In Peter Lynch's 6 Category of Stocks CYCLICALS FIT DUFU PERFECTLY

DUFU Has Gone Through A Cyclical Downturn And After Scraping the Bottom it will now Rise Back in its Cyclical Boom Times like the Turn of A Ferris Wheel

See

The Singapore Flyer (Ferris Wheel)

And on a clear day from the Top you can see both Johor & Indonesia

See what Dufu said about the time when it was at the bottom

Prospects (refer Bursa)

In 2023, the market cycle for Hard Disk Drives reached its lowest point. As we advance

through the second quarter of 2024, our Group is navigating the tail end of an unprecedented

downturn in the storage market

That was then!

Bad times never last if People Still Pursue Knowledge!

So see now what they "SEE AHEAD"

However, within our key operational domains - precision

machining of Hard Disk Drives and production of Sheet Metal and Stamping equipment and

components - we are witnessing a modest increase in demand.

We believe that global semiconductor sales are picking upand, coupled with a resurgence in

the memory sector, suggesting the potential onset of a new growth cycle, especially among

local manufacturers who typically lag behind global semiconductor players.This positive

momentum is supported by the conclusion of inventory adjustments and heightened demand in

electronics and AI-related applications.

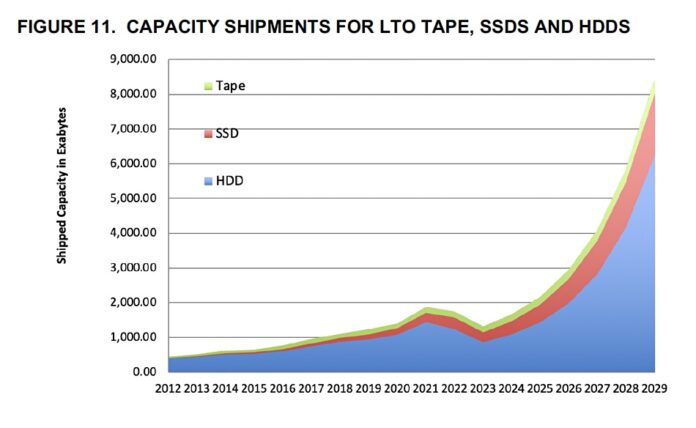

See this Chart

See chart above carefully

HDD Sales dipped from year 2021 down to 2023

Now see 2024 there is a gradual upturn

AND BEYOND 2025 TO 2029 HDD sales Will Go Up Like A Rising Ferris Wheel!

SO BETTER GET ON BOARD EARLY AND ENJOY THE RIDE UP

Warm Regards

Calvin Tan

Please buy or sell after doing your own due diligence

Or consult your Remisier/Fund Manager

DUFU IS EMERGING FROM ITS DARKEST NIGHT TO A COMING BRIGHT NEW DAWN AHEAD

Reposting Past Good Articles on Dufu below by others

From VALUE INVEST ASIA

The Master of Hard Disk: Dufu Technology Corp. Berhad

July 27, 2020

Dufu Technology Corp. Berhad(Dufu) (KLSE:DUFU) specialises in the manufacturing of precision machining parts and components for the Hard Disk Drive (HDD), industrial safety and sensor, telecommunications, computer and consumer electronics industries.

Since its listing in 2007, the stock has been a multi-bagger for its investors, its share price has grown over1,100% in value.In this article, we will take a closer look at Dufu’s business profile, management, and financials, to assess whether the company is suitable for an investment now.

