Intelligent Investing

Timber to furniture - The thing with currency, on value chain, Hevea, Homeritz & more

It is impossible to avoid the discussion of furniture stocks without touching the topic of currency. That is understandable as they are all export stocks and any changes on currency will potentially impact their earnings.

However investor needs to selectively choose where they should put their attention on when it comes to analysis. The issues with being too obsess with analyzing currency are:

- It is something a company has no control on & it doesn't tell you a thing about management capability or industry dynamic

- Be it a forex gain or loss, it shouldn't be part of the valuation to begin with. Valuation should only be based on cash flow generated from core operations

- You are trying to predict the unpredictable. You chances of predicting it correctly is same as mine - 50/50, like a monkey throwing darts

- 10 years later when you look back, for all the gains and losses caused by currency, it will only have a drop in the ocean effect on the true value of these stocks

Trying to predict currency impact on earnings raises another interesting question.

If the skills required to predict currency movement = X, then

predicting currency movement + the impact on earnings + how the market will react + how big the stock price will moves is going to require 2X of skills

You get the idea. It will be harder not easier.

Going by that reasoning, if you are confident with your ability to predict currency movements, you should be trading forex because the probability of winning is higher.

Another scary thing is investors are using the most recent 2015 figures for reasoning & extrapolation. A year where thanks to MYR depreciation, everything is inflated from top to bottom. Currency depreciation improves selling price which in turn inflate revenue, operating margins, increase asset turnover, balloon ROIC, and turbocharge EPS when 'Other income' is added onto it. You are running a high chance of overestimating value by using these abnormal figures as the base year.

*******

Furniture stocks or export stocks are the common name categorization given to stocks that sells timbers or manufacture furnitures. Categorization simplify things and make it easier for us to understand but it is far from saying they are all the same.

You probably seen many investors or analysts comparing Heveaboard to Homeritz. Traditionally Hevea had always been trading at a lower multiples (P/E, P/B etc) compare to Homeritz so analysts comparing both will always makes Hevea looks undervalued.

Calling Hevea undervalued isn't the issue as long it appears so in your valuation, but trying to compare Homeritz to Hevea seems a little strange if we examine the nature of their business and their numbers.

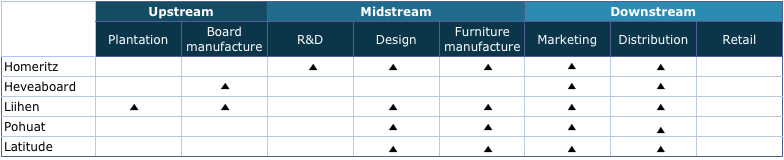

This timber/furniture industry value chain is not precise but does the job. Here:

Upstream - Everything from planting trees to converting them into particleboard or other types of board.

Midstream - All the effort undertaken from R&D, design etc that turn particleboard into end product - Furnitures.

Downstream - Activities of selling & delivering to customers.

All of the these companies' businesses are focused along the mid & upstream of the chain. They all have marketing & distribution divisions but those are not their core operations.

Coming back to Hevea. Hevea generate around 50% of their revenue from manufacturing particleboard and the remaining from RTA or Ready to Assemble furniture. You can argue technically they are selling furniture albeit those furnitures are not assembled, customers have to do it themselves.

Homeritz on the other hand, pour all of their focus into R&D, design and manufacturing high end upholstered furnitures for their customers.

Numbers tell the story.

These are the fixed assets extracted from the reports. When you look at plant, machineries & equipments (PPE), Hevea needs around RM170 mil of PPE to generate RM503 mil of revenue, or 2.95x. In contrast, Homeritz can generate RM146 mil of revenue with only RM4 mil worth of PPE. That's 32.95x.

Is that because Hevea is inferior? No, it is simply because they are in a different business. For a particleboard manufacturer like Hevea, the amount of machineries they need to chip, flake, dry, mat forming, hot pressing, sanding, sizing, laminating, to turn timber into particleboard are a lot.

In comparison, the machineries you need to turn particleboard into an upholstered sofa is very little. Sanding, polishing and some cutting tools should do the work. In saying that, the workmanship needed to turn the sofa into a high-end quality product will translate into higher expenses too. Pohuat & Latitude would have more similiarities to Homeritz than Hevea, while Hevea's business is more similar to Mieco.

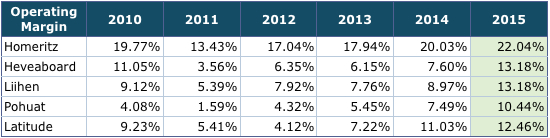

When you look at their operating margin it paints the same story.

Homeritz has always been the leader in profit margin. Again it isn't because Hevea is crap, it is just that they are selling undifferentiated products - particleboard. They can only achieve higher margin through operational efficiency. Whereas Homeritz can maintain a higher margin by focusing on the high end niche market. You can increase the selling price of a high-end sofa but extremely hard for particleboard.

You might have notice operating margin across all the companies increase substantially in 2015 compare to previous years, ranging from 50-100% jump in margin. Customers don't suddenly get excited by paying double for particleboard. This is how currency inflate the numbers from top to bottom. You will be up for a big surprise if you think 2015 is a new era.

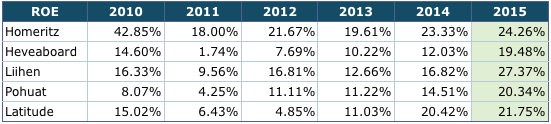

When you add asset turnover into the picture, you started to grasp the full picture of how the numbers came to be.

