Stocks market watch

Will Canone have same fate as Focus Lumber? Prominent investor buy and you also buy

If you noticed that Canone has been on the declining mode since last week. Those smarter investor may have already unload their holding slowly anticipating of poor result. As seen from Focus Lumber today, it is the biggest loser lost 11% of its value in just a day.

Canone quarter one of 2016 financial result will be announced soon anytime this week. Any weak earnings will just push Canone share lower and probably gap down to RM3.50. If broken, it may fall to RM3.00. This shares has been on speculating side since last year when prominent investor promoting it and acquired huge amount of Canone shares which cause the share price to spike up to RM4.40 on mid April 2016 as so many follow his foot steps. No wonder this prominent investor can proudly claimed this share increase more than 100%.

This prominent investor said the shares is undervalued. While an article by Focus Malaysia this week saying that the F&B Nutrition in Canone is overvalued when KWAP trying to acquire 30% stake for RM280 million. Then who is right now? I would think KWAP will be wasting money and jeopadising pension fund by paying much more than they should. KWAP should put public interest first and probably negotiate to get better price or walk away as these parties have intention to make big bucks in a short period of time. It has been years of selling this and that. Might as well sell off everything and don't need to do business. If you follow Kian Joo recent quarterly financial result, its down half than the previous quarter and may not contribute that much to Canone. So you will see weaker earning for Canone this coming quarter one of 2016 financial results. Any companies that being fakely push up and missed earning estimate will have huge gap down on the next day. Usually this gap down will be continuous for 2 days before stablise to lower fair value level. Be safe and make proper research before investing your hard earned money. Think twice of prominent investor statement.

News article from Focus Malaysia. They said overpriced.

Prominent investor claimed undervalued.

As of now Canone at RM3.80. Continous down trend. Maybe bad result ahead? Are you willing to wait for quarterly result to have gap down?

Take a look at recent Kian Joo financial result. Down 50% compared to the previous quarter. No wonder keeps dropping also. Less speculation so it will drop slowly without huge gap down although missed earning expectation.

If you remember. Canone drop by 6% during the last quarter as the result missed earning expectation.

Shot up to RM4.40 when this prominent investor acquired 15 million shares. All the followers just enriching him.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Stocks market watch

Prominent investor buy call analysis - Gadang, Liihen, Focus Lumber and XingQuan example

Created by ah_boon | Aug 14, 2016

Gadang - Prominent investor asking you to chase high again. For him to sell?

Created by ah_boon | Aug 11, 2016

Liihen - Prominent investor ask you to chase high. Will you follow his advice?

Created by ah_boon | Jun 05, 2016

Prominent investor now using Facebook to share his advice and hinting Liihen at high price

Created by ah_boon | Jun 04, 2016

Follow blindly when prominent investor buy. What will happen to Focus Lumber on monday?

Created by ah_boon | May 21, 2016

Do you think these shares will rise so much if prominent investor don't promote it?

Created by ah_boon | May 07, 2016

Untimely disclosures and secretive actions by prominent investor - A challenge to Bursa?

Created by ah_boon | May 07, 2016

Discussions

3 people like this. Showing 44 of 44 comments

ah_boon...give you like for the investigative style report...though i see zero solid evidence so far...he he

perhaps if results truly bad - then may be can consider giving FBI badge...lol!

2016-05-24 00:51

I believe any are gunning down Mr. Koon Yew Yin after the apparent dsmal performances recorded in Focus Lumber, VS ad a few other counters which he promoted recently. Canone is the target now. Do you think Canone will suffer the same fate like Focus Lumber? My take is no is you look at Johore Tin at the moment. Koon Yew Yin is holding 15 million shares and it may take him a while to sell them off.

2016-05-24 09:16

In all fairness, and im not siding anyone, how can anyone correlate the relationship between an increase in the share price with KYY's promotion? How would you know how many people actually bought the share because theyve read it from KYY blog or from i3? The fact is you can't tell. Just because the opinion is strong that it is doesn't mean it is true because it is something you can never prove.

2016-05-24 09:57

Please explain the increase of share price after 11 April after substantial buy announcement.

2016-05-24 10:00

Well, we have to reconcile with the fact that KYY kept promoting several counters in his after buying them. For example, Xingquan, R. Sawit, Ta Ann, Evergreen, Focus Lumber, VS, Canone, LiHen and the list goes on. Many would tend to follow simply because they felt that KYY is rich and made his millions through stocks. This is a remark of his own. Many would tend to follow him simply because he confessed that the millions he made from stocks are given to charity and sponsorships. But these fans are changing to be his haters. These fans lost money in those stocks mentioned. Xingquan for example has went down from RM1.60 to RM0.28. What if you have invested RM10,000 of your RM20,000 savings in Xingquan? What about R. Sawit? But I have confident in Canone as the numbers are churning out to be good. Having said that, Xingquan churns out the good number too.

2016-05-24 10:28

cariyoyo: If you brought cheap then should be alright. Anyway, its your decision if you want to continue to hold based on the prominent investor action.

