Stock Pick Contest Year 2021

A look back at the 11 stocks experts said you should own in 2021 - The Edge

Stock Pick Contest Year 2022 - How it works? (Please submit after 31-Dec-2021 4:50pm)

KUALA LUMPUR (Dec 30): At the start of 2021, The Edge highlighted 11 stocks that fund managers and analysts picked for 2021, as the availability of vaccines then raised optimism for a better year ahead.

However, what actually came was even more volatility as the strictest lockdown measures were reintroduced as Covid-19 cases surged amid the emergence of the more deadly and fast-spreading Delta variant, further supply chain disruptions globally that affected business recoveries, while labour issues shadowed some major companies listed on Bursa Malaysia, from glove makers to plantation giants.

On top of these, there were more political uncertainties at home as Tan Sri Muhyiddin Yassin lost his precarious grip on power when some allied lawmakers withdrew support, causing the then prime minister to resign, ending a tumultuous 17 months in office. He was then replaced by Datuk Seri Ismail Yaakob, which signaled the return of Umno to power.

And as the end of 2021 drew nearer, the markets were weighed down by the discovery of another new Covid-19 variant, the Omicron, and then shaken further by the most catastrophic floods the country had seen in recent years.

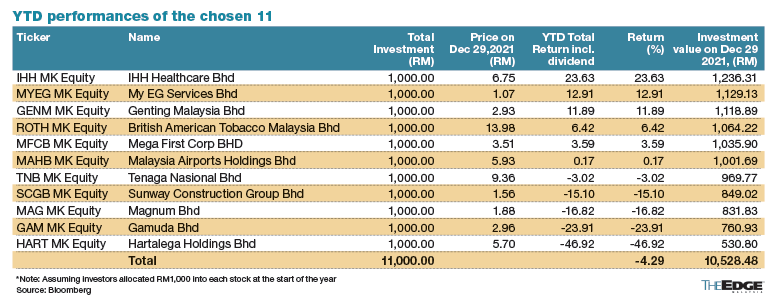

Hence, not surprisingly, the 11 stocks generated a return of -4.29% year-to-date (YTD), though still outperforming the FBM KLCI's -5.05%. Six of the 11 recorded gains, while five are in the red and likely to remain so, with only two trading days remaining before 2021 ends.

Among the losers, Hartalega Holdings Bhd topped the list amid concerns over mounting pressure on glove selling prices and overcapacity. In contrast, hospital operator IHH Healthcare Bhd was the top gainer, as it proved the resilience of its business despite the prevailing market turmoil.

IHH Healthcare Bhd

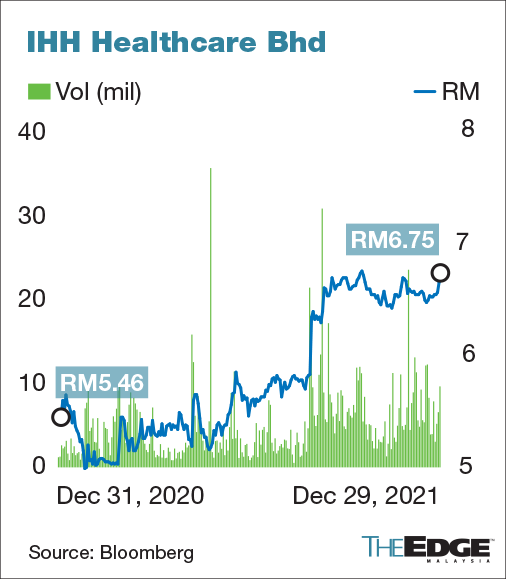

IHH Healthcare Bhd, which has been touted as a proxy for regional recovery from the Covid-19 pandemic, outperformed the FBM KLCI, as its share price rallied 22.7% from RM5.50 on Dec 31, 2020, to close at RM6.75 on Dec 29. Two months earlier on Oct 15, the stock hit an all-time high of RM6.87.

Notwithstanding the rally, RHB Research analyst Sean Chew believes IHH’s valuations remain undemanding. Chew, who has maintained “overweight” on IHH and upped his target price (TP) to RM7.35 from RM6.80, said in a note dated Dec 22 that the healthcare stocks under his coverage such as IHH have further room to run, premised upon new growth drivers and structurally higher cost of care.

