TeoCT

The Tale of Two Companies - Revenue

A Tale of Two Companies

Dayang & Perdana – Revenue

It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of Light, it was the season of Darkness, it was the spring of hope, it was the winter of despair, we had everything before us, we had nothing before us, we were all going direct to Heaven, we were all going direct the other way—in short, the period was so far like the present period, that some of its noisiest authorities insisted on its being received, for good or for evil, in the superlative degree of comparison only – Charles Dickens: A tale of two cities.

This is the second part of the journey. First a reminder of the light bulb moment.

Dayang owns 60.48% of Perdana. Perdana perform or not, straightaway 60.48% is transferred to Dayang. So, to invest in Dayang, one must look at Perdana and understand what is happening there.

Perdana

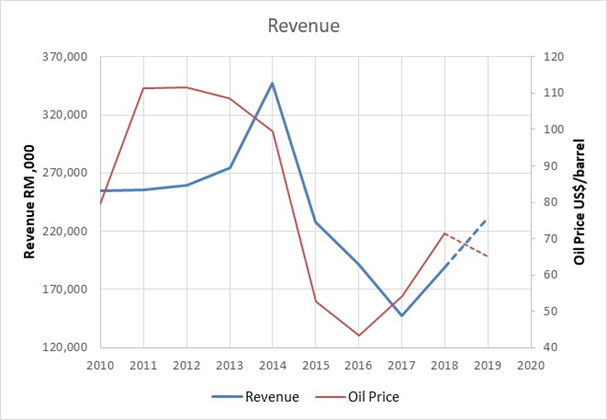

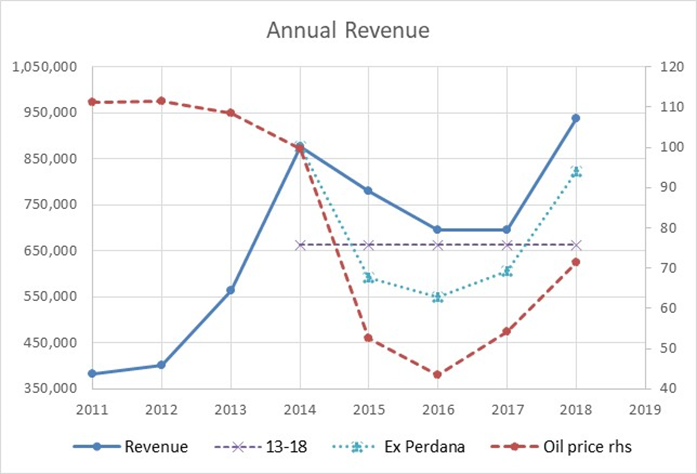

Revenues since 2010 are as shown:

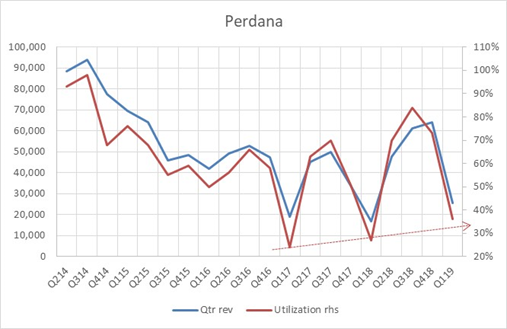

It appears that revenue is correlated to oil price, but with a lag of six to twelve months. Today, the average oil price (up to May) is US$ 65/barrel. It is too early to say 2020 revenue will be lower than 2019 or otherwise, as there are six months to go. Quarterly revenues are as shown below.

There is an increasing trend for first quarter utilization since 2017.

Q1 2019, utilization was 36%, a 9% gain from 27% of Q1 2018. It can be seen too that subsequent quarters utilization also increases compared to those from a year ago.

