TeoCT

Dayang - intrinsic value

Dayang – what exactly is its value

If you are an investor (holding a counter for at least 2 years) intending to invest in Dayang, I urge you go read the three Petronas Activity Outlook (PAO) – 2017-2019; 2018-2020 & 2019-2021. There is a wealth of information and very professionally presented focusing on what is relevant ONLY, very good.

An example:

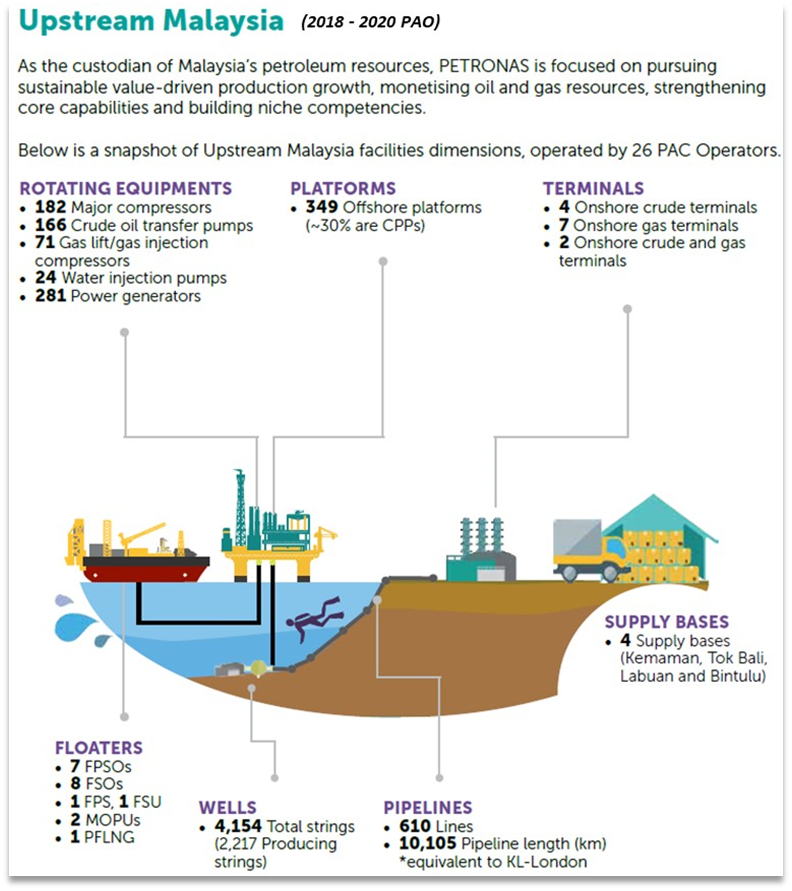

In one picture / infographic, the whole upstream in Malaysia is shown, wonderful.

Note – there are 349 offshore platforms! (Update - PAO 2019 2021 shows 353 offshore platforms)

I return to the ENTROPHY theory – these platforms need maintenance, ALWAYS (5 – 8 years cycle).

Sydney harbour bridge, San Francisco golden gate bridge, forth bridges in Edinburgh and many other such bridges – the fact is when the contractors finished painting this end, they must return to the other end and start all over again.

So, WORK is always there, 349 platforms!!! And growing.

Unfortunately, it is not clear from the PAO what is that one critical equipment required to carry out this maintenance work. This is, the Accommodation Work Barge or Work Boat.

Dayang Opal (left) built in 2012, WORK BOAT (WB) accommodate 197 persons with lifting capacity of 45 tonnes at 41.2m boom length. Dayang Pertama (right) built in 2005 – 189 persons, 25MT at 43m.

Above is a typical Accommodation Work Barge (AWB) that accommodate 300 persons and the crane capacity is 300 tonnes.

This is OFFSHORE; no home to go back to, or just drive down the road to the hardware shops to buy material that is missing, etc. These vessels are a MUST.

Having these vessels will be the edge, some call it MOAT, some, the barrier to entry.