Business overview

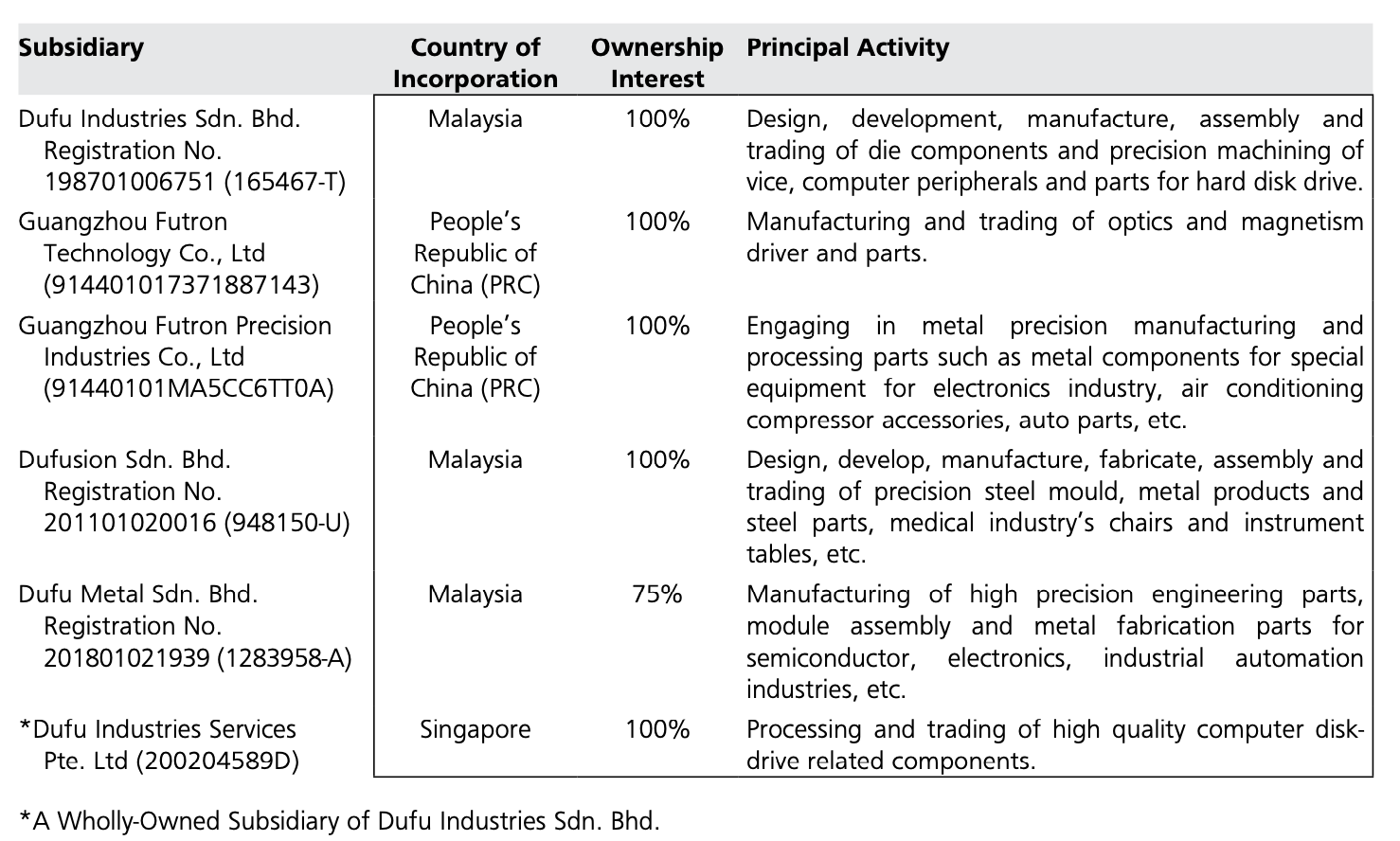

Dufu group is made up of seven entities. The listed entity is principally involved in investment holding while the principal activities of its six subsidiaries are as follows:

(Source: 2019 annual report)

The group manufactures the following products:

(Source: IPO prospectus)

More than 75% of Dufu’s revenue comes from the HDD segment where the group has established long term business relationships with its major customers such as Seagate Technology International (Singapore), Seagate Technology (Thailand) Ltd, Western Digital (M) Sdn Bhd, Western Digital (Thailand) Ltd and MMI Holdings Ltd. In fact, two of its major customers (unnamed) contributed 61.53% and 67.44% of the group’s revenue in 2018 and 2019 respectively.

(Source: 2019 annual report)

Dufu derives most of its revenue from abroad, 95% of which is denominated in US dollars (USD) while the bulk of the group’s expenses are paid in the respective local currencies where it operates. Therefore, the gradual strengthening of USD versus the Ringgit is a favourable trend and should give the group a lift in its operating margins.

