CEO Morning Brief

Analysts Lift Kossan’s Target Price, Earnings Outlook, But Cite ‘lofty’ Valuation

edgeinvest

Publish date: Fri, 17 Nov 2023, 08:54 AM

KUALA LUMPUR (Nov 16): Analysts lifted Kossan Rubber Industries Bhd’s target price (TP) after it beat expectations to swing to profit in the third quarter ended Sept 30, 2023 (3QFY2023), on better sales volume expected amid customers' inventory replenishment activities.

However, persistent pricing competition due to an oversupply in the industry will keep average selling prices (ASP) flattish in the near term, the analysts said.

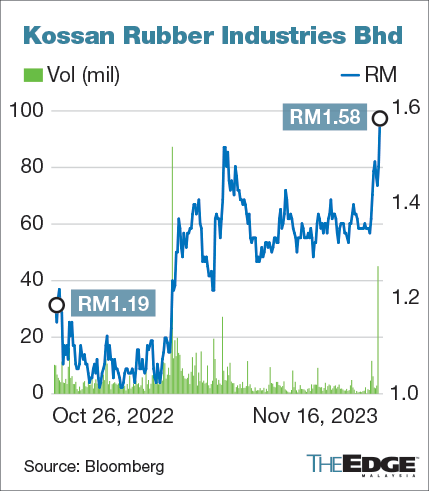

Shares of Kossan opened higher and rose as much as 16 sen or 10.8% to an 18-month high of RM1.64 in the morning session as net profit rebounded to RM40.97 million in 3QFY2023, after two consecutive quarters in the red.

The counter retreated to close at RM1.58, its highest in 17 months. It was 10 sen or 6.76% higher than its last closing price on Wednesday, and gave it a market capitalisation of RM4.04 billion.

Revenue came in at RM403.48 million, up 4.11% quarter-on-quarter (q-o-q) but down 28% year-on-year (y-o-y).

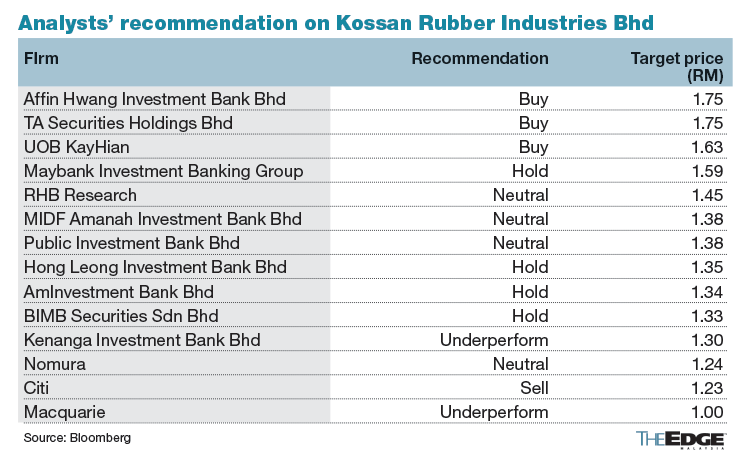

In a note on Thursday, Kenanga Research raised Kossan’s TP to RM1.34, from RM1.28, as it now projects the group to post a net profit of RM44 million in FY2023, from an earlier forecast of losses amounting to RM76 million.

However, it downgraded the counter to “underperform”, citing lofty valuations based on 42-87 times forward price-to-earnings ratio and forward return on equity of 1-2%.

The research house expects the over supply situation to persist “at least over the next 12 months”, and excess capacity of 112 billion pieces in 2023 “which is similar to 2022”, despite a 15% increase in demand this year.

Separately, Hong Leong Investment Bank (HLIB) pointed out that Kossan’s core profit after tax and minority interest (Patami) of RM32.1 million surpassed both its expectations of RM67.7 million in losses and consensus estimates of RM66.5 million in losses.

"The key deviation from our forecast was due to lower-than-expected costs on the back of better cost control management,” said HLIB, which upgraded the counter to “hold” with a higher target price (TP) of RM1.35, from RM1.

TA Securities, which has a “buy” call with higher TP of RM1.75 (from RM1.60) also pointed to improved q-o-q performance by Kossan’s technical rubber products and clean room divisions’ performance.

However, it highlighted Kossan’s 9MFY2023 profit before tax (PBT) of RM32.4 million reflected a weaker y-o-y performance, mainly due to a 22% decline in ASP, a 25% decline in volume, and increased energy and labour costs.

MIDF Research sees ASP for Kossan’s gloves division remaining “flattish in the near term”, it said in a separate note. It pointed to the oversupply amid intense competition from Chinese players.