Vessels not in used (in anchorage) is as good as scrape metal the longer they are not used. Read ICON article by Capt. Hassan Ali (https://www.theedgemarkets.com/article/icon-offshore-set-sign-debtrevamp-deal-month).

It is obvious Dayang (with Perdana) is miles away where AWB and WB is concern. For either Carmin or Petra to compete on par with Dayang, they will need to “plant up” with AWB/WB.

In February 2014 (https://www.theedgemarkets.com/article/petra-energy-sell-vessel-perdana-petroleum) there were talks between Petra and Perdana to sell / buy Petra Endeavour for US 25M. Ignoring inflation, one unit 300 pax AWB will cost about RM 104M today. And if you order one today, you will only get it about three years later. The odd is stack against you as all the necessary maintenance contracts has already been awarded. Next round will be in 2024. Who will lend you the money to build the AWB under current climate (with so many companies still under water) and without a contract too? Buy one in anchorage but need to drydock and refurbish, say RM 50M (guesstimate)?

(A rich man tried with FPSO and see where that got him albeit it is different sphere but similar, service to oil majors, one Company tried, also FPSO, almost went bust, taken over by the other Malaysian FPSO company –it is not easy to get in regardless one got money or otherwise.)

Furthermore, the age of Dayang (+ Perdana) AWB vessels are younger than Petra’s.

Carimin does not have one unit (AWB) so they will have a tough time muscling in for more job.

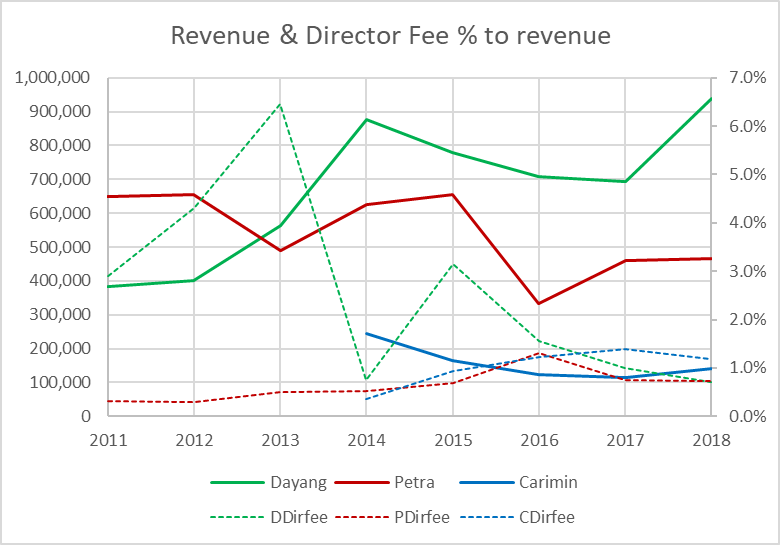

Still not convince, here are the profit margins (gross and net) plus free cash flow for consideration.

Dayang (together with Perdana) has a competitive edge (moat) in the MCM and HUC sphere; in fact, one can say, domination, because they have 6 units of AWB, 9 units of WB; double the nearest rival, Petra has only older AWB (3 units) and 4 units WB that come with higher maintenance cost.

And Dayang (green line) can generate cash for future (new vessels) capex compare to the other two.

Thus, the next cycle (2024-2028) of maintenance contracts, Dayang will again win the major bulk of them, sure, no guarantees, but highly likely.

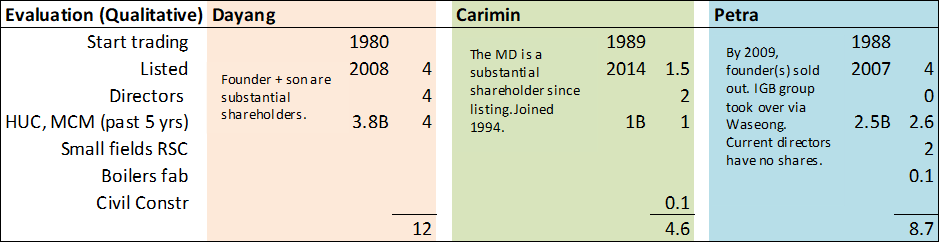

Directors

Among the three companies, only Dayang still has founder in the mix. Carimin MD (join 1994) and one other director hold substantial share in the company. Petra directors do not even hold a single share (2018 AR), they have no skin in the game.

