Future Potential of Petronm

Petronm Part 5

davidtslim

Publish date: Thu, 10 Aug 2017, 02:01 AM

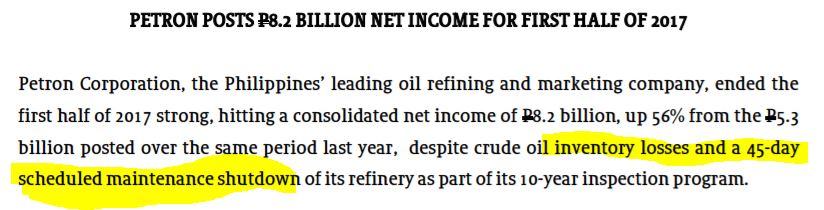

As some of you may know, Petron Corp (Philippines) has released media release for preliminary result which includes profit contribution from its subsidiary (Petron Malaysia) (73.4% stake). However, they did not provide breakdown for Petron Malaysia operation income in this release. The result of Petron Cop can be accessed at http://www.petron.com/web/Media/uploads/08_08_17_-_Media_Release_-_Petron_Posts_P8.2_Billion_Net_Income_for_First_Half_of_2017_._._.pdf

Let go through one of the key figures of this media release result as below:

Source: Media Release of Petron Corp (link above)

It reported a net income (profit) of Peso 8.2 billion for first half of 2017. The reported Q1 net profit (income) is Peso 5.6 billion. As a result, the consolidated Q2 profit for Petron Corp is P2.6 billion (8.2-5.6). What catching eye from this media release are inventory losses and a 45-day maintenance shutdown of its refinery plant. These two factors explain the decline in its net income from P5.6 to P2.6. I expect the refinery segment contributes high portion of profit in its Q1 result (due to high refinery margin) and the 45-day shutdown may has significant effect. Nobody knows how big the effect from its refinery shutdown to Petron Philippines results. One point I would like to highlight is Management told us that there is NO shut down for Petronm in 2017.

What I try to estimate in this article is the possible profit for Petronm from the Petron Corp result.

To be conservative, let start with worst case scenario for Petronm profit estimation. First we start with inventory/stock loss calculation

1. Worse case inventory/stock loss (Management stated in AGM they keeps 18-21 days stock) – I assume 22 days

Stock loss = 48k barrels x 22 (48.2 – 52.95)

= USD -5.016mil

= RM-21.57mil

2) Lower Refinery margin (lower down from USD5.3 to USD5.0) in a quarter (based on its regular throughput per day of 48k). Management also told us in AGM that its refinery currently running at around 60%.

= 4.368mil barrels X USD5.0 (estimated profit margin per barrel)

= USD 21.84mil

= RM 93.91mil

Throughput data from 2016 AR as shown in figure below (91 day in Q2 X 48k = 4.368 mil barrels)

3) Lower retails segment contribution (even though Ramadan month was in June and Q2 is 91 days as compared to 90 days of Q1), but let’s assume it performs 5% lower than Q1’17

= 100 mil (part 1 article assume 105 mil)

Net Gross Profit = -21.57mil + 93.91 + 100

= 172.34mil (part 1 article estimate 186.9mil)

4) Assuming higher operating cost and same finance cost of 5% more than Q1’17 (from Q1 report), Q2 operation cost and finance cost is = 36.33 mil

Net Profit = (172.34-36.33) mil = RM136.01 mil.

(Actually it should has lower finance cost in Q2 as last quarter it paid up 56 mil of loan that lead to lower interest cost)

Assume the same tax rate of 26.9% as per last quarter,

New possible lower or worse case Net Profit = RM136.01mil deduct 26.9% tax

= RM99.42 mil

RM99.42 mil --> EPS of 36.83 sen.

From this media release, Petron group profit is P2.6 billion and this translate to RM221 millions. From Q1 data, Petronm contributed about 30% of the overall net income. From estimated RM99.42 mil net profit, its contribution will rise to about 45% (99.42/221 x 100). This is the worse case scenario profit that I can think off for Petronm. The possible reasons higher contributions of Petronm on the overall Petron Corp profit are as below:

1. 45-days shut down of refinery

2. High inventory loss in Petron Corp (Philippine) as it refinery shutdown for 45 days (its Bataan refinery rated capacity is 180kbpd which should keep higher number of stock)

3. Overhead cost in refinery factory (due to it still needs to pay salary, electricity bill etc during the shut down)

4. Sub-contractors cost for the maintenance work

Let us go through another figure from the media result as below:

The figure highlighted is the oil sales volume which worked out to be 26.7 mil barrels as compared to 26.2 millions barrels last quarter, up about 500K barrels. Malaysia operation contributes about 30% of the total operation hence about 150K barrels increment is expected come from Petronm.

From this figure, it is expected some small growth in the income from retails as its sales volume are increasing supported by 16 news stations and 4 millions+ loyal mile members (also Ramadan)

Another point I would like to highlight is the inventory/stock loss is “accounting loss” or on paper loss, not the real loss as the stock will be converted to refined products from time to time. Furthermore, I would like to stress that the refinery margin (crack spread) data in Q2 should allow Petronm to maintain its strong profit as per Q1.

In fact, the inventory/stock loss will be recovered back if the Crude oil price closed at a price higher than USD48 at the end of Sept (Current Brent oil is trading at USD52++, so about +ve USD4 gain per barrel in their stock). In short, there will be similar amount (RM20 mil++) of stock gain in Q3 if crude oil price closed at USD52++.