2016-05-24 10:32

Good investigative analyst would already detected that Kian Joo results is dragged down by unrealized forex losses of RM22 million. The term unrealized means that it can turn the other way round next quarter if RM continues to weaken like what we see today. It can also turn worse if RM strengthen further below 3.9 (closing rate at 31 March).

I would not bet against another record breaking year after looking at good revenue and gross profit growth for Kian Joo.

2016-05-24 10:36

Funny thing is the price tag of F&B is not given by Can1, but by the buyer. It is funny because Can1 should be the one who is eager to announce rather than potential buyer. So to say that F&B is overpriced when buyer is the one announcing it, I just cant comprehend.

By the way, F&B counters are priced at that kind of PE.

2016-05-24 10:38

ah koon sell 20 buy 10 lots tactics to dispose,so in the end he manage to sell while others thought of tecnical rebound left stuck

2016-05-24 11:34

ah_boon, you say falling knife, some will say buying opportunity....i guess this is how market works, else got seller no buyer, where got fun...lol

Anyhow, after reading the above article, cant help but notice that there is no analysis at all. If you say too pricy, what is the basis?

Just because Focus say F&B overpriced, suddenly it becomes gloomy? Anyhow, Can1 did not say it is selling F&B. I find it funny that people want to buy at an overpriced value and Can1 dont seems to be accepting the offer. Hehehe

2016-05-24 16:06

Haha, Ah Boon enjoyed more on whacking the old man than doing analysis on stock

2016-05-24 16:43

You probably think what you do (personal attack) is right. Please walk, eat & drive carefully. Good luck

2016-05-24 21:59

This is not personal attack. It's just a matter of fact. Who ask this prominent investor to encourage margin financing to buy stocks. Misleading people for to enrich himself so that he can give charity.

2016-05-24 22:04

For the supporters of this prominent investor he or she must believe on his Trait no 7. According to him, this is the the most important, and rarest, trait of all is the ability to live through price volatility and fluctuation without changing your logical thinking process. So whatever I write here should not change your mind and you should continue to hold on. Don't be scared.

2016-05-24 22:20

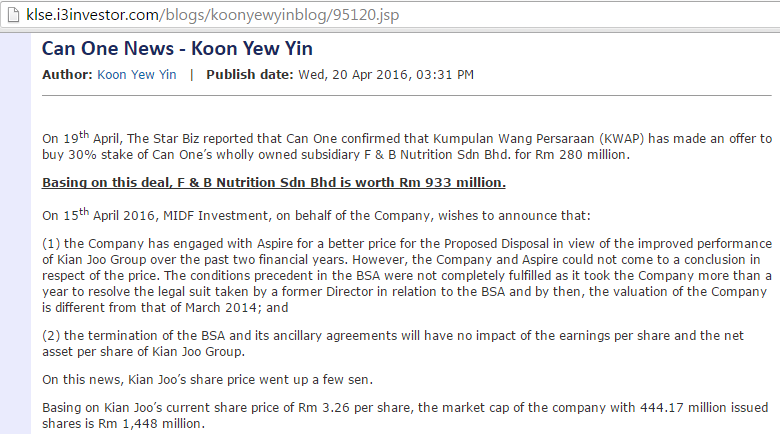

I agree with this article……

According to our prominent tycoon aka prominent investor, in his latest blog on canone, he says… The whole market capitalization of Can One is only 192.15 million issued X Rm 4.06 = Rm 780 million. It is so much undervalued, according to him….

http://klse.i3investor.com/blogs/koonyewyinblog/95120.jsp

How can someone with that state of minds can says Rm 4.06 is undervalued stock??? It is really outrageous crazy….For smart conservative investor like us, every undervalued stock, need to have margin of safety when we buy stock with good fundamental ….I can’t find any margin of safety on canone at the current price…… it is overvalued price……Unless, those who willing take risk, then go ahead……

ah_boon…. thank you for reporting the truth….

2016-05-24 22:41

Rencana ini banyak memberi manfaat kepada kita orang…..terutamanya kepada mereka yang masih baru dalam pasaran saham….

“Don’t shoot the messenger”....we should embrace and learn from one another….

Eventhough we are technically very experienced investor here, but we can’t run away from the facts…

With someone like ah_boon teaching us, we should be able to detect any share price irregularity movement next time....it is great, you keep on sharing with us your knowledge……

2016-05-24 23:18

Nampaknya kyy blog sekarang sudah boleh buat komen…… dia rasa bersalah agaknya…

Tapi sekarang dia nak mempromosi FLBHD pula…. Towkay koon, tak cukup kaya???... tak apalah…. Janji dapat pancing banyak ikan masuk sangkar…..terima kasih..…kerana sokongan kamu… hehehe….. http://klse.i3investor.com/blogs/kcchongnz/97079.jsp

2016-05-24 23:40

@malaysiaku mana boleh komen. Blog rasmi kat sini http://klse.i3investor.com/blogs/koonyewyinblog/blidx.jsp Itu towkey diktator. Tak bagi komen. Dia tahu banyak ulasan dalam blog yang dia tak mahu ambil tahu. Semuanya dia yang betul. Umur sudah lanjut tapi masih lagi nak mempromosi saham dan memerangkap mereka yang masih baru dalam pasaran saham. Dunia ini tiada yang percuma dan penuh dengan muslihat.