Moreover, Carimin and Petra are both involved in other businesses; while Petra’s are all in the oil & gas sphere, Carimin is outside (civil construction). This potentially dilute Board’s attention and focus on the HUC /MCM work and there is no synergy at all.

The closet rival, Petra, with directors having no skin in the game, I do not think there is much "drive", how to replace aging marine fleet to compete and FCF is so low?

Nonetheless, the directors pay, and fees are reasonable, Dayang and Petra coming in at 0.7% of revenue while Carimin is 1.2%. Dayang's revenue is also a quantum leap from the other two, Carimin is the lowest.

I think Dayang directors, especially the founder, have been very competent and know exactly where they want the company to be in the next 5 years, next 10 years and further. Yes, they underestimated the cost to get into Perdana, in hindsight, everything is crystal clear. Who predicted that oil price stayed low for that long?

But as argued above, Dayang requires Perdana, it is symbiotic, management control of the AWBs is important. This provided Dayang with price setting influence, and flexibility in pricing to the various clients. Do not forget, 60.48% of whatever price set by Perdana goes back to Dayang.

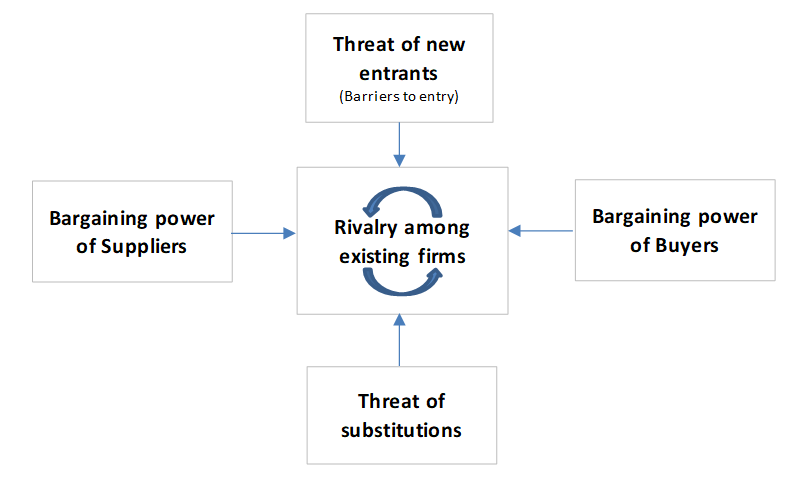

Still not convince, another way to look at the situation:

- Threat of new entrants – the need for AWB and or WB will dissuade, of course some will try but I just do not see how they can replace Dayang or even “chip” into the market.

- Threat of substitutions – newer platforms may come with components that requires lower maintenance; but the current 349 platforms will continue to require maintenance between 5 to 8 years until they are de-commissioned (when – ahh, easily for next 25 years, more later)

- Suppliers bargaining power – only Dayang with 65% to 70% of work can resist

- Buyers bargaining power – currently Carigali has the power as it has the higher number of platforms, the rest, of course will be based on open tender value. However, due to size of Dayang, it can dictate price that Carimin and Petra will find hard to make good money.

- Rivalry among Carimin, Petra and Dayang – the market is curved out for the next 5 years, so there should be no to minimal rivalry. Besides, due to Dayang (+ Perdana) size, Cariman and Petra just could not compete in price.

Oil price - Oil use

This question, future of oil as a source of energy to the world, the fear that it is coming to an end soon, well I cannot tell what the oil price would be, but I can tell you oil will continue to play a big part as a source of energy to the world at least until 2050. Please read all 15 pages of the following report from: https://www.oxfordenergy.org/wpcms/wp-content/uploads/2019/07/The-Energy-Transition-and-Oil-Companies-Hard-Choices-Energy-Insight-51.pdf?v=f5c3020d846f

When I finished Form 5 in mid 70s, there were talk that oil will run out in 10 years (in Malaysia). Then when I had my first kid in late 80s, again oil will run out in 20 years, today, oil is still being produce in Malaysia.