IHH is his top pick stock owing to the group’s defensive demand, with diversified presence and anticipated operational recovery from its lagging markets such as Malaysia and Singapore. Beyond recovery, he believes there could be additional upside (not captured in his TP) from management’s restructuring efforts that will boost IHH's return on equity (ROE)-enhancing strategy.

IHH returned to the black with a net profit of RM1.41 billion for the nine months ended Sept 30, 2021, from a net loss of RM130.48 million for the corresponding period last year, as revenue grew 31.3% to RM12.66 billion from RM9.64 billion. The healthcare group's earnings growth for FY2022 and FY2023 is anticipated to be propelled by bed occupancy rate (BOR) recovery in Malaysia and Singapore, while its Turkey operations could likely continue to benefit from strong medical tourism activities.

Among 20 analysts covering the stock tracked by Bloomberg, 16 had it on “buy” while four had it on “hold”, with TPs in the range of RM5.83 to RM10. — by Justin Lim

Tenaga Nasional Bhd

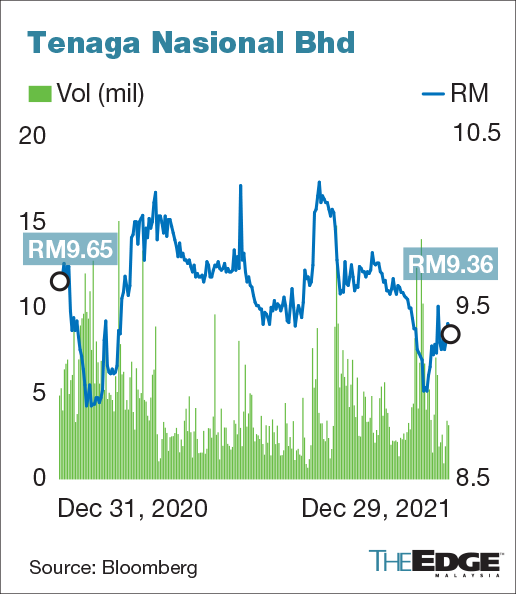

2019 was a bad year for Tenaga Nasional Bhd, in terms of share price performance despite the bumper dividend. While analysts saw values emerging as the stock price slid to a multi-year low, Tenaga’s share price continued to drift lower in 2020, although the fall was smaller.

Environmental, social and governance (ESG) concern has been the main factor that kept investors at bay.

Since the start of the year, Tenaga’s share price has slipped 6.7% YTD to close at RM9.36 as at Dec 29. It climbed to a year’s high of RM10.92 on March 29, and soon after, it embarked on a downward trend to a year’s low of RM9.02 on Dec 6 and Dec 8.

Earnings wise, the utility giant fared well in the first nine months ended Sept 30. Its net profit expanded nearly 17% to RM2.78 billion in the nine-month period from RM2.38 billion a year ago, while revenue increased 9.64% to RM36.89 billion from RM33.65 billion. Furthermore, it declared the same amount of dividend per share of 22 sen as last year.

But these failed to make Tenaga appealing during the year.

That said, the stock remains as a consensus buy with 15 out of 20 analysts tracking it having a “buy” recommendation. Their positive views partly hinge on a high dividend yield at above 8% and the undemanding valuation at low teen price-earnings ratio.

Maybank Investment Bank analyst Tan Chi Wei views that Tenaga has both the resolve and the required balance sheet strength to mount a serious renewable transition push. — by Shazni Ong