And again you just need to be careful with the asset turnover for 2015 because the denominator of the equation (Revenue/Total assets) has already been inflated by currency. However across the 5 years ratio you will have a good sense where it should be.

When you have the profit margin and asset turnover, you will have ROE.

******

The true value of a stock does not change much from year to year. That is also the case for this industry.

Dig into the business to understand what drives the numbers and how those numbers drives valuation. When the market sentiment is awash with currency horror & excitement, understand how the business is creating value is the only thing you can anchor on. What really matters in the end is how the business adds value, not what the conversion rate is.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Intelligent Investing

Discussions

21 people like this. Showing 27 of 27 comments

This is best:

The true value of a stock does not change much from year to year. That is also the case for this industry.

Dig into the business to understand what drives the numbers and how those numbers drives valuation. When the market sentiment is awash with currency horror & excitement, understand how the business is creating value is the only thing you can anchor on. What really matters in the end is how the business adds value, not what the conversion rate is.

2016-05-21 00:05

Ricky, if your article can come out few days early, then it would be even better to me :)

2016-05-21 01:32

Based on the analysis above, homeriz seems to be on par/slightly better compared to the rest of the competitor but why this counter couldn't go up/on par with those competitor?

2016-05-21 14:01

@alex88812 - Because valuation. Homeriz has the highest valuation of them all.

A good business is not necessary a good investment.

2016-05-21 14:32

No offense Ricky, just to add: Numbers do not necessary paint everything. One has to look at both quantitative and qualitative analysis. For example, some companies have not been doing well in some years due to macro changes, not the business itself:

"We took a long term major USD loan to finance the expansion, but were unfortunately hit with the 2008/2009 financial crisis soon after that and were forced to restructure our loan facilities. We were saddled with high

financial costs and repayment obligations and had to operate

under an extremely tight cash flow regime."

I always liked Icon's articles because he focuses precisely on both.

2016-05-21 14:50

And also, I would suggest it's better to add CFFO / FCF in the article if you really want to do a comparison. This eliminates forex gain / loss and can give a clearer picture.

Regardless, well done. Keep up with the good work.

2016-05-21 14:55

Hevea and homeritz are very close in terms of valuation, FCF/price and CROIC.... just that homeritz is in a better business compare with Hevea. This is my opinion.

2016-05-21 16:20

As making investment in stock market, one must think like a businessman. Doing all possible studies & analysis to know where the market & money are as well as the risks & competitions of the businesses.

Forex is part of business factors which all export companies can't avoid to consider when making business decision. Same should apply to investment decision by considering the short & long term effects from the fluctuation of RM.

After all, you need to make a choice based on your available funds & personal preference & risk stomach.

To buy or not to buy.

If to buy, which is the better one to invest.

Please remember, buying a good company at high price may not be a good investment.

However, I do agree that a good management with good business should be able to contain the risk of forex fluctuation.

So, when all seem like also good, then one should consider is the quality of the management. Is the company rewarding its shareholders by giving out consistent dividends over the past years?

Dividend policy & payout will be my main consideration when making my investment decision in selecting furniture/export stocks.

2016-05-21 18:40

Forget to say, well done again, Ricky. Thank you for sharing such great article, please keep it up.

2016-05-21 18:41

haha using profit margin to say that the company is better than another company? Not really a good measure.

Let say company A earning revenue RM1 but earn RM0.25 compare to a company which have RM10 revenue and profit RM2. Isnt it company A better? Profit margin not a best thing to measure a company.

Asset turnover not a good measure? Why say the asset inflated by currency. All of the furniture company balance sheet have been inflated, not only homeriz. Then why u say it is not a fair comparison? Because homeriz lower than other furniture company? then it is not a good measurement?

2016-05-22 00:37

Well done Ricky.

Should consider to include other similar listed company such as Sernkou for evaluation and comparison as well.

Tks.

2016-05-22 00:44

Yes pingdan, company A profit margin is 25%, another company margin is 20%. Company A is better, and im using profit margin formula profit/revenue.

2016-05-22 06:56

Few things to consider/determine:

1. Is the company earnings moving to higher levels - next couple of years (due to sustainable structure competitiveness advantage)

2. Did the share price already OUTRUN the fundamental due to sentiment.

2016-05-22 10:01

pingdan, if company A and B running the same type of business, then obviously company A is better. But more important is how much of profit can be generated from invested capital (ROIC). In my opinion, that will be a better benchmark than ROE.

2016-05-22 10:48

Sosfinance, that's the thing, everyone talk about rate/margin/%/return, how about future business progress. Anyone has better insider business vision on future export prospect?

2016-05-22 10:51

ricky yeo, i dun think profit margin is the only way. if let say company b is grow faster than company a although the profit margin is slightly lower than company A, i disagree with you point. but if both company is grow in the same pace, yes company b is better than company.

Another more thing to consider is share price. if a company with high profit margin is far far way expensive then another company, i will choose another company with lower margin. So many things to consider before buying a share.

2016-05-22 13:07

Hevea vs Homeriz vs Liihen. Is nature of business/core business as important or more important than financial analysis in fundamental analysis? Based on the above article, Hevea is ....

2016-06-01 14:24

Post a Comment

Featured Posts

Apps

Top Articles

1

Kenanga Research & Investment

2

3

BFM Podcast

4

5

BFM Podcast

6

BFM Podcast

7

RHB Investment Research Reports

8

PublicInvest Research

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

probability

very interesting Ricky...good to have analytical minds like you in i3.

2016-05-20 23:45