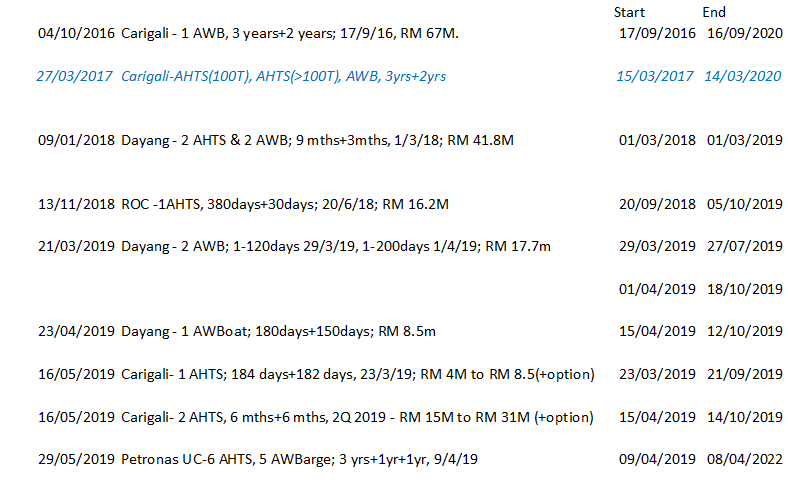

A breakdown of the contracts in hand are as shown with respective start and end dates.

Contracts in hand

Nine contracts worth over RM 220M and tender book is RM 240M (as reported in The Edge Financial Daily 23 May 2019). In the same Financial Daily, it was noted 15 of the 16 vessels are being used and that foreign vessel are now being sourced to support Perdana current fleet. As the report appeared on 23 May 2019 before the Petronas umbrella contract announcement, the 9 contracts worth would / could be more than the RM 220M mentioned. The cream of the 9 contracts is the recent Petronas umbrella contract, here is why:

When Velesto move one of their Naga rigs, who do they call – PERDANA.

When Carigali want a rig moved, who do they call – PERDANA.

When HESS want a rig moved, who do they call – PERDANA.

When Hibiscus want a rig moved, who do they call – PERDANA (to the music of Ghostbuster)

Quarter 1, 2019 revenue already saw a 53% increase year-on-year. Petronas Activity Outlook 2019 – 2021 shows a busy year for 2019; 16 to 18 jack-up rigs (who do they call – PERDANA).

So, with all the above information / knowledge, Perdana 2019 vessel utilization will surely exceed last year’s 64% (whole year). It is one busy year for PERDANA.

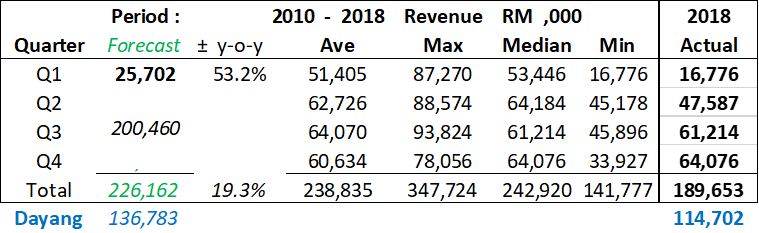

Figures in Bold are known / announced. Italic figures are estimates.

Forecasted 2019 revenue is RM 226M, a 19% gain from 2018 RM 190M. This is a conservative forecast with a 75% probability that Perdana will make RM 226M (± 5%), 25% chance that the revenue will be less than (RM 229M less 5% =) RM 215M. This forecast will be adjusted as quarterly results become known in August and November.

Dayang

Dayang revenues from 2011 to 2018 are as shown:

Do note that Dayang revenues excluding share of Perdana’s revenue is shown for the various shareholding from 98.01% (2015, 2016) to 60.48% since 2017.

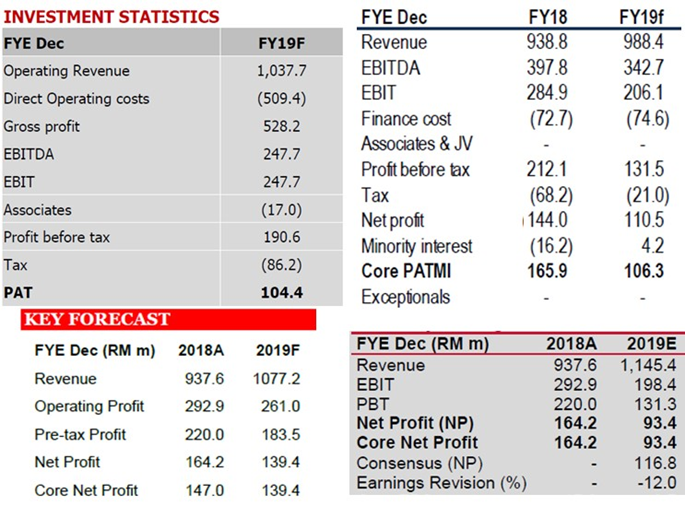

2019 revenue as estimated by the various investment banks (IBs) are as shown and these are assumed to have included 60.48% of Perdana’s 2019 revenue: -

