Corporate Updates

One Up on Malaysia’s Steel Industry

One Up on Malaysia’s Steel Industry

While there are many well-intentioned contents published on stock forums, some of them are simply based on writers' opinion and understanding may end up become inaccurate or mispresented, so to speak.

That being said, I do not wish to point fingers or lay blames to any parties, and I hope whatever I shared in this article could brighten up our reader’s mind.

To begin with, there are generally two types of steel industries player in Malaysia, namely the manufacturers and/or value add companies, and those who involved mainly in the trading and wholesaling business.

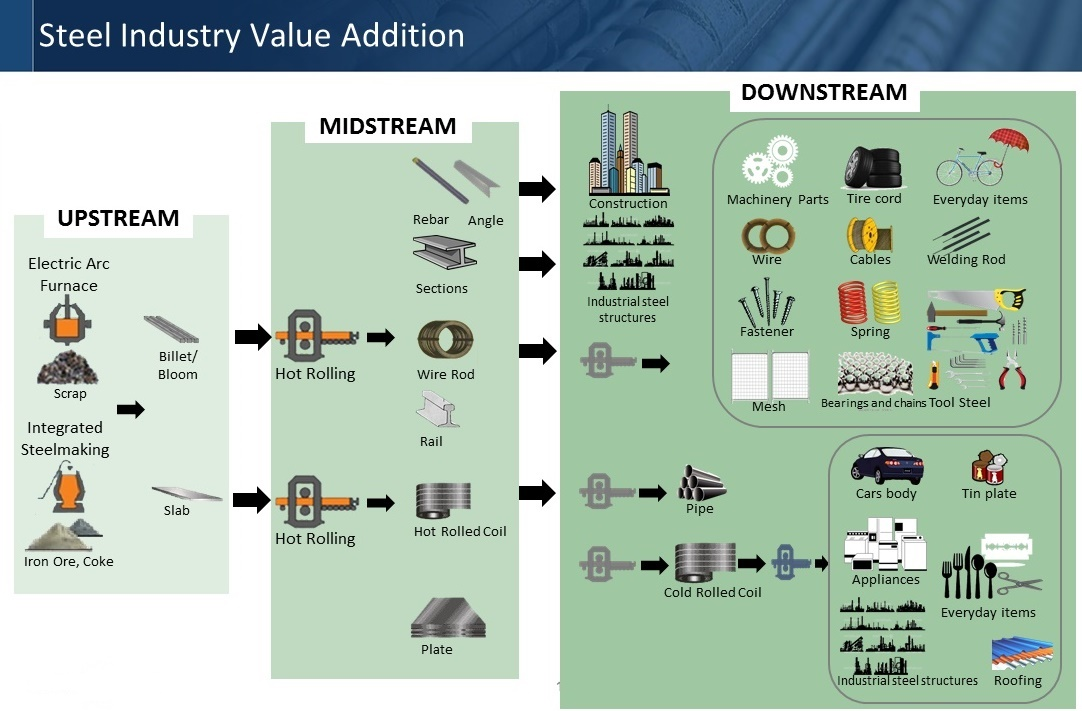

As for the value chain, the photo taken below from Bulatlat illustrated well on how it works.

Generally, Malaysia did not involve much in the iron ore mining industry, as our country’s mineral mining sector recorded a gross output value of MYR3.5 billion, out of which RM1.7 billion is attributable to bauxite and ilmenite mining (2016, Mining and Quarrying Economic Census).

And according to Trading Economics, the mining production in Malaysia had averaged a 0.75% drop from 2011 until 2021. Hence, we do not see much iron mining activities ongoing on Bursa.

While investors would generally refer “steel” prices on CNY-based rebar, which is the first search result one could find when you googled “steel prices”, flat steel and value-added products such as hot rolled coil and cold rolled coil data is relatively harder to be found. Hence, there are many who misunderstood the pricing – which is completely understandable, especially for those who are new to the market.

You could also see that the application of long steel such as rebar and flat steel are much different.

Understandably, the prices for “steel” are constantly fluctuating alongside with supply and demand.

While many could argue that “steel” prices had gone down from its high, the value of construction work done alone in 2022 Q1 in Malaysia had amounted to RM29.5 billion – steel, being one of the key construction materials, is poised to see an increase of demand, and at the current juncture, it is still considerably profitable for steel players in Malaysia.

For manufacturers in Malaysia, they are generally applying to a costs-plus model in terms of factoring their prices. In other words, as long as the management had been keeping a close eye on steel prices and managed their inventories well, the company should remain buoyant against the price fluctuation headwinds, while preparing rigorously for the next upcycle.

