by Koon Yew Yin, the Malaysia philanthropist tycoon

As you all know, the KLCI is striking the historical high and investors have to be more careful in their stock selection. You should be a net seller and do not buy any share unless it is really undervalued. Do not take unnecessary risk.

My reason for writing this is to satisfy my own ego which is my greatest weakness. Another reason is to do some charity by teaching you how to make money from the stock market. In fact, almost all my wealth is from the stock market. I am not a professional analyst and I have nothing to gain if you buy or not. I am aware that I will have no place to hide if you buy it at the current price level of around RM 2.00 and you lose some money.

There are so many criteria for stock selection. Most professional analysts consider the current earning is most important because it is so difficult to predict the future. That is why they are not interested to buy JT now as it is not showing much profit because most of the palms are young. I prefer to accumulate slowly when Fund Managers are not buying.

Reasons to own Jaya Tiasa shares

1. Jaya Tiasa’s major business is timber and plywood. After cutting down the timber, they started planting oil palms in 2002 aggressively. They have planted about 62,000 ha. The average age of their palms are about 5/6 years old. That is why the company is not showing much profit and professional fund managers are not interested. As a result the price has been depressed for almost one year. The current price has formed a base and it is safe to buy it. In fact about one year ago, the company place out 15% of the total issued shares at RM 7.90 before the bonus issue of 2 for every one held. That means the big fund managers have bought the shares at RM 2.63 per share.

See below price chart:

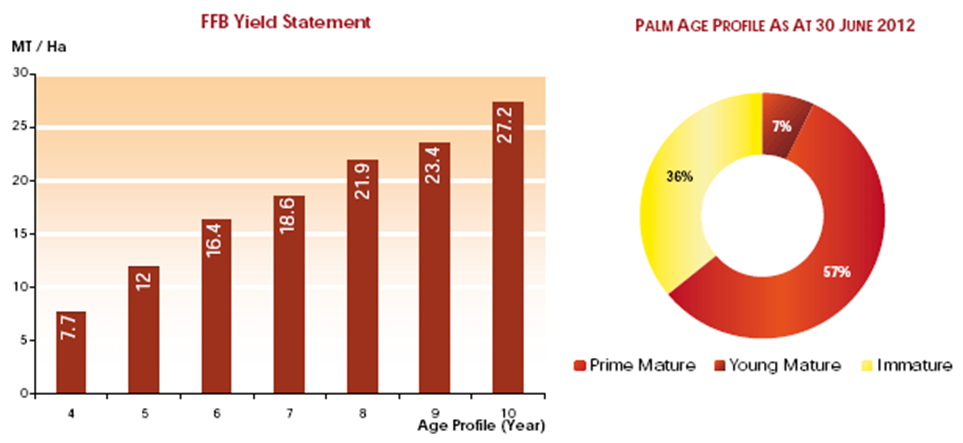

2. If you look at the FFB production / palm age chart below, you can see there will be sustainable FFB production growth over the next 10 years. Among all the criteria for stock selection, sustainable production/profit growth prospect is the most important. When the palm is 4 years old it can produce 7.7 tons of FFB per ha and when it is 10 years old it can produce 27.2 tons. That means it has a production growth rate of about 3.5 times in 6 years. What business can offer you such growth rate?

That is why most of the older plantation companies are cash rich. The younger companies, like JT has to use their cash for the construction of mills and expand their plantation area.

3. The whole plantation sector is so depressed due to its prolong weak CPO price. Like any commodity CPO price will recover. If you look at the 5 years price chart below, you can imagine that it will sooner or later recover. Always buy when people are fearful!

4. Palm oil is largely grown in Indonesia and Malaysia. Fortunately it cannot be grown in China, India and US or EU. Due to continuous population and economic growth, there will be increasing demand for eatable oil. There is absolutely no good reason why soya bean oil is selling at a higher price than palm oil when it is proven that it is not superior to palm oil. Please read my recent article on the Fight the Smear Campaign against Palm Oil.

5. As reported, the price of timber and plywood has increased by about 50% due to the Japanese demand for the reconstruction of the damages caused by the recent tsunami. I will move a resolution in the coming AGM to list the company’s timber business. I believe all shareholders will support my proposed resolution. This will benefit JT shareholders. For example IOI Corp is listing their Property business and IOI Corp shareholder will be given one IOI Property share for every three IOI Corp shares held.

6. As shown in the last annual report, most of the largest top 30 shareholders were financial institutions. The 30th largest shareholder was CIMSEC nominees (Asing) Sdn Bhd Bank of Singapore Limited for Profit Centre Asset Management Limited holding 5,639,916 shares. They all know the company has sustainable profit growth. This is reassuring to me and all serious investors.

7. The total issued shares is 974 million X RM 2.10 = RM 2,045 million plus about RM 500 million bank loan= RM 2,545 million divided by 62,000 ha planted area = RM 41,000 per ha which is comparatively cheap without considering their timber and plywood businesses. The EV per ha for many of the famous plantation companies is more than Rm 100,000 per ha.

Conclusion

:

This share is good for serious long term investors. It has sustainable profit growth prospect for the next many years which is the most important criteria for stock selection. It is not meant for day traders.

Disclaimer: I am obliged to tell you that my family members have accumulated more than 33 million JT shares and I am not asking you to buy it. If you buy, I have nothing to gain and I am not responsible for your profit or loss.

I have the same opinion with Mr Koon that we should invest on a counter with future growth prospect. All the research reports from investment bank are Bull-Shit since TP given based on their own discretion and valuation method. Majority of retail investor will beat the market if all the TP or recommendations are useful. I am going to accumulate JTIASA(4383) start from today. Thank you for your post KCLAU and Mr Koon.

p/s: try to edit the title of “best bet”. We invest on future growth of the company but NOT betting on unforeseen events that with gambling behavior.

[…] As the author I expect readers to comment and query sensibly. Here are my answers to the query submitted on my previous article about Jaya Tiasa: […]

who could really predict what would happen for the next few years time?

The growth rate of 3.3 times does not necessarily translate into company/revenue growth of the same quantum. It can be treated as base rate for plus/minus, the growth rate could be much lesser given some discount for uncertainties, such as the flunctuate down of CPO price over those years.

It will be great if the family can accumulate up to 10% in the company share for retail investor to feel confident. Sometime it can be worrisome if the top 30 is only consist of institutional investors, which capable to hit and run in big chunk, leaving the small player dry and high.

I must thank ZFS for his comment. Jaya Tiasa’s growth rate can be about 3.5 times in 6 years just basing on the FFB production as the palms are getting older. Its profit can be higher or lower depending on the selling prices of its products such as CPO, plywood and swan timber.

All I can safely say is that JT has sustainable profit growth prospect for the next many years. The current profit is poor because most of their palms are young and that is why its share price is so depressed for a long time. Koon Yew Yin

Dear Mr Koon,

If I am not mistaken, the bank loan is about RM 821 million (short term loan RM 372.8 million plus long term loan RM 447.9 million as at 2013 Q3 report) instead of RM 500 million as you said.

Thank you.

This is the reply from Koon Yew Yin through email:

“Dear Lee Fong Yong,

Thank you for pointing out my carelessness in guessing that Jaya Tiasa has about Rm 500 million loan instead of Rm 800 million. Although this amount appears to be fairly large but basing on the open market price of oil palm plantation at Rm 50,000, it represent 16,000 ha. JT has planted more than 62,000 ha and many other assets.

Koon Yew Yin”