Extraction technology does not stand still, now we are talking about enhanced oil recovery, in the future, the above report provides some glimpse. And, new fields are being found.

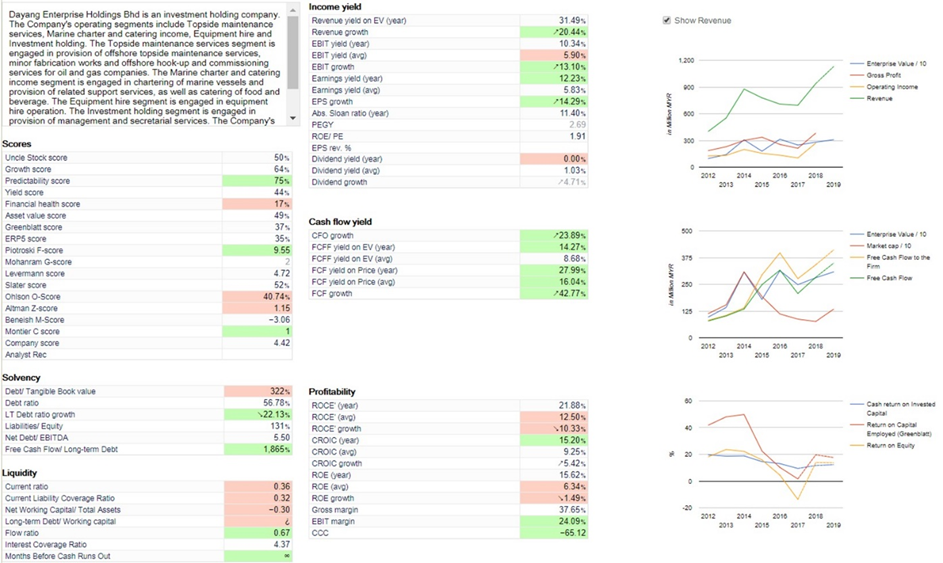

I will now attempt to determine the intrinsic value of Dayang, in fact I will not. There is this website – Unclestock (https://www.unclestock.com/#!s=5141.KL) does it all. ROC, ROCE, ROIC and more. (Thanks US for internet.)

Unclestock did not stop there, it went on to cash flows in various metrics and intrinsic value (IV) based on so many different methods – DCF, Warren Buffet, Graham, Lynch, etc., all in all 10 methods giving results of 0.54 to 5.71 RM/share. And it averages the IV to one figure – 1.82 RM/share.

