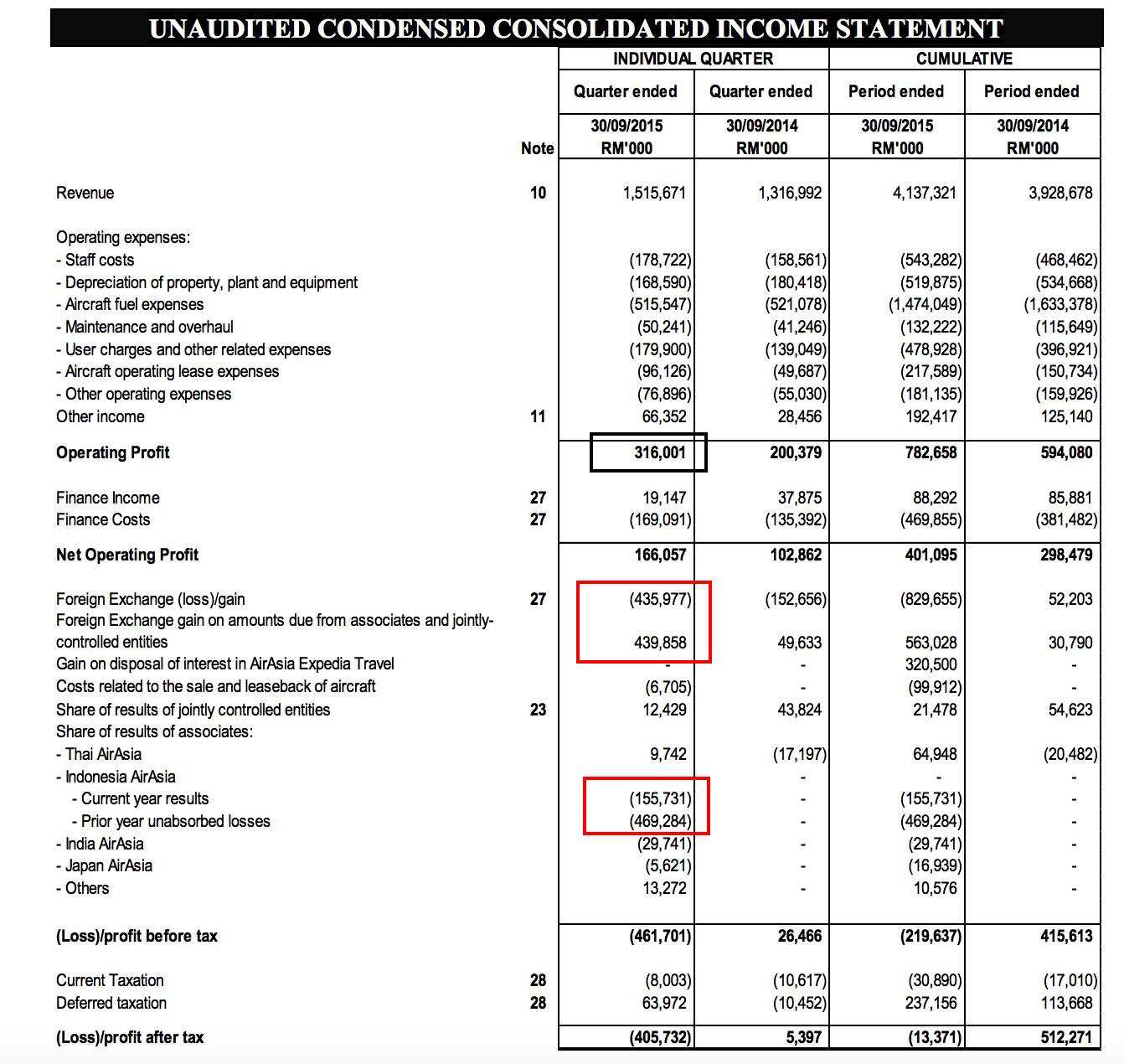

Anyone that has a quick look at the results would be shocked as it reported a net loss of RM406 million. However, before one trembles, take a look at what caused these losses. It absorbed RM625 million in losses mainly due to the conversion of Indonesia Airasia's owings into shares - to reverse the negative shareholders funds as required by the regulators in Indonesia. This shall I say is already expected and announced.

|

| 3Q15 Income Statement |

What's key in the results

One of the things that's noticeable is the challenges it faces in the newer markets that it has gone to - Indonesia, Philippines and India. As a result, do not expect these new ventures especially India and Japan to be profitable fast.

Airasia has also started to publish results for all its markets and provide its consolidated report. Notice the low right number of RM64.91 million...That's consolidated number in the event it is assumed as it has control over those companies.

Another point to note is that with oil price at around USD42- 45 per barrel, there is still room for Airasia to enjoy better margin due to low fuel price. For the quarter, its average price was USD77. I would expect it to be below USD 60 by 2016. Most airlines have hedged a significant part of their fuel causing them to still buy fuel at higher than spot prices. Most of them has lessen their hedges for 2016. (Notice that fuel still comprise of 38% of the total costs, hence making it the single highest costs element for Airasia and in fact for all other airlines)

All in all, while most may just be looking for a single headline, as shown below, if we look deeper, there are many positives especially for one of the largest airline in Asia and with such a deep discounted price.

|

| Flash headline via TheEdgedaily |

Mat Cendana

Reasonable analysis here. Much better than The Edge's and the media's interpretation of the results.

2015-11-28 01:53