OldSchool.com - Jae Jun

How to Normalize Earnings and Get Better EPS Estimates than Analysts - Jae Jun

Earnings ain’t bad.

*GASP*

Despite the consensus view that EPS is the bad guy in the value community, it’s still useful.

Sure I prefer to use free cash flow or owner earnings wherever possible, but cash flow isn’t a good measure for certain companies.

The easy trick is to just skip companies with negative or erratic cash flows, but some of my biggest wins have come from outside the “Buffett” quality companies with no debt, lots of FCF and growing revenues.

The second easiest method is to look up analyst earnings estimates and to use their numbers.

Yahoo makes it easy with their analyst estimates section and even I’m in the process of upgrading my data sources and database for Old School Value to include a whole range of analyst and industry estimates to help you make better estimates.

Despite this, the 7 deadliest words in investing according to Prof Aswath Damodaran, are

“They must know something that you don’t”

In other words, don’t believe what others say.

Are Analyst Earnings Estimates Accurate?

I do use analyst earnings.

But I don’t immediately discount my values simply because it’s different to the analysts.

After all, it’s a known fact that analysts are wrong all the time.

See below.

Optimistic Analyst Estimates

There are even papers on predicting analyst forecast errors.

Previously, I described how I check whether analysts are incorrect.

How to Tell When Analysts are Wrong

Using the analyst EPS, I work backwards to see what the revenue number is based on the expected EPS.

For example, if I look at Chipotle Mexican Grill (CMG), the analyst EPS for the current year end was $17.47.

To achieve an EPS of $17.47, the revenue has to come out to $5.3billion.

The TTM revenue is currently sitting at $3.8b. Even before the company released results, this was overly optimistic.

The released Q4 EPS was $3.84, which puts their final 2014 EPS at $14.13.

Far shy of the $17.47 estimate.

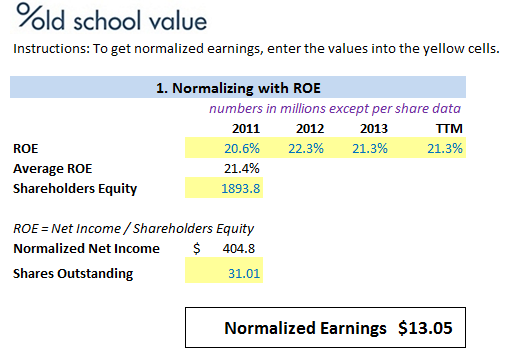

On the other hand, I get an EPS of $13.05 using a simple normalized EPS method that anyone can do (I have a spreadsheet for you at the end too).

$13.05 is also off the actual $14.13, but I’d rather be wrong on the conservative side instead of being too bullish and suffering the consequence.

A result of being conservative is missing a stock here and there, but a result of optimism is losing money quickly.

How to Normalize Earnings to Make Educated Assumptions Yourself

How did I get $13.05?

Here’s how you can calculate your own normalized EPS using one of the two methods explained by Aswath Damodaran.

Average the firm’s return on investment or profit margins over prior periods:

This approach is similar to the first one, but the averaging is done on scaled earnings instead of dollar earnings.

The advantage of the approach is that it allows the normalized earnings estimate to reflect the current size of the firm.

Thus, a firm with an average return on capital of 12% over prior periods and a current capital invested of $1,000 million would have normalized operating income of $120 million.

Using average return on equity and book value of equity yields normalized net income.

A close variant of this approach is to estimate the average operating or net margin in prior periods and apply this margin to current revenues to arrive at normalized operating or net income.

The advantage of working with revenues is that they are less susceptible to manipulation by accountants

More articles on OldSchool.com - Jae Jun

Revealing My Action Score Stock and the Dilemma of Selling - Jae Jun

Created by Tan KW | Oct 23, 2018

Priceless. Stock guide from a person with a few months of experience. - Old School Value

Created by Tan KW | Jun 14, 2018

Worried About the Market? Protect Yourself with Valuation - Jae Jun

Created by Tan KW | Apr 20, 2018

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Apps

Top Articles

1

https://dividendguy67.blogspot.com

2

3

4

6

Kenanga Research & Investment

7

Good Articles to Share

8

Good Articles to Share

Sydney house fire kills three children, police suspect homicide

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

No trading signals available.

Stock

Time

Signal

Duration

No trading signals available.

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....