Magnum Bhd

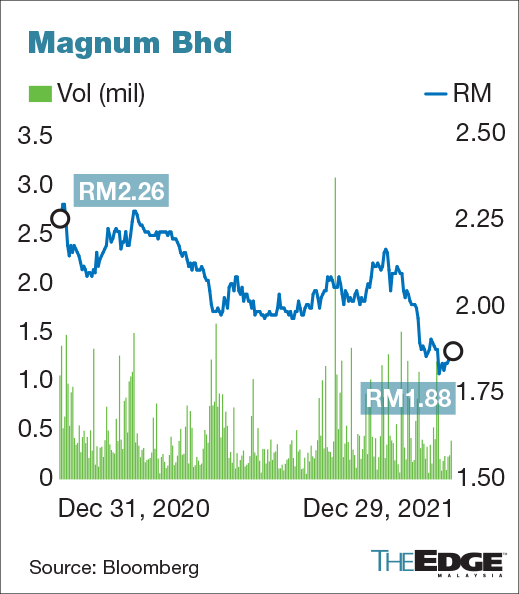

Numbers forecast operator (NFO) Magnum Bhd was chosen early this year in anticipation of improved performance and attractive dividend yield — provided that there would be no more movement restrictions and draw cancellations, which hounded its performance in 2020 amid the pandemic.

However, the worst case scenario happened as lockdown measures returned, stricter than before, which further hammered Magnum and other fellow NFOs earnings. For the nine months ended Sept 30, 2021 (9MFY21), Magnum sank into the red with a net loss of RM20.34 million, versus a net profit of RM62.19 million it made in the same period a year ago, as revenue shrank 32.23% to RM776.55 million from RM1.15 billion.

Besides lesser draws due to the movement restrictions, it also made higher prize payouts. Notably, it didn't declare any dividend for FY21 so far, as opposed to the 6.54 sen it announced in January-September of 2020.

Meanwhile, the stock has fallen 16.82% YTD. Going forward, CGS-CIMB Research analysts Sherman Lam Hsien Jin and Foong Choong Chen are anticipating Magnum returning to the black by reporting a net profit of RM36 million in the fourth quarter ended Dec 31, 2021 (4QFY21) — after posting a net loss of RM29.91 million in 3QFY21 — on the back of a full quarter of operations and a gradual pick-up in NFO sales.

They projected the company’s earnings per share (EPS) to grow to 16 sen for FY22 and FY23 each, from projected EPS of four sen in FY21, underpinned by NFO sales recovery post-Covid-19 restrictions and aided by clampdown on illegal NFOs, according to their research note dated Dec 15.

With the anticipated earnings growth, they are expecting Magnum to restore its dividend payout to pre-pandemic levels of 15.2 sen in FY22 and 15.4 sen in F23, for a projected dividend yield of 8.09% and 8.18% respectively.

The research outfit has a “buy” call on Magnum with a TP of RM2.30, which indicates an upside of 22.34% as of its closing price of RM1.88 on Dec 29. — by Justin Lim

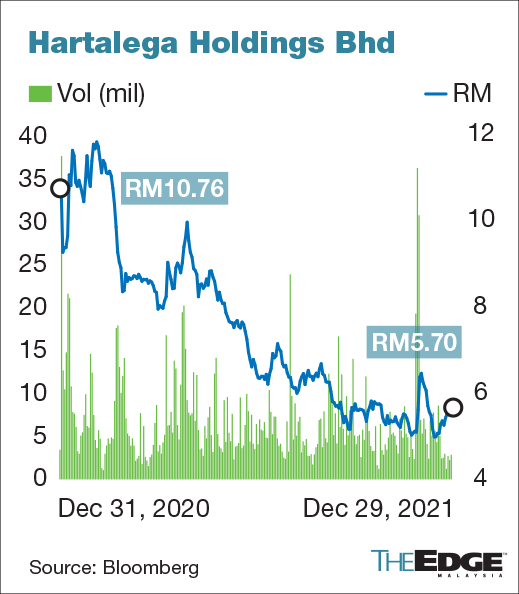

Hartalega Holdings Bhd

Glove maker Hartalega Holdings Bhd was the worst performer among our stock picks for the year, with a YTD decline of 46.92% amid the sharp fall in average selling prices (ASP) for gloves due to soft demand and increase in capacities, which in turn soured investors' sentiment.

Nonetheless, the counter still garnered 10 "buys" out of 23 analysts covering the stock, according to Bloomberg data; of the remainder, eight had it on "hold" while five placed it on "sell".

In reiterating his "buy" or "add" call on the stock, CGS-CIMB Research analyst Walter Aw said he believes Hartalega is fundamentally solid, as it has a net cash of RM4.7 billion at end-2QFY22.

