Kenanga Research & Investment

Daily technical highlights – (BAUTO, AWC)

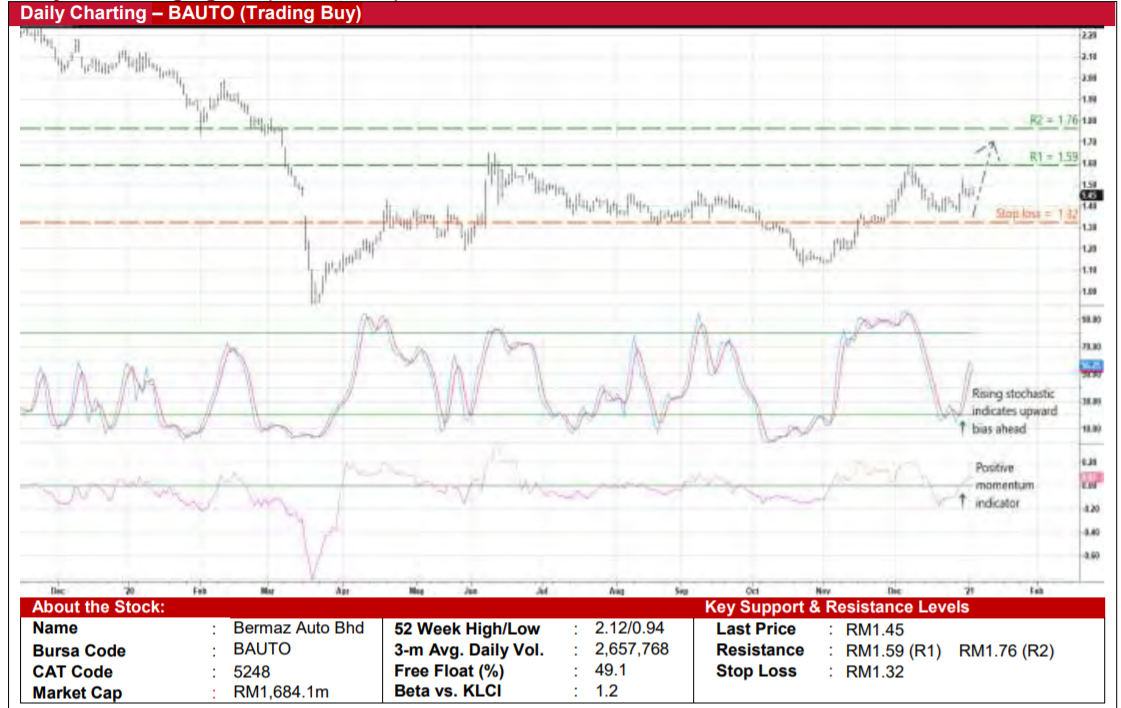

Bermaz Auto Bhd (Trading Buy)

• BAUTO is set to benefit from the double effects of the government’s extension of sales tax exemptions for motor vehicles (until end-June 2021) and the strengthening of the Ringgit and the Philippine Peso (both have appreciated against the Japanese Yen by 5.3% and 5.4%, respectively since the financial meltdown in March last year).

• With earnings on the recovery, consensus is projecting BAUTO – which is principally a distributor of Mazda vehicles in Malaysia and the Philippines – to make net profit of RM101m in FY April 2021 and RM150m in FY April 2022.

• The stock also offers attractive dividend yields of 3.4% for FY21 and 5.2% for FY22 based on consensus DPS of 5.0 sen and 7.6 sen, respectively.

• From a technical perspective, BAUTO’s share price – after correcting from a high of RM1.59 one month ago to settle at RM1.45 yesterday – could be resuming its ascending trajectory (which started in March last year).

• A breakout from the existing consolidation pattern appears likely as the stochastic indicator rises from the oversold zone while the momentum indicator cuts above the zero line.

• Riding on the upward strength, BAUTO shares will probably climb towards our resistance thresholds of RM1.59 (R1; 10% upside potential) and RM1.76 (R2; 21% upside potential).

• Our stop loss price is pegged at RM1.32 (or 9% downside risk).

AWC Bhd (Trading Buy)

• AWC is principally involved in the: (a) provision of integrated facilities management (IFM) services for buildings and facilities; (b) environment sector via the design, supply, installation, testing & commissioning and operations & maintenance of automated pneumatic waste collection systems; (c) engineering business as a contractor for the implementation of full air conditioning systems and mechanical & electrical engineering works for buildings and facilities; and (d) the provision of railway construction and maintenance solutions by supplying and providing specialized services in the areas of railway track, depot and rolling stock.

• The Group has recently clinched a slew of contracts valued at: (a) RM21m for sub-contract works for a water treatment plant in Malacca on 2 December; (b) RM5m for an IFM contract for a building in Sarawak on 3 December; (c) RM108m to provide hospital support services for a hospital in Shah Alam on 9 December; and (d) RM4m for the supply of rail grinding service for the MRT2 project on 5 January 2021.

• These contract wins are expected to contribute positively to future earnings as the Group is set to turn around after registering a net loss of RM18.8m in FY June 2020 (when its bottomline was hit by impairment losses).

• For 1QFY21, AWC reported a net profit of RM5.6m (versus 1QFY20’s net profit of RM6.7m and 4QFY20’s net loss of RM29.9m). The Group is also in a financially strong position with net cash holdings & short-term investments of RM68.8m (21.8 sen per share or almost half of its existing share price) as of end-September 2020.

• On the chart, the stock could see a trend reversal after overcoming a multi-year downward sloping trendline. The positive technical outlook is backed by its share price crossing over the 50-day SMA line and the recent appearance of bullish Dragonfly Doji candlesticks.

• On the way up, AWC shares will probably rebound to reach our resistance thresholds of RM0.52 (R1; 13% upside potential) and RM0.59 (R2; 28% upside potential).

• We have placed our stop loss price at RM0.40 (or 13% downside risk from yesterday’s closing price of RM0.46).

Source: Kenanga Research - 6 Jan 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Kenanga Research & Investment

Actionable Technical Highlights - PRESS METAL ALUMINIUM HLDG BHD (PMETAL)

Created by kiasutrader | Nov 25, 2024

Actionable Technical Highlights - PETRONAS CHEMICALS GROUP BHD (PCHEM)

Created by kiasutrader | Nov 25, 2024

Weekly Technical Highlights – Dow Jones Industrial Average (DJIA)

Created by kiasutrader | Nov 25, 2024

Malaysia Consumer Price Index - Edge up 1.9% in October amid food price surge

Created by kiasutrader | Nov 25, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

3

4

5

save malaysia!

Visa-free travel to China extended for Malaysians to 30 days

6

7

Good Articles to Share

Four convicted in Spain over homophobic murder that sparked nationwode protests

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....