The positive factors that I can think off for Petronm in Q2 are summarized as below:

1. Petronm commercial (jet fuel) and lubricant sectors showed strong growth (more than 10% in Q1’17) and may drive higher retail profit in Q2’17.

2. 91 days in Q2 as compared to 90 days in Q1 should help in retail and refinery business

3. Forex gain due to appreciation of RM against USD

4. Lower finance cost as it paid up RM56 mil debt. It may turn net cash company when the coming quarter result released

5. 18 new stations have been opened and high fuel oil refinery margin (http://www.reuters.com/article/refineries-fueloil-idUSL3N1JH360)

Risk

There maybe some other cost or expenses that out of my estimation for Petronm in Q2. Inventory/stock loss maybe one of them but this can be recovered when converted to product and become stock gain in Q3 (if crude oil higher than USD48).

Summary

1. I would say Petronm is doing pretty well in the past two quarters (41 sen and 40 sen EPS in Q4’16 and Q1’17). As long as it can produce 33 sen EPS or above in coming quarter, it actually achieve a growth of profit of nearly 50% YoY (vs Q2 2016).

2. If you check Petronm's Q3'16 result (17.33 sen, 46 mil), then you will know how big the potential of Petronm coming Q3'17 result improvement in view of stable retails and strong refinery margin (crack spread) in July and Aug.

3. For medium term investor, I expect Q3 result to be robust as stronger refinery margin (crack spread) can be observed from July to August. Q3 result is expected to be released in Nov.

4. Petronm currently trading at PE 7.37 with price of RM8.99. Simple comparison with its peers like Petdag (PE 24) and LCTITAN (forward full year EPS of 26.32 sen for price of 4.43, PE more than 15). Even you compare with its mother company Petron Corp also trading at PE 11 in Philippine.

5. The quality of earning is supported by strong free cash flow (FCF) of RM300 mil++ per year. This FCF has helped to pare down its debt to RM251 mil from more than RM1000 mil in 2014. With this cash flow rate, I expect Petronm can become debt free company by end of the year with decent dividend payout.

You can get my latest update on share analysis at Telegram Channel ==> https://t.me/davidshare

Disclaimer:

This writing is based on my own assumptions and estimations. It is strictly for sharing purpose, not a buy or sell call of the company.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Future Potential of Petronm

Discussions

6 people like this. Showing 31 of 31 comments

Thank you David again for this well thought write up and it makes great sense ! Will sailang all.......

2017-08-10 05:06

Probability, what do you think and anything you would like to add or highlight here ?

2017-08-10 05:08

Thank you David for your calculations. My estimate wasn't accurate previously as I did not account for the retail sector..shall refer to your calculations and tune for future reference.

2017-08-10 07:07

Appreciate the hard work, but how come petron Phillipines shut down half a quarter but sales volume still can maintain?

2017-08-10 07:39

Plant closure is a one off event. Just imagine the state of petronm after 6-12 months. Investors need to hv more patience

2017-08-10 08:12

Tqvm david.

Worst case oledi so good earning !

Can't imagine the actual result leh

2017-08-10 09:10

Itu dia david. Ramai analysts pun tak pandai buat analysisa macam you.

Ribuan terima kasih.

2017-08-10 09:50

Thanks David, sold my house and pants already, waiting for money to transfer then will sialang

2017-08-10 09:55

Thanks david, is the mandarin version also on the way out ? Guess will reach more valued investors if chinese next version is written.

2017-08-10 10:05

Not a Petronm or HRC investor, but enjoyed reading you articles. Well written article backed with facts and good reasoning.

Keep up the good work David!!!

2017-08-10 11:10

Game over already. Theme play for oil refining finish already. Don't talk about petron cock any more.

2017-08-10 15:39

Thanks for the hard work. I am in Petron for the long term, because I think it's leaner operation will do well in weak economy, in addition to its integrated operation.

2017-08-10 15:55

Thanks David for your write up. Sure appreciate yr hard work. Will watch Petronm to buy a few lots for long haul. Already into HRC 2 months ago. Keeping for long haul too

2017-08-10 21:03

The below article is very good to read..

Wall Street Is Beginning to Take Note of Escalating Tensions With North Korea

http://www.nbcnews.com/business/markets/why-stock-market-taking-trump-kim-war-words-its-stride-n791551

2017-08-12 23:54

Post a Comment

Featured Posts

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2025-01-31 15:50:00

TURTLE SYSTEM 20

10 Mins

BUY

2025-01-31 15:50:00

TURTLE SYSTEM 55

10 Mins

BUY

2025-01-31 15:50:00

TURTLE SYSTEM 55

5 Mins

BUY

2025-01-31 15:30:00

EMA 5

30 Mins

BUY

2025-01-31 15:30:00

TURTLE SYSTEM 20

30 Mins

BUY

Apps

Top Articles

1

THE INVESTMENT APPROACH OF CALVIN TAN

2

Stock Market Enthusiast

Feng Shui Market Outlook for FBM KLCI in the Year of the Wood Snake (2025)

3

Dragon Leong blog

4

Bursa Stock Talk

5

Kenanga Research & Investment

Oil & Gas - Dissecting Petronas and Trump's Impact on the Sector (OVERWEIGHT)

6

Rakuten Trade Research Reports

7

TA Sector Research

8

My Trading Adventure 2025

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

John Lu

Brilliant!! I dont have Petronm but I sialang in HYC!!

Petronm up, HYC also follow

2017-08-10 02:35