iVSA Stock Review

Holistic View of Top Glove with Fundamental Analysis & iVolume Spread Analysis (iVSAChart)

Is Top Glove Share Price Ready for a Break Through?

Background and Core Business

Established in 1991 with only one factory and three production lines, Top Glove has since grown by leaps and bounds to become the world's largest rubber glove manufacturer. It was listed on the Malaysian bourse, Bursa Saham Kuala Lumpur on 27 March 2001. In a short span of slightly more than a year, on 16 May 2002, Top Glove Corporation Berhad's listing was successfully promoted from the Second Board to the Main Market of the Kuala Lumpur Stock Exchange.

Renown for producing high quality gloves at an efficient low cost based on its time-proven Business Direction, Top Glove offers a wide and diverse product range, fulfilling demand in both the healthcare and non-healthcare segment. It serves a network over 2,000 satisfied customers across more than 195 countries. With its eye on the next level of success, Top Glove now aspires to increase its global market share from 25% to 30% by 2020. It is also aggressively expanding its business scope and on the lookout for M&A opportunities in similar and related industries.

Based on Financial Year (FY) 2016 full year results, Top Glove achieved RM 2.89 billion turnovers, which is considered to be a large enterprise based on turnover value. Other aspects of the company’s latest financial results are illustrated in the table below.

|

Top Glove (7113.KL) |

FY 2016 |

|

Revenue (RM’000) |

2,888,515 |

|

Net Earnings (RM’000) |

361,051 |

|

Net Profit Margin (%) |

12.50 |

|

Return of Equity (%) |

19.71 |

|

Total Debt to Equity Ratio |

0.22 |

|

Current Ratio |

1.99 |

|

Cash Ratio |

0.72 |

|

Dividend Yield (%) |

4.63 |

|

Earnings Per Share (Cent) |

28.77 |

|

PE Ratio |

17.27 |

Over the latest past 6 Financial Year (FY), Top Glove’s revenue has in general increased from RM 2.05 billion in FY2011 to RM 2.88 billion in FY2016, which translates to a 40% increase in 6 years. However, Top Glove experienced a slight decreasing revenue trend during FY2012 to FY2014 from RM 2.31 billion to RM 2.28 billion.

In terms of net earnings, similar trend is observed whereby it has a general increasing trend in the last 6 years but experience a down trend from FY2012 to FY2014. The jump in revenue from FY2011 to FY2016 is 3.19 times from RM 113 million to RM 280 million.

Net profit margin wise, Top Glove scores a 12.50%, which is slightly above average for a manufacturing company. Return On Equity (ROE) wise, Top Glove performs well by achieving 19.71%.

On company’s debt, Top Glove has an acceptable debt to equity ratio at 0.22, meaning 22% of the company’s value is made up of current and long term liabilities. The company’s current ratio and cash ratio are of healthy value at 1.99 and 0.72 respectively.

Top Glove is outstanding in terms of dividend by paying a higher than average 4.63% dividend yield follow by an acceptable dividend payout ratio at 0.503.

In conclusion, Top Glove is a large enterprise with a great global presents and good fundamentals for having strong revenue and net profit value over the past 6 years as well as high dividend payout. Outlook in terms of growth for Top Glove is excellent looking at the jump of revenue and net earnings from FY2015 to FY2016 at 15% and 29% respectively. With these great growth results, the chance of share price break through for Top Glove based on continuation of strong fundamental performance is high and it is just a matter of time for it to happen for investors with longer term horizon.

Next quarterly results announcement should be on the month of Dec 2016 for Q1 results.