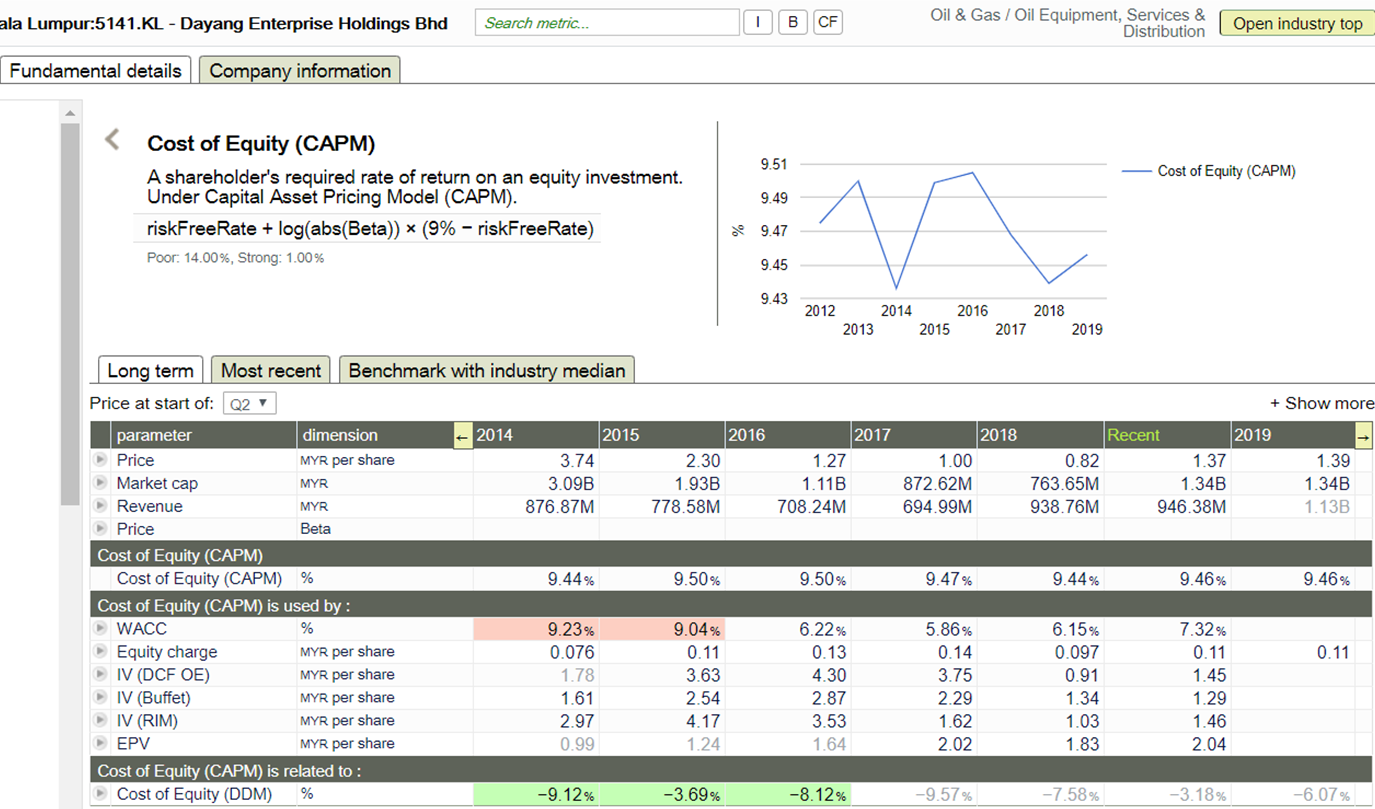

The cost of equity (CAPM) used is as shown in unclestock, extracted below for easy reference:

CAPM calculated is 9.46%, lower than the many returns (on capital, invested capital, etc). So Dayang is creating shareholder values.

There is no need to further throw in these returns, that per shares and so on, everything is at this unclestock. All these metrics are all very well. It uses current data and spew them out (garbage in garbage out). One can pick and choose the metric to justify one’s view. Who is right who is wrong, well it is all relative?

The question that an investor needs to ask is the future. Next 5 years – 10 years, will DAYANG continue to dominate, make more money, will it continue to have so much business? Answer is yes, yes and YES.

The closest rival – Carimin and Petra, their cash flows will not allow them to plant up (check unclestock if you do not like my charts above). Dayang can easily!

This dominant position should be worth something that I think, the many IV methods did not account for, +18%, gives Dayang intrinsic value as RM 2.15 per share.

Conclusion

- Dayang has a wide moat – ownership & control of newer 6 units AWBs & 9 units WBs

- Work is always there – 349 platforms and counting, just more or less, depending on the oil price. During lower for longer period, Dayang’s revenues, 2015-778M; 2016-708M; 2017-695M is still respectable plus excellent FCF.

- This 5-year cycle – 2019 to 2023 MCM is all firmed, done deal, all RM 3.5B to RM 4B of it, now waiting for results of I-HUC tender.

- Next cycle – 2024 to 2028 (and future cycles to come), highly likely Dayang will win similar (contract) value if not more.

- Intrinsic value is RM 1.82 to 2.15 per share.

Gosh so much serious work, here something to lighten the mood.

A man is dating 3 women and is trying to decide which to marry. He gives each of them $5,000 to see what they do with the money.

The first has a total makeover. She goes to fancy salon, gets her hair, nails and face done and buys several new outfits. She tells him she has done this to be more attractive to him because she loves him so much.

