https://dividendguy67.blogspot.com

Bitcoin - understanding the Options Implied Volatility

Introduction

I often get this question - how does Options Implied Volatility (IV) predicts future returns on its stock/ETF?

Let me illustrate numerically what it means, using IBIT as example.

Introducing IBIT

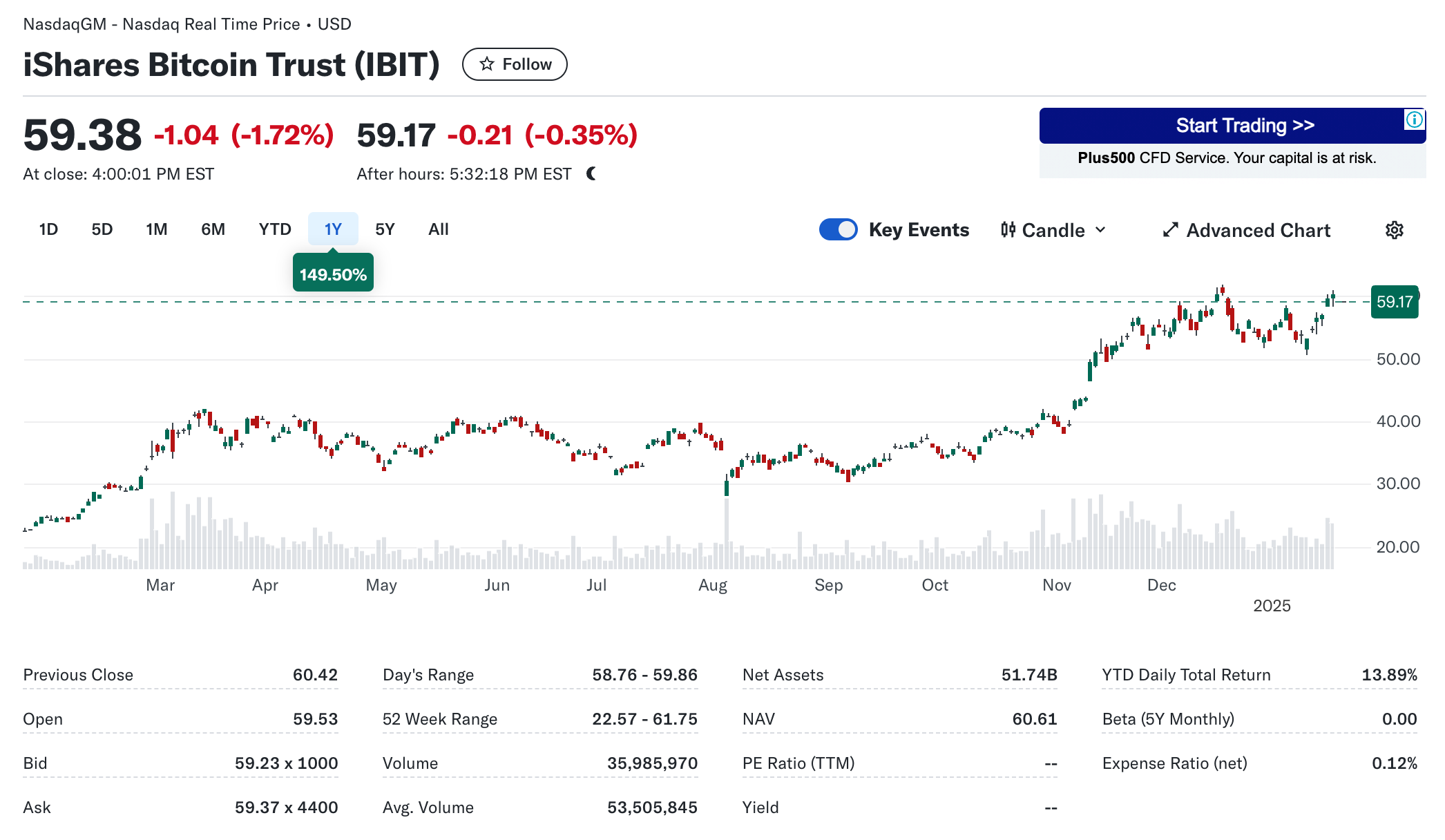

IBIT is a spot Bitcoin ETF that trades in the US market.