For number crunchers, we need to relook at the term “Revenue”, which obviously was made up of 2 aspects for steel companies, namely the volume supplied and selling price of the products.

In weaker steel prices time, the manufacturer or trader could rack up their volume to cover up fixed costs as well as enhance their margins, and during the steel upcycle, they could enjoy both at once. It all comes down to how well the company was managed, especially on the inventory level.

Speaking of which – inventories could make a difference on the profit and loss statement, but for obvious reasons it would depend on when the goods were sold. Do bear in mind, that these inventories are not like your properties, which one could revalue to inflate its bottom line, but instead, it needs to be sold then only its bottom line can be concluded, which is always tied back to the timing of sales.

Of course, for slow moving inventories and those inventories which are below their net realisable value, the steel manufacturers and/or traders may even need to impair or setting up an allowance for impairment on the books!

Therefore, I was amazed when investors are touting the idea of steel companies inflating their numbers by not doing anything on their inventories.

However, for investors, it is always about the return on investment. We all know that the stock market generally had a 6-12 months forward nature in pricing and valuation, and that would very well explain the current valuation of the steel companies. Coupled with hampered investors sentiment, there you go, low single digit PE steel companies.

It is wise for investors to normalize the company profit, and to certain extent – try to wait out for a low for companies who managed their cash flow well.

Oh! Speaking of which, cash flow and debt is another commonly debated issue in the steel industry.

I think many investors may understand the basics of working capital, but not the concept of trade financing. You see, in a capital-intensive business, it is sometimes cheaper to raise a super short-term borrowing of 30 to 120 days in order to secure customers and better margins.

This is common that steel industry, or commodities related companies on Bursa had over a great deal of their debt in short-term trade financing, which is lower in financing costs, as it was prorated.

It is just sad to see that investors are injudiciously and blatantly claiming that steel makers would raise borrowings just to pay dividends to attract investors. Dividends are generally approved by the board members while for final dividends, shareholder's approval needs to be sought. The board members which also consists of independent directors must have closely monitor the cash flow of the company before approving it.

So much for saying debt-for-dividend.

I think investors need to be fair in justifying the profit and loss, as well as cash flow movement of any steel companies in Malaysia before crowning an undervalued or overvalued statement over them. It is simply irresponsible.

Remember, what is undervalued now can be overvalued in 6-12 months’ time, and vice-versa.

More articles on Corporate Updates

Nasdaq-Listed AGAPE Forges Ahead with Sustainable Energy Business

Created by pinchofsalt05 | Nov 08, 2023

Subang Parade Contends with Unprecedented Flash Flood After Heavy Rainfall

Created by pinchofsalt05 | Nov 06, 2023

Rinani Group Berhad Acquires 5.85% Stake in Malaysian Genomics

Created by pinchofsalt05 | Jul 15, 2023

Unleashing the Power of Speed: New Launch Amazfit Cheetah Sets the Pace for Run Performance

Created by pinchofsalt05 | Jul 03, 2023

Discussions

1 person likes this. Showing 3 of 3 comments

As raider say b4....Steel industry is cyclical and for msia steel industry.....the players are aggressive & speculative.....they tend to ramp & speculate on their inventories more than their reqn, when steel price is going up and dump in aggressively when price is going down loh!

This scenario is true as most of the steel player tend to borrow heavily on their trade & give big credits to their customer loh!

If want to succeed in investing in this business in the long run....better buy into strong players which are net cash rich and will not be affected by heavy debts loh!

2022-08-10 13:10

Dengar baik baik, what raider said....very important to note....when u invest in cyclical steel stocks loh!

As raider say b4....Steel industry is cyclical and for msia steel industry.....the players are aggressive & speculative.....they tend to ramp & speculate on their inventories more than their reqn, when steel price is going up and dump in aggressively when price is going down loh!

This scenario is true as most of the steel player tend to borrow heavily on their trade & give big credits to their customer loh!

If U want to succeed in investing in this business in the long run....better buy into strong players which are net cash rich and will not be affected by heavy debts loh!

2022-09-12 08:21

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

Mercury Securities Research

2

HLBank Research Highlights

3

PublicInvest Research

4

RHB Investment Research Reports

5

MQ Market Updates

6

RHB Investment Research Reports

Market Strategy - Data Centre-Artificial Intelligence Party Pooper

7

MQ Market Updates

8

黄金十年-延续篇

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Lam Ah

Very detailed article, thank you for sharing

2022-08-10 13:00