(Source: 2019 annual report)

Industry players and market position

HDD manufacturers source HDD components from a handful of suppliers only. They are stringent in their selection of component and parts suppliers as quality, reliability and delivery time are crucial in this competitive market. The production volume allocation for the component or part is determined on a quarterly basis. Quality and cost are two primary determinants for an increase in production allocation for a given quarter from its existing qualified suppliers.

The closest competitors to Dufu for the supply of HDD disk spaces and clamps to Seagate and Western Digital are seen as:

To the best of knowledge of its directors, the group estimates that it is one of the top suppliers of HDD disk spacers and has a 20-30% market share globally.

Future prospects and strategies

Dufu’s prospects are very much tied to the HDD industry. International Data Corporation (IDC), in its Data Age 2025 report, predicts that worldwide data creation will grow to an enormous 163 zettabytes (ZB) by 2025, which is 10x the amount of data produced in 2017, where hard drives will be central in managing 70% of the data-sphere.

Internet of Things (IoT), real-time data, cognitive artificial intelligence (AI) systems, increased security data requirements, and big data analytics are among the key trends that should result in strong demand for high capacity HDDs. Therefore, Dufu, which manufacturers HDD-related components, is set to ride on this increasing demand.

Despite the positive projections in HDD, Dufu acknowledges that it faces significant business and customer concentration risks. The group intends to diversify its product portfolio and penetrate into the automotive segment following its International Automotive Task Force (IATF) 16949:2016 certification on 15 April 2019. While discussions are in progress for its automotive products, this segment is still at a very nascent stage to contribute positively to the group’s top-line growth.