The second buys the man a number of gifts. She gets him a new set of golf clubs, some accessories for his computer and some expensive clothes. She tells him that she spent all the money on him because she loves him so much.

The third woman invests the money in the stock market. She earns several times the $5,000. She gives him back his $5,000 and reinvest the remainder in a joint account. She tells him she wants to invest in their future because she loves him so much.

Which one does he choose?

Answer: the one with the biggest boobs.

Thank you all for reading. It has been a most interesting journey for me, learning, understand how to assess, value and understand the business of Dayang.

Also, thanks for the insights provided by so many readers and forum contributors. Hope we all learnt something.

Further thoughts:

Eventually, Dayang will gives dividend again (maybe 2 years down the road) once debt is parred down somewhat.

There is not much R&D apparent in (public) information so far. I am sure Dayang (now considered including Perdana) is doing plenty (plus digitalization) to maintain their No.1 position in the HUC & MCM sector. This is in term of delivery (execution of work, completing timely and within budget).

Doing de-commissioning (of platforms) will be a natural extension and again, Dayang, will be front and central in any tender/contract.

With Petronas support, Dayang (& others) are going oversea – this is positive.

The I-HUC tenders, intense lobbying, may follow the distribution of the MCM contracts if work is distributed like MCM, else, maybe 50% Petra, 50% Dayang (or less as it is in the interest of Petronas to avoid too reliant on one contractor ONLY). Heck, if RM4B is true, 30% will be whooping RM1.2B, spread normally over 3 to 5 years.

Recent changes in substantial shareholders is intriguing to say the least. On balance, should be more positive than negative.

Have a pleasant weekend and Happy investing all.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on TeoCT

The Great American Firewall: On the Question of Censorship by Danny Haiphong

Created by teoct | Jul 23, 2020

Discussions

7 people like this. Showing 26 of 26 comments

Sell before uncle koon sells. That's the intrinsic value I believe :D

2019-07-20 11:35

Having seen the pain so many went through with the lesson many learnt with Heng Yuan (Shell), I will stay away esp if the super investor is promoting the stock. I apologize to you teoct for my comments esp after you had taken so much pain and effort writing these articles. The 'sea' is so full of fishes and I will prefer to catch the 'others' Fools tread where wise man stay away!

2019-07-20 13:24

teoct , thanks again for coming up with such a comprehensive article on dayang business and future potential . The competitive studies showed that dayang has an obvious edge over the other 2 competitors .

2019-07-20 14:13

I think IMO 2020 will boost Malaysian sweet crude production tremendously....

pretty sure it will have explosive effect on Dayang.

2019-07-20 14:20

even with the same throughput-production output...all malaysian petroleum producer will double or triple their profit due to significant premium our oil will have against other sour crudes..

this profit will trickle down to midstream and downstream players...

2020 might turn out to be the best year for Malaysia

2019-07-20 14:30

imagine the effects on bottom line.. a premium of 15 usd/brl from a premium of 4 usd/brl will have

Australian Pyrenees crude sells at record premium ahead of IMO 2020 – sources 28/05/2019

https://www.hellenicshippingnews.com/australian-pyrenees-crude-sells-at-record-premium-ahead-of-imo-2020-sources/

Australian oil and gas company Santos has sold heavy sweet crude Pyrenees at an all-time high premium of more than $10 a barrel as traders continued to stock up the oil ahead of a ship fuel change mandate, three trade sources said on Monday.

* The 600,000-barrel cargo loading in late-July was sold to a trading company at a premium close to $15 a barrel above dated Brent, they said

* Pyrenees is one of a handful of Australian heavy sweet crude grades that are being sold at record premiums because of strong demand from traders who are storing the low-sulphur oil to prepare for a surge in ship fuel demand when IMO 2020 kicks in.

2019-07-20 15:58

Petronas have all the incentives to ensure all their rigs in tip top condition for full swing production....they would need to fill up the vacuum created by the unusable sour crude oil

2019-07-20 16:04

What kind of moat does Dayang has? Scale economies, network effect, process power, brand, switching cost, counter-positioning, or cornered resources?