2016-05-24 23:55

@very_goat this post is totally not related to Canone or Focus Lumber. Although it related to this prominent investor of VS but he has sold off much of VS shares. These Dyson products although looks cool and useful but it's so expensive and not many can afford to buy it. In my opinion, these Dyson products is just a temporary hype and not sustainable.

2016-05-25 21:32

ah_boon...u need to comment on Canone results...

cannot escape without a proper conclusion

2016-05-25 21:39

Canone result already out and as expected the earning deteoriating. See whether RM3.50 support well tomorrow or else it will head towards RM3.00. Since today is RM3.63 as it already drop so much since last week, even if gap down to RM3.50, it's just a 3.5% down. Usually gap down will cause at least 5% drop and may broken the RM3.50 support.

2016-05-25 21:52

Also to add another point, Kian Joo being sued again. Haih... So much drama in these two counters. One always being sued while another one want to sell this and that.

2016-05-25 21:55

when u see Koon buy.....u better sell. cos when he sell, he wont tell u. so better sell before Koon sell.

2016-05-26 09:19

ah_boon, really disappointed reading your last comment. Very clearly you are just interested in hammering people without checking the facts. Yesterday's announcement was an update on existing law suit and NOT as what you have stated...."being sued again".

Also never in any Can-1 announcement they say they want to sell anything. In fact if KWAP have offered to buy 30% FNB at RM280m which people perceived as overpriced and they say they are not selling, I just wonder where you get the impression they want to sell this and that.

I suggest you take a closer look at the numbers rather than making misleading statements. If you need to calculate FNB value, there are good data available publicly:

1. Johotin acquisition of Able Dairies few years back

2. Sale of Etika Dairies to Japanese group 3 years back

3. Current trading PE of food counters such as FNN, Dutch Ladies, Nestle and discount it

2016-05-26 09:25

Actually bulk of the drop is from share of results from associated company and tax. Actual business results has maintained.

2016-05-26 09:26

Small shareholders if they sell at this price will only benefit the big sharks who can pick the share up on the cheap. I believe this counter have more value than you can imagine.

2016-05-26 09:31

@mccheat Don't scare. Buy more if you are so confident. Maybe you will be rewarded later. Being sued or not, the fact is Kian Joo has so many legal tussel before. PE level is not the main criteria. What's the point to have high PE level if the company no longer capable of producing increasing profit.

2016-05-26 16:09

ah_boon, that's why I say you like to shoot when you see shadow...lol. Absolutely no regard to fats...oops facts.

1. Since 2011, there were only 2 legal cases. First case when See family wants to stop Aspire deal. Second case when the other see family sue the company for retirement benefit and lost of salary (until he reaches 70 years old - could you believe it?). There are not many legal tussles. And those are not threatening the business.

2. Kian Joo has announced a drop in profit but if you read the notes, you will noticed that unrealized loss is RM22 million. If you take that out, the profit is actually up and impressive too. Why unrealized loss? That is something I will find out.

2016-05-26 21:21

F&B had been growing steadily since Can1 acquired it, if you care to look deeper into it.

2016-05-27 09:19

Revenue/segment profit are RM137.6M/RM4.3M in FY2009, RM220.0M/RM10.9M in FY2010 to RM562.2M/RM48.7M in FY2014 to RM533.0M/RM59.0M in FY2015. PAT for FY2014 was RM36.1M and FY2015 was RM45.5M.

2016-05-27 09:19

2015Q1 - RM123.9M / RM11.0M

2016Q1 - RM133.2M / RM15.5M

Did not see growth in F&B so cannot justify high PE? Hmmmm...

2016-05-27 09:19

When Johotin bought Able Dairies a few years back, it was at 15.5 times PE. At this PE, F&B will be worth RM705M

2016-05-27 09:20

When Asahi acquired Etika Dairies in 2014, the purchase price was at USD328,787,704 when its PAT was at RM29.4 million, about 65% of F&B's PAT in 2015. The PE? A whopping 36.08 times. At this PE, F&B will be worth a whopping RM1.7 billion.

2016-05-27 09:20

@mcheat maybe you should create a blog post to mention about Canone advantages.

2016-05-27 16:02

It is of interest to me a novice investor in the stock market. I myself am an investor in ihsg as an Indonesian exchange.

I also wrote an article related to stock investing at https://www.dompetinvestasi.com

2022-10-16 20:13

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-17 09:30:00

TURTLE SYSTEM 20

30 Mins

BUY

Apps

Top Articles

1

南洋行家论股

2

BreakingOut

3

Koon Yew Yin's Blog

4

Bursa Stock Musings - Thoughts & Ideas

PGF Capital - insti shareholding up from 5% to 14%! (part 1)

5

The Alpha Trader

6

南洋行家论股

7

How to become a resilient trader

8

RHB Investment Research Reports

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

moneySIFU

Good job, all supported with facts & traceable sources.

Years already hearing selling this selling that, another real story of wolk's coming

2016-05-24 00:49