That said, buyers are replenishing their glove inventory following the expiration of pandemic-related stockpiles, it said, which would in turn support utilisation rate, resulting in production costs per unit and improved margins.

MIDF upgraded Kossan to “neutral” with a much higher revised TP of RM1.38 from 88 sen.

Meanwhile, PublicInvest Research upgraded its call to “neutral” at a higher TP of RM1.38, from RM1.08.

It sees lower raw material prices and the strengthening US dollar working in the company’s favour, and increased demand for the technical rubber products segment which could push revenue higher “in tandem with improved infrastructure spending”.

At the time of writing, Kossan shares traded up 11 sen or 7.43% at RM1.59, giving it a market capitalisation of RM4.07 billion. The counter is up more than 42.7% this year, Bloomberg data showed.

Kossan's better-than-expected performance spurred some trading activity among glove counters. Others who are yet to announce their results for the quarter ended September include Supermax Corp Bhd, as well as lower-liners Comfort Gloves Bhd, Careplus Group Bhd and Hextar Healthcare Bhd.

At the time of writing, shares of Supermax rose two sen or 2.32% to 88 sen, alongside Comfort (up two sen or 5.55% to 38 sen), Careplus (up one sen or 3.63% to 28.5 sen), and Hextar Healthcare (up 2.5 sen or 12.19% to 23 sen).

Shares of Top Glove Corp Bhd also rose three sen or 4% to 78 sen, while Hartalega Holdings Bhd shares traded unchanged at RM2.35.

Kossan's improvement was in line with its peer Hartalega Holdings Bhd, which earlier this month also posted a profit after three consecutive quarters in the red.

Meanwhile, Top Glove Corp Bhd recorded its worst quarterly performance in the quarter ended Aug 31, 2023 (4QFY2023) with RM463.15 million in losses on revenue of RM475.87 million, due to wider operating losses and impairments recorded in the quarter.

Read also:

Kossan returns to black in 3Q with better cost controls, lower material costs

Source: TheEdge - 17 Nov 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

2024-08-24

HARTA2024-08-24

KOSSAN2024-08-24

TOPGLOV2024-08-23

HEXCARE2024-08-23

KOSSAN2024-08-23

KOSSAN2024-08-23

KOSSAN2024-08-23

KOSSAN2024-08-23

KOSSAN2024-08-23

KOSSAN2024-08-23

KOSSAN2024-08-23

KOSSAN2024-08-21

HARTA2024-08-21

HARTA2024-08-21

KOSSAN2024-08-21

KOSSAN2024-08-21

KOSSAN2024-08-21

TOPGLOV2024-08-20

HARTA2024-08-20

TOPGLOV2024-08-16

KOSSAN2024-08-14

HARTA2024-08-14

SUPERMX2024-08-13

CAREPLSMore articles on CEO Morning Brief

High Court Allows Felda and FIC to Obtain Two Classified Reports as Evidence in Semarak Land Suit

Created by edgeinvest | Aug 23, 2024

RM49,000 Deposited Into Wan Saiful's Personal Account Two Years Ago, Says Witness

Created by edgeinvest | Aug 23, 2024

'Lembu' and 'durian' Among Codes Used by Officers at KLIA Allegedly Involved With Syndicate

Created by edgeinvest | Aug 23, 2024

1MDB-Tanore: Defence Says Jho-Low 'mirror-image' of Najib Theory Lacks Proof

Created by edgeinvest | Aug 23, 2024

Naza-Berjaya JV Files Notice of Discontinuance Over Challenge of Govt Vehicle Fleet Project

Created by edgeinvest | Aug 23, 2024

Kerjaya Prospek Unit Sues Yong Tai Subsidiary Over Alleged Unpaid Sum of RM105 Mil

Created by edgeinvest | Aug 23, 2024

PTT Synergy Inks Deal With China's Siasun to Distribute Autonomous Equipment in Malaysia

Created by edgeinvest | Aug 23, 2024

Hextar Retail to Introduce Hong Kong's Tam Jai Noodle Chain in Malaysia

Created by edgeinvest | Aug 23, 2024

Capital a Secures US$443m Revenue Bond to Strengthen AirAsia Fleet, Financials

Created by edgeinvest | Aug 23, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

.png)

Apps

Top Articles

1

Mercury Securities Research

2

save malaysia!

3

4

The Alpha Trader

7

8

THE INVESTMENT APPROACH OF CALVIN TAN

JCY (5161) Posted a 2nd Qtr of Good Profits: Showing a Clear Sign of A Turnaround, Calvin Tan

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....