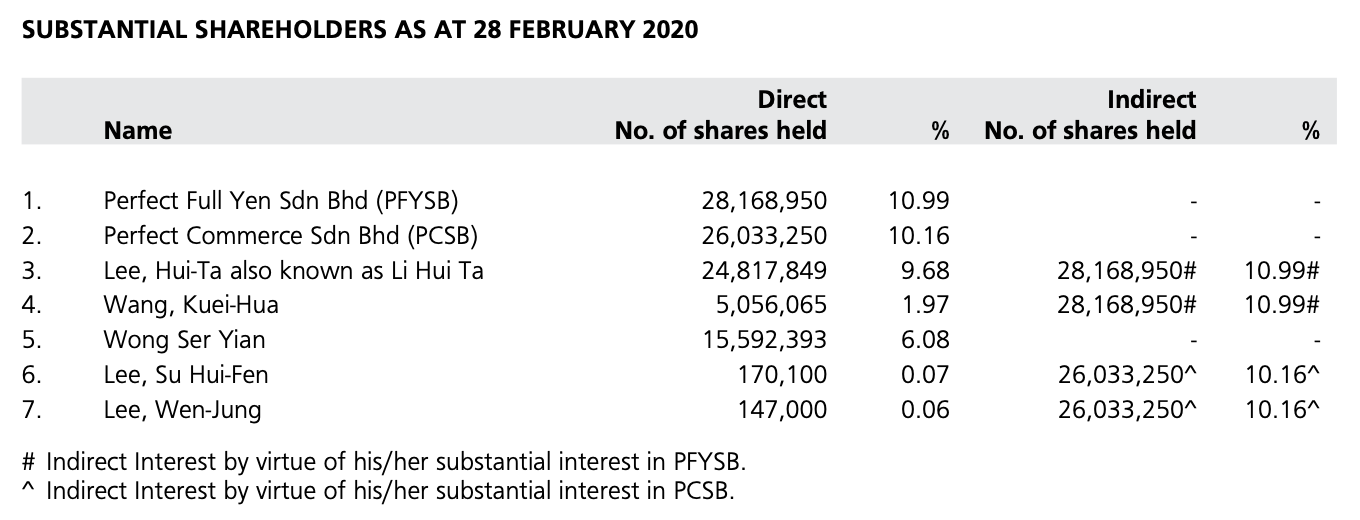

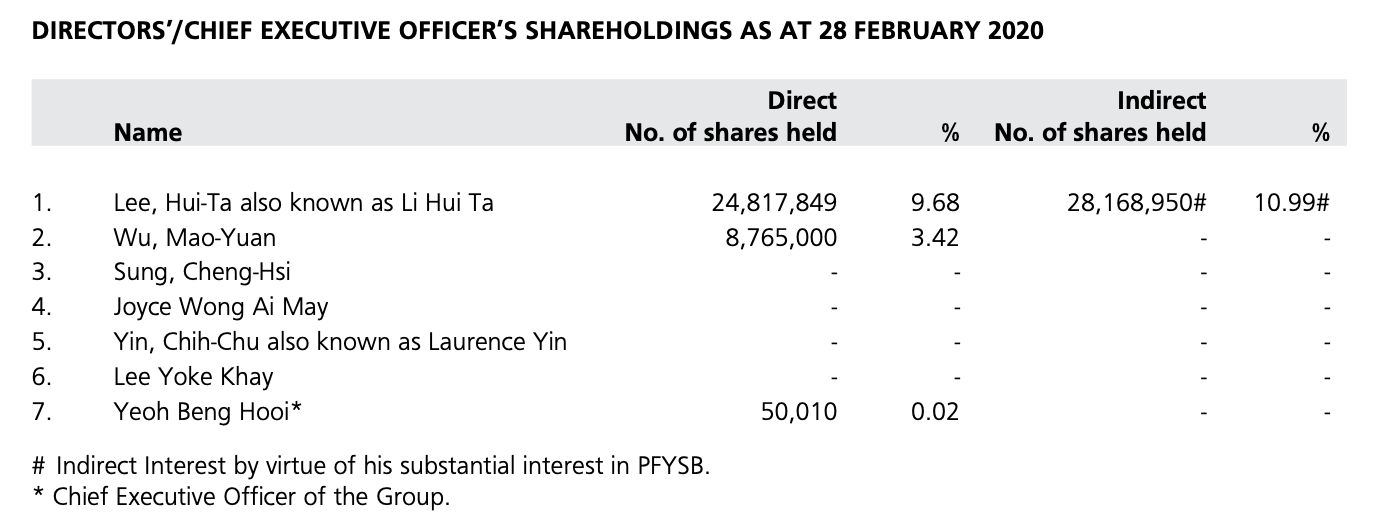

Major shareholders and leaders

Dufu’s largest shareholder is Mr. Lee Hui-Ta (also known as Li Hui Ta) with a direct and indirect equity stake of 20.67%. Ms. Wang Kuei-Hua is Mr. Lee Hui-Ta’s spouse. Mr. Lee Hui-Ta is the Executive Chairman and Co-founder of the group and has more than 28 years of experience in precision tooling and precision machining.

(Source: 2019 annual report)

Key senior management personnel include Mr. Wu Mao-Yuan who serves as Executive Director since 2015. Mr. Wu is also the Managing Director of Guangzhou Futron Technology Co. Ltd, a subsidiary of the group. He owns an equity stake of 3.42% in Dufu.

Separately, Mr. Yeoh Beng Hooi is the Chief Executive Officer (CEO) since 2015, after serving as Chief Operating Officer (COO) since 2004. He has a 0.02% equity stake in the group.

(Source: 2019 annual report)

Financials

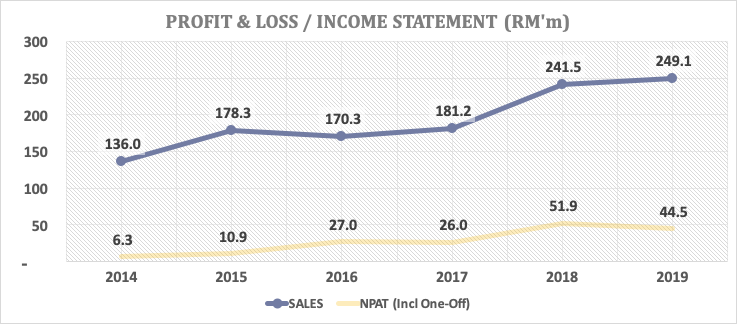

Measure 1: Growth in revenue and profits

Dufu has achieved growth in revenue and profits at compounded annual growth rates (CAGR) of 12.87% and 47.84% from 2014 to 2019. These are commendable growth rates.