Aw’s TP for the stock is RM6.40, which implies an upside of 12.28%, compared to Hartalega’s last closing price of RM5.70 on Dec 29.

He said in a Dec 15 note that Hartalega deserves to trade at a premium to its sector, given its industry-leading technology in the nitrile space, higher margins, and stronger ESG metrics in the glove sector.

Hartalega was once one of Maybank Investment Bank's top picks. However, it has now been downgraded to “sell”. In a strategy note dated Dec 9, Maybank IB analyst Wong Wei Sum, who kept his “negative” view on the glove sector, said glove ASPs have yet to find a bottom. As such, he does not think this is the time to bottom-fish glove stocks just yet.

While new Covid variants such as Omicron may slow down the decline in ASP, the underlying structural negative ASP trend will remain intact, Wong said. He also expects interest in Covid-related stocks such as gloves to wane, as the vaccination rate rises globally. — by Justin Lim

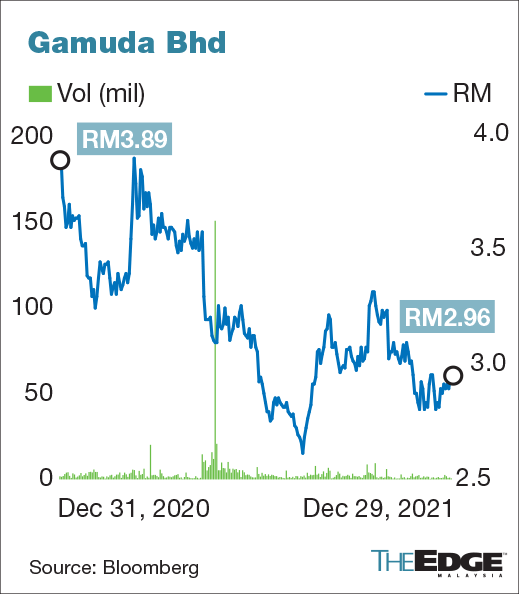

Gamuda Bhd and Sunway Construction Group Bhd

There was high hope that the government would kick-start more infrastructure building projects to drive economic growth in 2021 — a move that would have augured well for construction outfits, like Gamuda Bhd and Sunway Construction Group Bhd (SunCon).

However, construction stocks did not perform as well as expected. The Bursa Malaysia Construction Index has fallen 17.4% YTD as at Dec 29 to 154.27 points, a reflection of the lacklustre interest in the sector.

Likewise, the share prices of both Gamuda and SunCon headed lower although the duo posted higher earnings during the year.

Gamuda fell 24% YTD to close at RM2.96 as at Dec 29 after it hit a high of RM3.90 in March. SunCon rose to a year's high of RM1.87 in early March. However, the upward momentum was not sustainable, dropping to a low of RM1.51. It has lost 17% YTD to RM1.56 as at Dec 29.

Interestingly, the two construction stocks remain on most analysts' recommendation lists. There are currently 13 "buy" calls on Gamuda compared with four "hold" calls and two "sell" calls, according to Bloomberg. The average target price is RM3.64.

Over at SunCon, eight out of 13 analysts who track the company are advising their clients to buy SunCon shares. The average target price is RM1.80.

Nonetheless, Hong Leong Investment Bank Research is bullish about the construction sector in 2022. It forecasts construction-sector earnings to double next year, driven by higher productivity and wider margins amid expectation of job awards recovery driven by both the private and public sectors. — by Shazni Ong

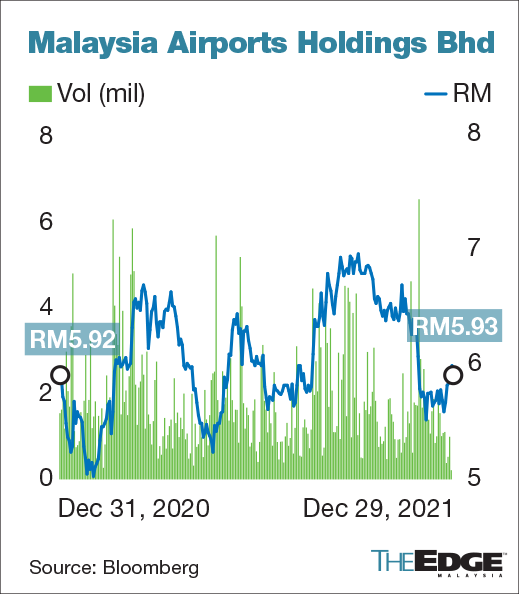

Malaysia Airports Holdings Bhd

The airport operator was seen as a good proxy to the recovery theme play in 2020 amid expectation of higher cross-border air travelling this year.