2019-07-20 20:58

Another thing: When a website or an analyst start throwing many valuations at you i.e DCF, Graham, Warren Buffet, Lynch, Ricky Yeo etc - you can safely ignore those valuation

2019-07-20 21:01

TeoCT, what was the cost of equity used to derive the Intrinsic value? Thats quite important to know..as it means even if you buy at the esrimated IV, your growth..i.e return is as per COE.

Thanks for sharing this Unclestock link. Need to subscribe

2019-07-20 21:31

ok i got it...they had used 9.5%

https://www.unclestock.com/#!s=5141.KL

a lot of information there... interesting site.

2019-07-21 02:39

Thank you all for the likes, comments and sharing. Indeed, pputeh, one should stay within ones competency. Mine is oil & gas. But did you not like the joke?

deMusangKing, I was reminded of this: Mother Teresa was wandering the corridor and heard a young Sister shouting "F@$# off to the birds on the window ledge". She came in and advised, "Sister, all you had to say is shoo and the birds will F@$# off".

But thank you for visiting and appreciate it very much.

probability, yes CAPM is 9.5% and unclestock is indeed interesting and supercool. This will add to my laziness in studying new counters. I have included it in the write-up to avoid uncertainties. And importantly it is less than the several returns (on capital, equity, etc) for 2018. A positive sign.

Mr Yeo, interesting queries:

a) scale economies, you meant "economy of scale" - yes, Dayang certainly has economy of scale as their vessels will be used much more compared to the other two. Much like Airasia - keep the planes in the air. Base cost divided by more hours used, that is why I said Dayang has pricing power, price setter rather than price taker.

b) network effect - from my limited knowledge, this is more for internet type of businesses like Facebook, Google, etc. But, all the PSCs, production sharing contractors, (Shell, Carigali, ROC etc) - users, will definitely know Dayang and had used their service one time or another and will have experienced their capability and quality of delivery, which is good as far as I know.

c) process power - Carimin, Petra and Dayang will have similar process to implement the MCM works as this processes is quite universal in the other part of oil and gas regions. It will be the quality of delivery (QA/QC) and on time that become important and more importantly the equipment (in this instance, AWB/WB vessels) to deliver the MCM services.

d) Brand - in Malaysia, I would say Dayang has Brand power (in O&G, known to deliver), how to quantify, I am at a lost. In the region, Dayang probably known, but each Nation has their own peculiar requirements that may have impeded Dayang from forging outside Malaysia. The contract in Turkmenistan is via Petronas.

e) switching cost - to the PSCs that has contracts with either Carimin and Petra, it will cost them to switch to Dayang mid-way through current contracts. They will only do so if their appointed contractors are not performing or there is certain critical work that need doing as Dayang has the capability and capacity to response to quickly. However this type of work is rare and Dayang will charge an arm and a leg.

f) counter-positioning - I am at a lost here, looking forward to your clarification.

g) cornered resources - in a way yes. As the vessels under Dayang (& Perdana) are being used (generating cash) while those of Petra, ICON and Sea-link are in anchorage, the longer, the worst off for them. The PSCs are very particular that vessels meet the sea going standards as life is at stack (reputation risk), and these vessels need to be dry-dock every so many years. Each dry-dock will cost millions. Now if there is no jobs, obviously postponed and the longer the postponement, the higher the cost to dry-dock. So, vessels of Dayang becomes more valuable as they are always able to meet requirements. It is not in the conventional sense that Dayang owned all the AWB/WB, then no.

"you can safely ignore those valuation" - I am a bit lost here. Appreciate if you will advice, how then, to value Dayang's intrinsic value.

I was intrigued to actually find that there are so many ways to value a company and I am sure different method will probably be applicable to certain type of company and not to others. I am just too lazy to find out (if that is what you meant). A statistical average sound like a decent estimate of all the different methods at unclestock, after all, these are all estimates, no right nor wrong.

Nevertheless, many thanks for the interesting queries. I hope the clarification clear some (if not all) of the issues.

Happy Sunday.

p/s, gosh all comments received are serious, I hope the joke towards end help some.