This is the most popular and fastest growing Spot Bitcoin ETF in the entire world. Today's trading volume alone is 35.9 million shares, or turnover of $2.3 billion! (and it's not a big day). It closed at $59.38.

It's Net Assets is valued at $51.7 Billion! This means it holds $51.7 Billion worth of Spot Bitcoin. As Bitcoin price rise 10%, IBIT price rise 10% and vice versa. If the price are mismatched, then, arbitrageurs and traders like myself can take advantage of the differences between the 2 prices and in reality, there are algos, robots, and other traders who constantly on the lookout to take advantage of the differences in prices in different markets for the same product. Note Bitcoin trades at 248 different exchanges around the world, including this one.

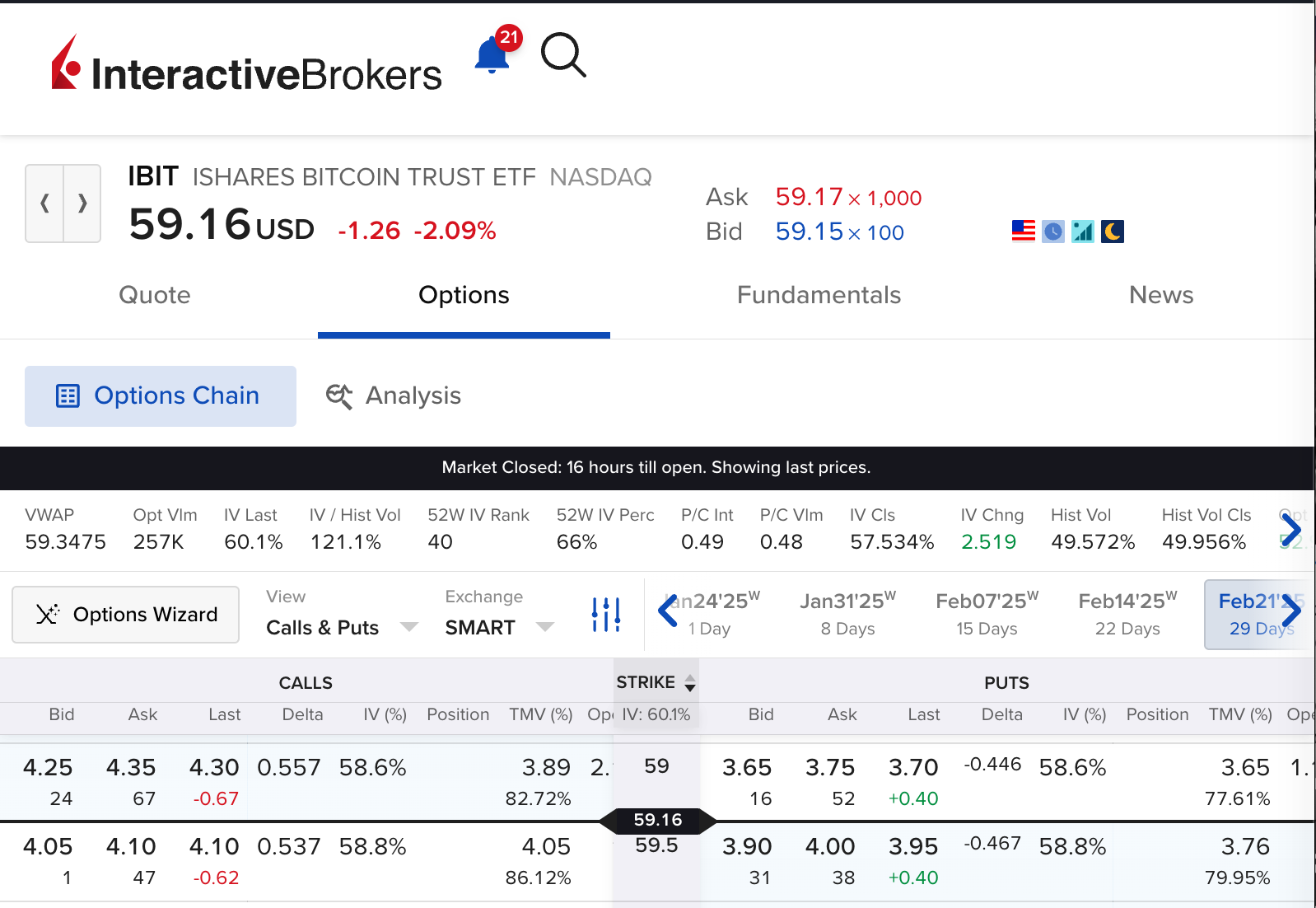

Looking at IBIT Option Chain

Note that 1 lot of Option equals 100 shares.

A background - not all Option Chain are equal especially to their Bid Ask spreads (and by implication, volume and open interest).

Above, IBIT Bid Ask spread is decent, ranging 5-10 cents after market close - the spreads are typically tighter during US options trading hours (the options market closed at 5AM KL time). I took this screen short after market close - so, the volume of the bid and ask (the small number below the Option price) has shrunk drastically. If you watch the Option chain during US trading hours, you will see massive volume of bid and ask for IBIT. Like several hundreds, thousands and even tens of thousands. This makes IBIT Options one of the most popular and larger Options market together with MSTR stock options.

In fact, typically, there are a LOT more monies to be made trading the derivative market like Options, than stocks. If you trade smart and responsibly, it reduces your risks substantially, giving a higher Sharpe ratio compared to stock only traders. However, the converse can happen too, if you don't know what you are doing and size irresponsibly.