Although cross-border travelling remains restrictive throughout the year due to the resurgence of Covid-19 cases and the emergence of Delta variant, Malaysia Airports Holdings Bhd's (MAHB) share price has been resilient.

The stock closed at RM5.93 on Dec 29, nearly on par with last year's closing of RM5.92 even though foreign tourist arrival has yet to recover in Malaysia. It reached a year's high of RM6.97 on Oct 4.

Nonetheless, MAHB has seen a glimpse of gradual recovery following the vaccination roll-out and the drop in new Covid-19 cases, which have led to ease of travel, such as the Langkawi international travel bubble and the Vaccinated Travel Lane.

In November, MAHB saw passenger movements of 4.7 million — an increase of 158% over the same month last year.

This was the highest volume recorded for its network of airports since April 2020 after the first Movement Control Order (MCO) was implemented in Malaysia on March 18, 2020, and suspension of international flights in Turkey towards the end of March 2020.

Looking ahead, MIDF Research believes that the passenger traffic will be further improved in the coming months following the allowance of interstate travel in Malaysia coupled with the introduction of safe international travel initiatives among governments. However, the firm said the resurgence of Covid-19 cases due to the new variant remains as a key concern. — by Shazni Ong

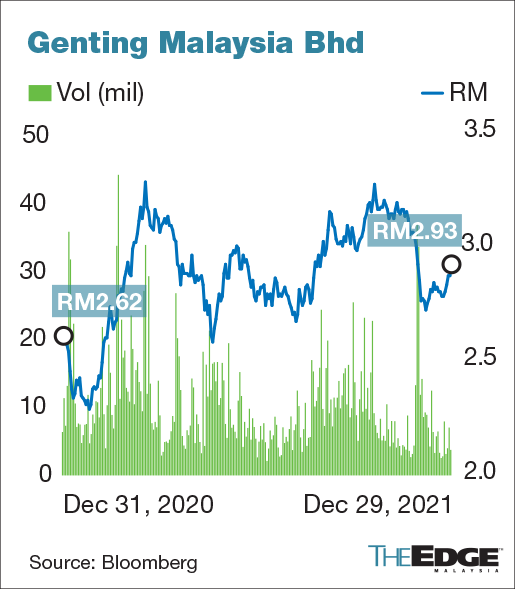

Genting Malaysia Bhd

Genting Malaysia Bhd (GENM), which was battered in 2020 amid the unprecedented pandemic that forced it to halt its operations around the world, was among top picks of fund managers and analysts in 2021.

With vaccine availability, it was expected to benefit from pent-up domestic tourism demand as international borders were expected to remain closed for some time and Malaysians wouldn't be able to travel abroad. Even if international borders had reopened this year, GENM was expected to benefit from the arrival of foreign tourists.

As such, from a low of RM2.30 on Jan 25, GENM shares rose to a high of RM3.29 on March 18. But the stock's growth momentum faltered following the reintroduction of movement restrictions, as Covid-19 cases surged. Nevertheless, YTD, it is still up 11.94%, as it settled at RM2.93 on Dec 29.

The group’s financial performance in the latest quarter was within most analysts’ expectations. Its net loss for the third quarter ended Sept 30, 2021 (3QFY21) narrowed to RM289.25 million from RM704.64 million a year ago, as its overseas operations recovered. Its revenue for the quarter, however, fell 41.69% to RM826.27 million from RM1.42 billion, due to lower contribution from the leisure and hospitality business in Malaysia.

For the nine months ended Sept 30, the group’s net loss also narrowed to RM1.12 billion from RM2.02 billion a year ago, while its revenue slid 34.99% to RM2.27 billion from RM3.49 billion.

Fund managers and analysts remain positive on GENM, as its cash cow Resorts World Genting (RWG) has resumed operations following the lifting of movement restrictions.