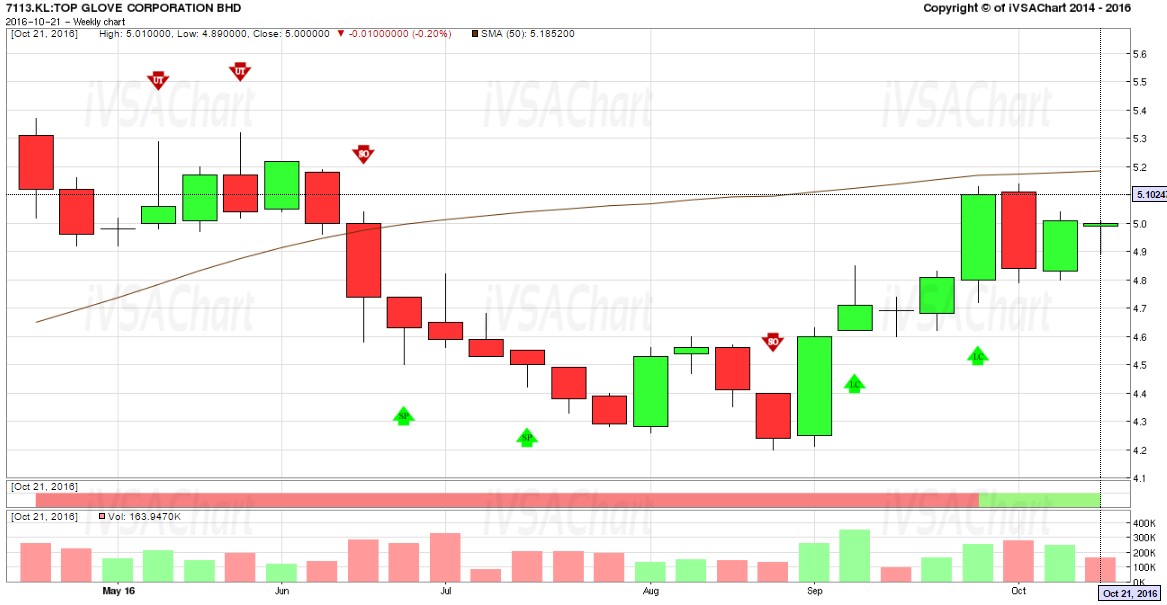

iVolume Spread Analysis (iVSA) & comments based on iVSAChart software – Top Glove

Based on Top Glove 6-month weekly iVSAChart, the market has tested the support around RM4.30 – RM4.20 levels, with lower prices rejected and then prices were gradually lifted higher to RM4.60 to RM4.80 levels with higher volume.

There is resistance level now around RM5.10 and at best, Top Glove will move sideways and re-accumulate in the short term. For investor with longer term view and patience, this is a good quality company to accumulate around current levels and during pull back, while enjoying a good dividend yield.

Interested to learn more?

- Free eBook available now! Click this URL to get your free eBook of “Get Rich with Dividends by Bill Wermine and Martin Wong”: http://ebook.ivsachart.com/

- Find out more about iVSAChart events via: https://www.ivsachart.com/events.php

- Follow & Like us on Facebook via: https://www.facebook.com/priceandvolumeinklse/

- Contact us via: email at sales@ivsachart.com or Call/WhatsApp at +6011 2125 8389/ +6018 286 9809/ +6019 645 3376

This article only serves as reference information and does not constitute a buy or sell call. Conduct your own research and assessment before deciding to buy or sell any stock. If you decide to buy or sell any stock, you are responsible for your own decision and associated risks.

More articles on iVSA Stock Review

Holistic View of Leon Huat with Fundamental Analysis & iVolume Spread Analysis (iVSAChart)

Created by Joe Cool | Dec 15, 2016

Holistic View of Tomypak with Fundamental Analysis & iVolume Spread Analysis (iVSAChart)

Created by Joe Cool | Dec 15, 2016

Holistic View of ECS IT with Fundamental Analysis & iVolume Spread Analysis (iVSAChart)

Created by Joe Cool | Dec 01, 2016

Holistic View of Magni-Tech with Fundamental Analysis & iVolume Spread Analysis (iVSAChart)

Created by Joe Cool | Dec 01, 2016

Holistic View of Teo Seng with Fundamental Analysis & iVolume Spread Analysis (iVSAChart)

Created by Joe Cool | Nov 14, 2016

Holistic View of QL Resources with Fundamental Analysis & iVolume Spread Analysis (iVSAChart)

Created by Joe Cool | Nov 03, 2016

Holistic View of Scientex with Fundamental Analysis & iVolume Spread Analysis (iVSAChart)

Created by Joe Cool | Oct 24, 2016

Holistic View of KESM with Fundamental Analysis & iVolume Spread Analysis (iVSAChart)

Created by Joe Cool | Oct 17, 2016

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

Bursa Stock Musings - Thoughts & Ideas

PGF Capital - insti shareholding up from 5% to 14%! (part 1)

2

南洋行家论股

4

The Alpha Trader

5

Koon Yew Yin's Blog

6

How to become a resilient trader

7

RHB Investment Research Reports

8

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....