Now, I want to share with you, how you could take advantage of Options market if you think Bitcoin expected returns over the next 12 months is only 18% p.a., much lower than 60% in 12 months time. If you are right, you can make a LOT of monies following these "standard" actionable steps

Step 1. Start first by short selling 1 $59.5 Call and collect $4.07 (mid price between $4.05 and $4.10). Total cash collected from shorting = $407 (less $1 broker commissions).

Step 2. Wait till 21 Feb expiry (29 days away).

Step 3. Check IBIT shares by expiry date. Let say Bitcoin does exactly what you predicted i.e. just up 1.5% a month or 18% per year. So, let say your view is true and IBIT share price rise from $59.38 x 1.015 = $60.27.

Step 4. Get assigned 100 shares short of IBIT at $59.5 after 21 Feb expiry date. You are now short $100 shares of IBIT at $59.5

Step 5. Buy back at the Open Market at $60.27 at a small loss of $0.77

Step 6. But remember, you collected $4.07 earlier. So, you can net the loss of $0.77 against the $4.07 you collected earlier, giving you a net profit of $3.30 i.e. you just pocketed a cool net profit of $330!

Step 7. Repeat this for 12 months - make $3.30 x 12 = $39.60.

Step 8. Note you didn't outlay or buy anything - you have always shorted first and then buy back later.

Step 9. Your annualized returns then becomes 39.60/59.38 = 66.6% per year!

My question to you

Do you think, the Options market will hand 66.6% annualized returns to you just so easily?

If so, contact me - I have a golden bridge to sell to you that will return you more than 66.6% per annum returns!!!

You should still make decent returns selling ATM options but if Bitcoin and IBIT share price explodes, you will stand to lose a lot of monies. The reason the market is willing to give you a chance to earn 66% is because the market believes Bitcoin price will be very volatile in the coming 12 months. Which is why I predict that Bitcoin / IBIT future returns over the next 12 months could be in the range of 60% +/- 20%, the range indicated by the Options Implied Volatility. Most of the time, this is a decent estimate, but sometimes, it can be wrong too.

