OldSchool.com - Jae Jun

Are Net Net Stocks Worth Investing In? Here are 3 Quick Checks You can Perform - Jae Jun

April 14, 2015.

What You’ll Learn

- What is a net net and what characteristics they hold.

- A short list of net net stocks in the US market.

- 3 basic checks to perform on net-nets to see whether it’s worth investing in.

With such a hot market, a section of the market that is clearly overlooked is the cheap Graham net net market.

Net Net stocks have the following characteristics:

- ugly stocks

- horrible businesses

- big glaring issues

- bad management team

- often penny stock prices

The term net net comes from Graham, when he first came up with Net Current Asset Value and Net Net Working Capital.

NCAV = Current Liabilities – Total Liabilities

You can see how cheap a stock is if the price is below NCAV per share.

It’s telling you that the company is basically worth nothing more than the tangible assets on the balance sheet.

But net net’s aren’t totally useless because these ugly stocks are certainly overlooked.

Nobody wants to be holding a piece of junk that you can’t show off to friends.

I maintain a list of net nets to look at once a while, but during this bull market, the list is definitely thin.

At the time of this writing, the list is:

- Armco Metals Holdings (AMCO)

- STR Holdings (STRI)

- Ocean Power Technologies (OPTT)

- Emerson Radio Corp (MSN)

- Delcath Systems (DCTH)

- Sears Hometown and Outlet Stores (SHOS)

- SGOCO Group (SGOC)

Well there is one net net that is worth looking at.

Emerson Radio .

Calculate NNWC (Net-Net Working Capital)

When I look at net-nets, I ALWAYS look at the balance sheet.

I first use the NNWC (Net-Net Working Capital) method which is the most conservative measure. It’s a modified version of the NCAV formula above.

NNWC = Cash + (0.75 x Accounts receivables) + (0.5 x Inventory) – Total Liabilities

Think of it as the price a company will be sold for in a fire sale.

Here is what I see for Emerson Radio using the Net Net section of the Old School Value Analyzer.

Emerson Radio Net Net Calculation

At first glance, it’s looking good so far. The stock is trading below the NCAV and NNWC per share vale.

That’s extremely cheap and it also acts as a big margin of safety too.

A healthy balance sheet is a number 1 requirement for a failing business.

Moving onto the next check.

Check FCF or Owner Earnings

Next, I want to make sure that the net-net stock is not burning cash. The longer a company can live through its “burn rate”, the better.

Emerson Radio Cash Flow Positive?

If you look at FCF, the up and down is evident over the past 5 years. But it does pass the test of not being negative year over year.

The TTM figures are as of Q3 so it looks like fiscal 2014 will be another positive year for FCF.

Check Basic Items from Income Statement

Here’s where you get to see the issues Emerson is experiencing.

Keep in mind that I’m not trying to go too deep into analyzing the financial statements. There’s no need to with net nets because the issues are so obvious and if you know your accounting, you should be able to know the numbers in less than 10 minutes.

Emerson Radio Income Statement Notes

Revenues have been slashed, and SG&A is increasing which is a red flag.

At the moment, operating income is still positive though. It’s nothing pretty to look at however.

3 Basic Checks to Perform for a Net Net

For a net-net to be investable, it should:

- have a solid balance sheet, preferably more cash than inventory or receivables

- not be bleeding cash (at least breaking even or positive)

- have positive EBITDA

These are three very basic checks that will weed out many net-nets right away.

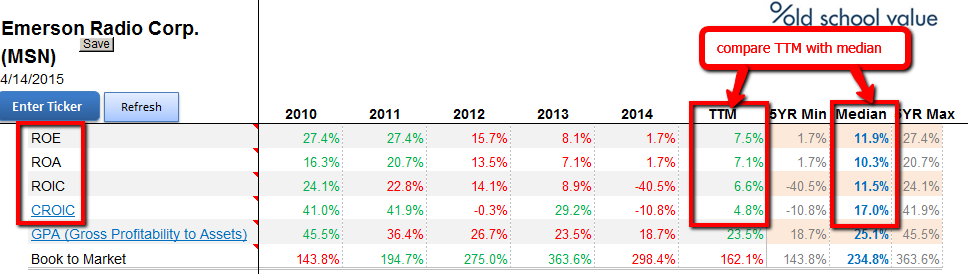

Revisiting some characteristics from up top, don’t expect much in terms of management effectiveness. Take a look at the following metrics.

Bad Business but Good Net Net?

The cash conversion cycle also tell a similar story.

Always Watch Cash Conversion Cycle

The median time to convert inventory to cash was 26.2 days. But in the TTM, it’s ballooned to 66.9 days.

Obvious issue glaring at you.

Is Emerson an Investable Net Net?

More articles on OldSchool.com - Jae Jun

Revealing My Action Score Stock and the Dilemma of Selling - Jae Jun

Created by Tan KW | Oct 23, 2018

Priceless. Stock guide from a person with a few months of experience. - Old School Value

Created by Tan KW | Jun 14, 2018

Worried About the Market? Protect Yourself with Valuation - Jae Jun

Created by Tan KW | Apr 20, 2018

Discussions

Be the first to like this. Showing 1 of 1 comments

Post a Comment

Featured Posts

Apps

Top Articles

1

https://dividendguy67.blogspot.com

2

3

4

6

Kenanga Research & Investment

7

Good Articles to Share

8

Good Articles to Share

Sydney house fire kills three children, police suspect homicide

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

No trading signals available.

Stock

Time

Signal

Duration

No trading signals available.

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

calvintaneng

EXCELLENT ARTICLE

These Are Terrible Characteristics

1) UGLY STOCKS. Unattractive. Avoided. Little or no coverage. If any the comments are negative. Long given up by the Mainstream Investors.

2) Horrible businesses.

Losses after losses. Being sued by creditors. Unpleasant law suit news

3) Big glaring issues.

Director paid themselves millions and give peanut to share holders. "Con man" type of leadership?

4)Bad management team. Failed business ventures? Lousy subsidiaries?

5) Fallen to penny stock levels. No demand at all. Seldom traded. Out of Investment Fund Coverage. Totally forsaken.

Well, to invest in these type of companies there are 3 basic criteria

1) IS ITS ASSETS WORTH MORE THAN LIABILITIES?

NET OF ASSETS IF CONVERTED TO CASH MINUS DEBT IS THE ACTUAL CASH OF THE COMPANY. SO IS IT SELLING BELOW CASH? THIS IS THE FIRST TEST. FAILING WHICH WE MUST GIVE IT A PASS.

2) IS THE BUSINESS VIABLE SOME DAY IN FUTURE? AN UPTURN LIKE THE REAL ESTATE OF ISKANDAR?

3) THEN DIVERSIFY INTO AS MANY COUNTERS AS POSSIBLE - 100 or more.

Some might fail. But Some Might turn out to be "FUTURE 10 BAGGERS!!"

After 40 long Years Walter Schloss testified that IT WORKS.

YES, BUYING TRASH PAYS!

2015-04-14 18:53