IBs 2019 revenue is from RM 988.4M to RM 1,145.4M with an average RM 1,062M. The lowest to the highest difference is 16%. It is assumed the revenue included 60.48% of Perdana’s. Since Q1 result was announced, two IBs revised down their earnings (net profit) and two no change.

It is not possible to do a Mission Impossible like Tom, lowering into Dayang’s CFO office and get latest figures, so data from public domain is used for this latest and previous forecast.

But we do know the eights contracts won by Dayang as listed below: -

Dayang said the contracts in hand is worth RM 3B and this was before the contracts from Hibiscus and ROC were announced. Now, it would be nearer RM 3.5B.

As it is June now, work orders (WOs) in hand planned for implementation now till end of this year is firmed. Chances for these WOs to be cancelled would be nil. This is because material / equipment has been ordered; in various stages of assembly, fabrication, work crews and vessel scheduled, etc. These are already in various degree of completion, no turning back. As for next year, first quarter work should also be almost firm while second quarter might be subject to cancellation should oil price turn bad (falling below investment “hurdle” US$ 50 per barrel – Brent).

The only risk for remaining year would be adverse weather (tropical storm?) regardless of oil price.

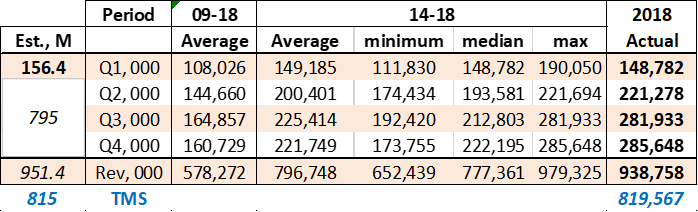

So, here is my latest estimate considering Q1 2019 result.

(Bold figures are announced; italic ones are estimates.2018 total is audited.)

Topside maintenance Services revenue would be 951 – 137 = RM 815M ONLY, about 1% less than 2018 given the lower TMS of Q1 2019 vs Q1 2018.

IBs revenue estimates appear bullish while mine is a bit conservative. However, the big difference would be the profit margin that will be covered in details in the next write-up. Stay tune.

As quarterly results become known (August and November), revenue forecast maybe tweak accordingly.

Appreciate readers constructive critique so that revenue can be more accurate with “wisdom of the crowd” (as oppose to madness of the crowd). Many thanks. Disclaimer as before.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

2024-11-22

DAYANG2024-11-22

DAYANG2024-11-22

DAYANG2024-11-22

DAYANG2024-11-22

DAYANG2024-11-22

DAYANG2024-11-21

DAYANG2024-11-21

PERDANA2024-11-21

PERDANA2024-11-21

PERDANA2024-11-21

PERDANA2024-11-18

DAYANG2024-11-18

DAYANG2024-11-18

DAYANG2024-11-14

DAYANG2024-11-14

DAYANG2024-11-14

DAYANG2024-11-14

DAYANG2024-11-14

DAYANG2024-11-14

DAYANG2024-11-14

DAYANG2024-11-14

DAYANG2024-11-14

DAYANGMore articles on TeoCT

The Great American Firewall: On the Question of Censorship by Danny Haiphong

Created by teoct | Jul 23, 2020

Discussions

1 person likes this. Showing 5 of 5 comments

Thanks for the sharing. Can't wait for the 3rd sequel and the wait is similar to waiting to watch the game of throne recently.....lol....

and bro teoact.....pls dun be so mean and drag the dayang trilogy into 6 episode like the GOT...lol

2019-06-11 11:36

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

Good Articles to Share

2

3

Mercury Securities Research

4

Koon Yew Yin's Blog

5

BFM Podcast

6

7

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

RainT

haha

I thought this article about company REVENUE

the title confusing

2019-06-10 23:19