According to Bloomberg, up to 12 analysts have the stock on “buy”, while five kept it on “hold” and one has it on “sell”. The average TP for the stock is RM3.45. — by Tan Siew Mung

British American Tobacco (Malaysia) Bhd

British American Tobacco (Malaysia) Bhd (BAT Malaysia) was seen as an undervalued play in 2021, after its share price fell to RM13.14 on Dec 31, 2020, from over RM40 four years back.

Due to its defensive nature, the tobacco manufacturer climbed steadily to a high of RM15.20 on May 25. However, it did not manage to sustain its momentum, and eventually closed 0.71% lower YTD at RM13.98.

This was despite the group managing to grow its net profit for the third quarter ended Sept 30, 2021 by 23.43% to RM78.68 million from RM63.74 million a year ago, on lower operating expenses, even as quarterly revenue slipped 2.31% to RM613.02 million from RM627.52 million.

For 9MFY21, the group’s net profit climbed 26.19% to RM213.41 million, from RM169.12 million a year earlier, while revenue grew 7.26% to RM1.78 billion from RM1.66 billion.

Consistent with its sales volume growth trajectory, the group’s total market share stood at 52.5%, up one percentage point (ppt) from the same period last year.

The group has paid out 71 sen worth of dividend YTD — after a third interim dividend of 26 sen was paid out on Nov 25 — which was 95% of its earnings per share for the nine months ended Sept 30 (9MFY21).

Analysts are mixed on BAT Malaysia’s outlook. According to Bloomberg, seven analysts have it on “buy”, while eight recommended a “hold”. The average TP stands at RM16.03. — by Tan Siew Mung

MyEG Services Bhd

E-government service provider MyEG Services was seen as a stock with great potential this year, as many of its contracts have been renewed.

It was also a busy year for the group, as it got several new contracts amid the continued spread of the Covid-19 pandemic. For instance, it was recently appointed the exclusive distributor for Breathonix Pte Ltd’s BreFence Go Covid-19 Breath Test System (BreFence Go) in Malaysia.

It has also received approval from the Road Transport Department (JPJ) to commence the proof of concept (POC) for an automated training and driving test system.

The firm will also be introducing decentralised finance (DeFi) products in Malaysia to provide cryptocurrency services to users of digital asset exchanges that are licensed as recognised market operators locally and abroad.

Shares of MyEG, which fell to as low as 78.5 sen on Aug 4, and climbed to a high of RM1.11 on Nov 25. YTD, it has increased 11.46% to RM1.07.

The increase in net profit came as the group’s net profit for the nine months ended Sept 30, 2021 climbed 22.21% to RM235.43 million, from RM192.64 million a year ago, with revenue increasing 28.21% to RM490 million from RM382.17 million.

According to Bloomberg, eight out of nine analysts who covered the stock have “buy” calls on it, while one adopted a “hold” stance. Their average TP for MyEG is RM1.44. — by Tan Siew Mung

Mega First Corp Bhd

Mega First Corp Bhd, which is engaged in the renewable energy (RE), resources and packaging businesses, was selected as a top pick at the start of the year due to the expected steady and resilient earnings from its 260MW Don Sahong hydropower project.

Shares of the company had a good start in 2021, as it climbed to a high of RM3.93 on Feb 5, from RM3.27 on Jan 12. However, it pared most of its gains towards year-end, with only a gain of 1.74% YTD to RM3.51.

The group’s net profit for the third quarter ended Sept 30, 2021 (3QFY21) saw a slight decline of 0.72% to RM88.86 million, from RM89.5 million a year ago, dragged by its renewable energy and resources divisions.

Its quarterly revenue, however, expanded 10.08% to RM232.5 million from RM211.21 million a year ago, bolstered by an increase in revenue contribution from the packaging division.

For the nine months ended Sept 30, 2021 (9MFY21), the group’s net profit went up 9.33% to RM249.52 million from RM228.24 million a year ago, while its revenue increased by 14.63% to RM634.05 million from RM553.16 million.