2019-07-21 11:22

probability - thanks for sharing on the potential higher prices for Malaysian crude. Hibiscus will benefit more than Dayang in this particular case.

Keep them coming mate. Take care.

2019-07-21 11:28

On unclestocks.com, look like the Cash and ST investment in the Balance sheet are wrong from 2016 onwards

2019-07-22 06:29

coolio, yes it is different because unclestock considered deposit placed with banks to be not as liquid as unit trust (ST Investment) - "very liquid assets", that is the term unclestock used. Deposit placed with banks might be used as collateral for loans and unclestock has been conservative here.

2019-07-22 09:13

Cold hard truth? Dilution of directors attention? Malaysian directors so incompetent? Rate this C.

2019-07-22 11:13

dusti - cold hard truth? Maybe warm truth, not hard as it is a qualitative assessment. But, there is always a but, civil construction industry is one notoriously bad paymaster. There is that possibility of diversion of fund meant for MCM work to the construction work to maintain that (civil) project. When this sort of decision put to the Board, what do you think? I have seen many companies through wanting to increase "shareholder return" (sometime I wonder which shareholder's return) get into jam. The possibility is there.

Now, I am sure all of these three will have 5-years plan to develop the company. Surely capital (working or PPE) would be required. In Petra, they will need to go back to the respective major shareholders to seek approval or even funding (RI/PP). Hey, directors authority (spending) levels are also set, OK. If one research who the major shareholders are, one would come away with reservation/doubt. The major shareholders likely say, fund from internally generated fund or borrowing. With the type of cash flow, most unlikely, so the Board will be frustrated and dishearten. As Mr Yeo said, need CAPEX to renew vessels, etc. which company will have the capability?

Incompetent - I do not think that these (above) are sign of incompetence. But the choices presented for decision making is such. Also, most likely, (independent or otherwise) directors are selected such that they share major shareholders thinking.

A company with founder as director would more likely make decision that benefit him as a shareholder (and more likely minority shareholders too). Sometime it is not RM 1,000 / RM 10,000 / RM 100,000 or RM 2M but RM 800 M decision (RI/PP & sukuk). He himself has to come out with millions as well, do not forget that.

Ok C, fair I suppose without much "hard" facts except my conjecture.

Happy investing.

2019-07-22 16:06

As was mentioned in the article there was intense lobbying. Subsequently, market here-say was the I-HUC cancelled. Carigali had no choice but to proceed to award the HUC contracts accordingly as they have the most new platforms to install and commission.

Petronas Carigali being the largest operator in Malaysia awarded 3 contracts for HUC to Carimin (Angsi only), Dayang (P Msia exclude Angsi) and Petra (Sabah & Sarawak). Unfortunately no value was given in the announcements. Maybe in value would be 15% (Carimin) / 35% (Dayang) / 50% (Petra) of a total value of around RM 1B to 1.5B. Dayang portion would be RM 150M to 225M, not bad at all.

2019-09-16 11:43

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2025-01-06 15:50:00

ADX

5 Mins

SELL

2025-01-06 15:25:00

ADX

5 Mins

BUY

2025-01-06 15:05:00

ADX

5 Mins

SELL

2025-01-06 14:55:00

ADX

5 Mins

BUY

2025-01-06 14:45:00

ADX

5 Mins

SELL

Apps

Top Articles

1

The Alpha Trader

2

南洋行家论股

3

Good Articles to Share

Why so many younger Chinese are saying ‘I don’t’ to marriage and family

4

Good Articles to Share

5

Good Articles to Share

Expect another 'sluggish' housing market in 2025: Real estate advisor

6

Good Articles to Share

Attorney slams judge over Trump sentencing: ’Constitutionally crippled’ #shorts

7

Good Articles to Share

This was the ‘crucial’ moment that proved Trump is for 'working people': Journalist

8

Good Articles to Share

WATCH LIVE: Former President Jimmy Carter’s funeral services begin

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

No right Nor wrong Only to Win

So much research done and infos shared ftom teoct .

Big thanx

2019-07-20 11:24