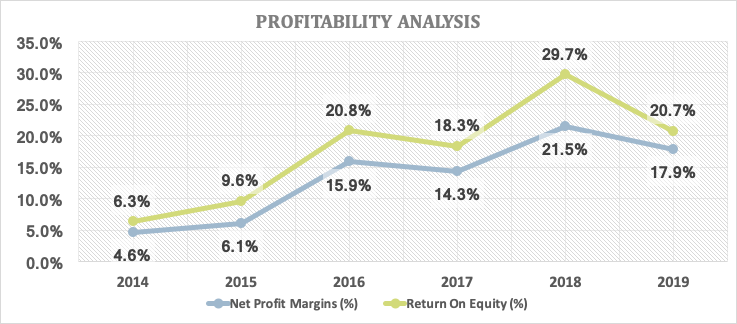

Measure 2: Profitability

Dufu’s net profit margins have tripled from 6.3% in 2014 to 20.7% in 2019. Meanwhile, the group’s return on equity ratios has improved substantially over the same period from 4.6% in 2014 to 17.9% in 2019.

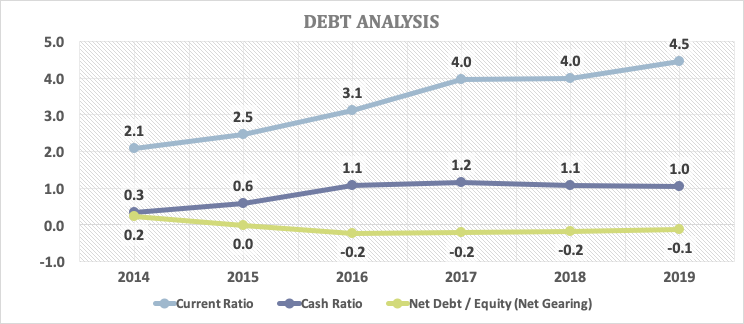

Measure 3: Liquidity

Dufu’s current and cash ratios are at healthy levels. The group also does not have gearing issues as it is in a net cash position. As at 31 December 2019, Dufu has cash and cash equivalents of RM43.5 million versus total borrowings of RM17.5 million.

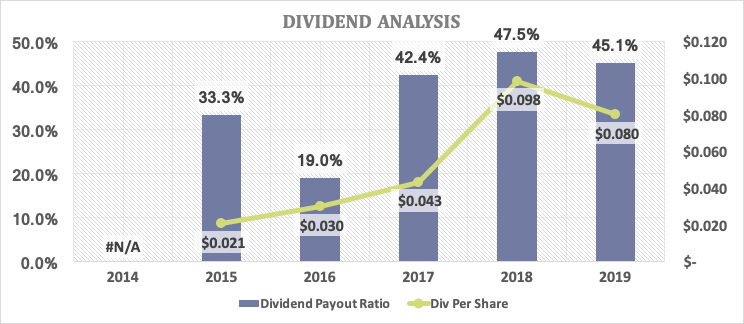

Round 4: Dividends payout

Dufu has rewarded shareholders with increasing dividend per share in line with increasing profits. In recent years 2017 – 2019, the dividend payout ratio has been above 40% of profits.

Conclusion

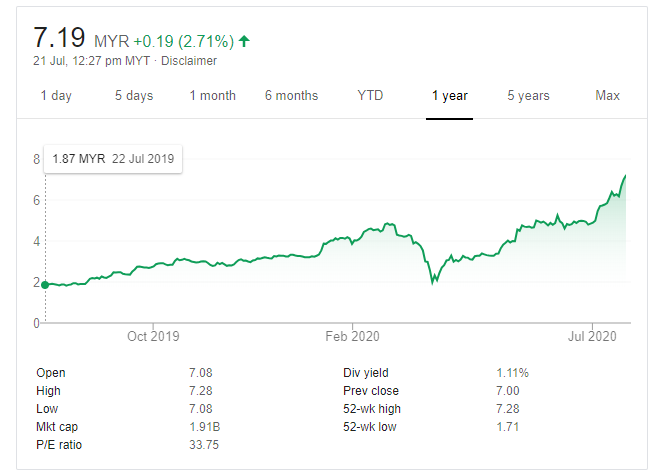

With a closing share price of RM7.19 as at 21 July 2020, Dufu is trading at a price to earnings (PE) ratio of 34, with a market capitalisation of RM1.9 billion.

