HLBank Research Highlights

Retail Strategy - Volatile and Newsflow-driven Quarter

The lingering worries on trade war uncertainties, slower economic growth potential and inverted yield curve may continue to dampen the market tone moving forward. However, we see potential catalysts such as (i) recovering firmer Brent oil prices, (ii) optimism in construction sector, (iii) export-oriented companies amid weakening bias USD/MYR trend and (iv) defensive (consumer) and high dividend yielding corporates. Hence, we believe retailers will need to cherry-pick stocks for potential winners under the abovementioned sectors. We like (i) O&G: SAPNRG, EATECH, (ii) construction: KIMLUN, KERJAYA, TRC, GFM, (iii) export-oriented: SUPERMAX and (iv) defensive: DKSH, UCHITEC.

Market Review

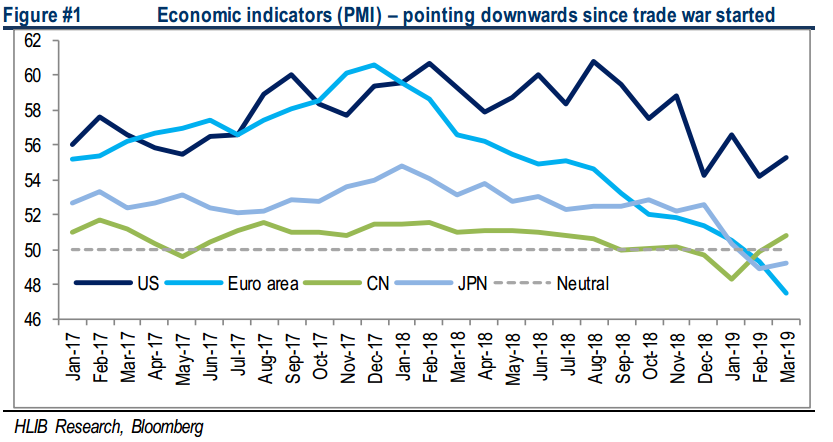

Trade war(i) uncertainties still persist… The prolong trade disputes between the US and China has started since mid-2018 and has been contributing towards weakening business sentiment and slowing economic activities globally. Meanwhile, economic indicators globally are weaker since trade war started; PMI manufacturing (Figure #1) in the US, China, Japan and Eurozone have been showing declining signs over the past 6 months.

…global growth forecast slashed by the Fed and dovish monetary policy… With the weaker GDP data from US and China in 4Q18, major central banks have slashed their forecast for 2019, including the Fed, which recently slashed the economic forecast for 2019 during the FOMC meeting and reduced its interest rate outlook from 2 times to zero in 2019. This is being viewed as dovish and could be suggesting to the market participants that an economic slowdown could be setting in.

…triggered an inverted yield curve(ii). The 10-year Treasury yield has weakened against the 3-month bond yield, forming the inverted yield curve after the FOMC meeting, which led to a sell down in banking heavyweights.

(i) Trade war has not completely settle, however trade discussions are claimed to be progressing well between US and China. (ii) Inverted yield curve (10-year vs. 3-month) may point towards a recession in the next 6-24 months on a 4 out of 7 occasions (Source: Bloomberg)

Source: Hong Leong Investment Bank Research - 11 Apr 2019

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

2024-11-16

SUPERMX2024-11-15

SAPNRG2024-11-15

UCHITEC2024-11-14

EATECH2024-11-14

GFM2024-11-13

SAPNRG2024-11-13

SAPNRG2024-11-13

SAPNRG2024-11-13

SAPNRG2024-11-12

KERJAYA2024-11-12

KERJAYA2024-11-12

KERJAYA2024-11-12

KERJAYA2024-11-12

KERJAYA2024-11-12

KERJAYA2024-11-12

KERJAYA2024-11-12

KERJAYA2024-11-12

KERJAYA2024-11-11

KERJAYA2024-11-07

KERJAYA2024-11-07

KERJAYA2024-11-07

SUPERMX2024-11-07

SUPERMX2024-11-06

KERJAYA2024-11-05

KERJAYA2024-11-05

KERJAYA2024-11-05

KIMLUNMore articles on HLBank Research Highlights

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

3

BFM Podcast

5

BFM Podcast

6

BFM Podcast

7

8

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....