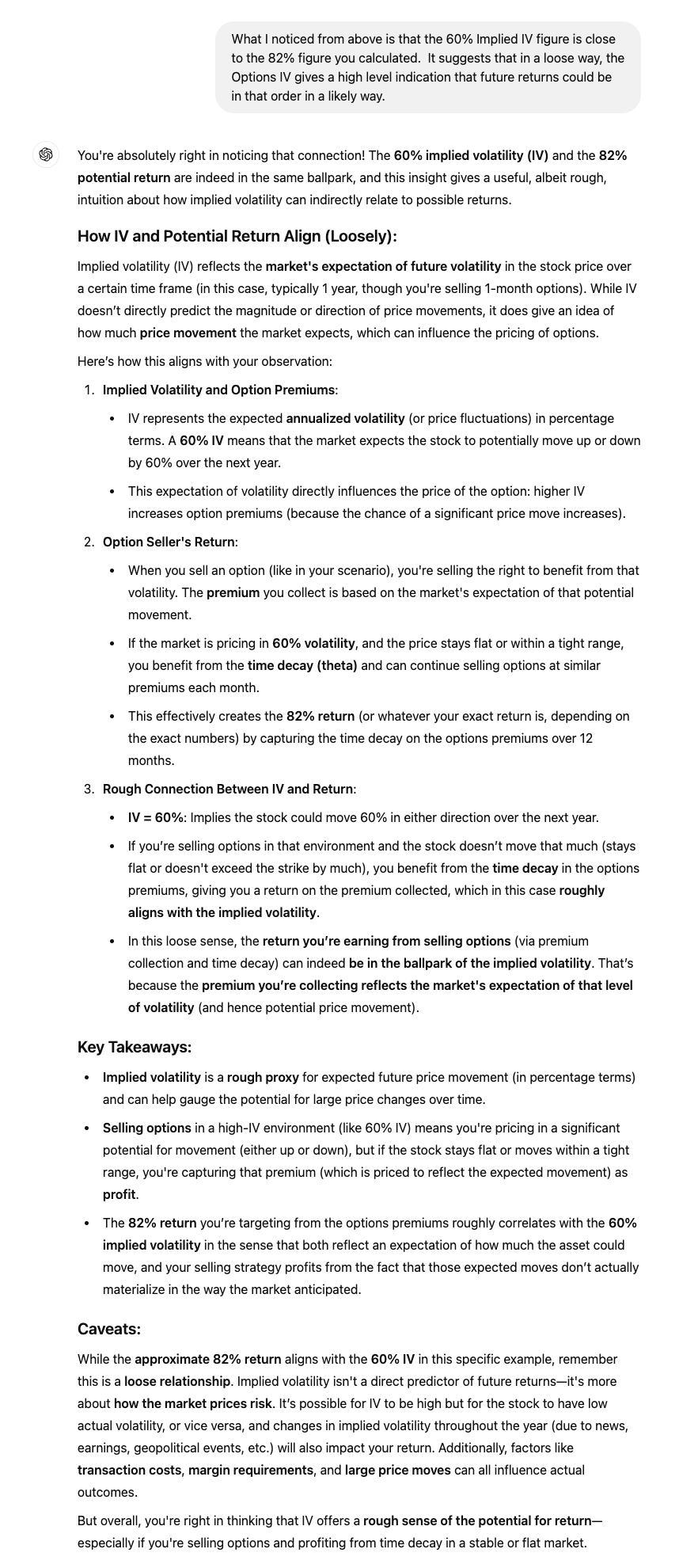

My check with ChatGPT

Summary and Conclusion

There is a "rule of thumb" amongst seasoned Options traders, that the Implied Volatility of an ATM Option gives a rough (loose) estimate of the potential size of the stock's long term expected returns over the next year.

This is simply because of the way the Option's Implied Volatlity is calculated.

And surprisingly, over the long term, it's a darn good estimate!

I have also shown you a practical way to take advantage of it, if you are right and the Options market is wrong!

However, I must caution you - expect that most of the time, you are wrong and the market is right!

And this is what is meant by - "there are no free lunches".

There is no free lunches in the Options market.

Trade safely!

Disclaimer: Not a financial advise. Just a random guy on the Internet. You are always responsible for your own trading and investing decisions.

More articles on https://dividendguy67.blogspot.com

Happy January! Trump inaugurated, account new all time highs

Created by DividendGuy67 | Jan 22, 2025

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

RHB Investment Research Reports

2

3

HLBank Research Highlights

4

5

TA Sector Research

6

Mercury Securities Research

7

MQ Market Updates

8

Double Swords 双剑论股

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....