Dufu’s operations were affected in Q1-Q2 2020 as its plants in China and Malaysia were temporarily shut down due to the preventive measures towards the Covid-19 pandemic. Both plants have subsequently recovered back to full workforce but the group remains cautious of potential supply chain disruption risks since the scale and length of the pandemic remains unresolved.

Over the long term, Dufu’s growth is underpinned by higher demand for storage solutions given the huge growth in data consumption as well as technological advancements in increasing the number of components within an HDD platform. Investors with knowledge and expertise in this area could find Dufu of interest.

(Source: Google Finance)

Market Segment

Product

HDD components

Spacer

Clamp and spring washer

Circular latch

Swage pin

Ground pin

Extreme coil pin

Hexagon nut

Industrial safety and sensor components

Heat and gas sensor housing

Infra-red sensor housing

Sensor terminal pins

Sensor cap

Lead frame

Telecommunication components

Battery connector

Balance weight

Computer peripheral components

Contact solder

Consumer electronics components

Mounting bar

Reflection plate

Back cab

Chassis

Heat sink

Bracket

Others

Terminal (Automotive)

Shunt resistor (Automotive)

2019

RM

2018

RM

Customer I

122,621,649

114,207,846

Customer II

45,393,505

34,323,740

168,015,154

148,531,586

Group revenue

249,122,579

241,451,305

% of group revenue

67.44%

61.53%

2019

RM

2018

RM

Malaysia

18,187,477

22,967,833

China

41,050,764

39,498,571

Singapore

19,022,641

19,470,894

Thailand

142,599,974

127,535,840

Other countries

28,261,723

31,978,167

Total

249,122,579

241,451,305

Disk Precision Industries Pte Ltd (DP), Singapore and Global Primax, China (for Seagate); and

DP and Notion VTec Berhad (KLSE:NOTION) (for Western Digital).

Dufu has rewarded shareholders with increasing dividend per share in line with increasing profits. In recent years 2017 – 2019, the dividend payout ratio has been above 40% of profits.

Conclusion

With a closing share price of RM7.19 as at 21 July 2020, Dufu is trading at a price to earnings (PE) ratio of 34, with a market capitalisation of RM1.9 billion.

Dufu’s operations were affected in Q1-Q2 2020 as its plants in China and Malaysia were temporarily shut down due to the preventive measures towards the Covid-19 pandemic. Both plants have subsequently recovered back to full workforce but the group remains cautious of potential supply chain disruption risks since the scale and length of the pandemic remains unresolved.

Over the long term, Dufu’s growth is underpinned by higher demand for storage solutions given the huge growth in data consumption as well as technological advancements in increasing the number of components within an HDD platform. Investors with knowledge and expertise in this area could find Dufu of interest.

DUFU PEAKED ABOVE RM7.00 IN GOOD TIMES

WILL DUFU GO BACK THERE?

ONLY TIME WILL TELL

Share this:

More articles on THE INVESTMENT APPROACH OF CALVIN TAN

Calvin, finally after you got their funds stuck there for so long, you are guiding them the make real profits in klse superbull run (But jcy, notion and dufu have gone up so much....Can't you ask them not to chase high but to wait for double bottom?)

Calvin, no mention on Dufu's receivables since you like to harp on this issue? Btw, the current PE is very high. You seem to have a problem in stock picking...

Eagle Group members who bought bplant at 57 sen, Jtiasa at 63 sen, Taann at Rm2.75, Thplant at 47 sen, Fgv at Rm1.16 and even Tsh at Rm1.09 are all doing fine. Many received best ever dividends

Outlook: Demand for large capacity HDDs mainly for cloud and enterprise computing and increasingly for Artificial Intelligence (AI) machine learning data storage has seen a resurgence of demand and orders as we serve that space diligently. We have established long-term relationships with these major HDD makers and the commitment for long-term supply is of paramount importance. We will grow in line with the industry growth pattern

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

calvintaneng

Peter Lynch: What is a Cyclical Stock and How to Invest in them? | Stock Shop 1998【C:P.L Ep.41】

https://www.youtube.com/watch?v=hCSD5zbNxeQ

2 months ago