According to Bloomberg, four analysts who covered the stock recommended a “buy” for it. Their consensus TP works out to be RM4.41, a potential upside of 25.64% from its current level. — by Tan Siew Mung

https://www.theedgemarkets.com/article/look-back-11-stocks-experts-said-you-should-own-2021

More articles on Stock Pick Contest Year 2021

Discussions

Be the first to like this. Showing 20 of 20 comments

the 11 stocks generated a return of -4.29% year-to-date (YTD), though still outperforming the FBM KLCI's -5.05%.

and,

The experts picks, although can't beat FD but still better than many retailers picks :D :D

2021-12-30 10:27

The return of 11 highest stocks picked in i3 Stock Pick Contest Year 2021 ?

2021-12-30 10:34

the edge

i3 result for nov.

https://klse.i3investor.com/blogs/stock_pick_2021/2021-11-30-story-h1594734076-Stock_Pick_Year_2021_30_Nov_Result.jsp

firehawk The return of 11 highest stocks picked in i3 Stock Pick Contest Year 2021 ?

30/12/2021 10:34 AM

2021-12-30 10:41

thanks,

but I mean the return of the 11 stocks that highest picked in the contest :-)

2021-12-30 10:44

Negative return for stocks picked by so called experts. Would not want to place my money with them to invest. Definitely

2021-12-30 15:27

Glad to know that my performance is slightly better than the "Experts" this year. I think they are only expert in manipulating the price.

2021-12-30 17:15

with vast resources they have, few computers, fat salaries, these so-called experts are really a shame..

2021-12-30 17:29

Countdown - 1 more day

Please submit 2022 pick after 31-Dec-2021 4:50pm

https://klse.i3investor.com/blogs/stock_pick_2022/2021-12-27-story-h1596428352-Stock_Pick_Contest_Year_2022_How_it_works_Please_submit_after_31_Dec_20.jsp

2021-12-30 17:47

Not a single technology pick there. The experts couldn't have picked the worst sectors even if they tried. Always go with what market wants.

2021-12-30 19:12

Glad to know that my performance is slightly better than the "Experts" this year.

2021-12-31 08:15

Those expert talk cock only la. They don't disclose their full portfolio man. Just snapshot of the portfolio only.

2021-12-31 14:44

Expert -tive return. Omg. No need get high degree from Universities lah. Monkey throws darts at newspapers also can pick better shares from newspapers.

2021-12-31 17:06

Typo*** Expert -tive return. Omg. No need get high degree from Universities lah. Monkey throws darts at the Edge stock section in newspapers also can pick better shares from newspapers.

2021-12-31 17:08

2022 is year of WATER TIGER. Very FIERCE WATER TIGER. The Crocodile also scares of WATER TIGER. Seriously.

2021-12-31 17:10

lousy returns, buy US Stocks easily 100% returns... bungkus lah you all, plus MYR lousy currency

2021-12-31 19:36

This is the TOC page for Stock Pick Contest Year 2022 - https://klse.i3investor.com/blogs/stock_pick_2022/2021-12-31-story-h1596494692-Stock_Pick_Year_2022_Table_of_Content.jsp

Kindly review and feedback if you find any mistake on the portfolio setup.

Please take note that there are few submissions not follow the requirements have been ignored.

Thanks!

2021-12-31 22:04

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Apps

Top Articles

1

https://dividendguy67.blogspot.com

3

4

Good Articles to Share

Could Kamala Harris beat Donald Trump in November's presidential race?

5

Good Articles to Share

Iranian warship capsizes during repairs in port of Bandar Abbas

6

Good Articles to Share

7

Good Articles to Share

Jonathan Turley unveils exciting new book 'Free Speech in the Age of Rage'

8

Good Articles to Share

Why Impossible Foods signed hot dog-eating legend Joey Chestnut #yahoofinance #youtubeshorts

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

No trading signals available.

Stock

Time

Signal

Duration

No trading signals available.

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Tan KW

Stock Pick Contest Year 2022 - How it works? (Please submit after 31-Dec-2021 4:50pm) https://klse.i3investor.com/blogs/stock_pick_2022/2021-12-27-story-h1596428352-Stock_Pick_Contest_Year_2022_How_it_works_Please_submit_after_31_Dec_20.jsp

2021-12-30 09:46